Sharing my notes from latest updates from investor ppt, concall and from my own insights:

-

Company is venturing into manufacturing of crowns, bridges, veneers, dentures and other orthodontic products via its Smile Labs ventures. This market has huge TAM of $1.7 Bil USD growing at 11% CAGR

-

Smile Labs was acquired and Vasa owns 60% of it. It was doing a revenue of 5 Cr before acquisition

-

Company wants to digitize the entire design and manufacturing process and also reduce the turnaround time which should act as a major differentiator.

-

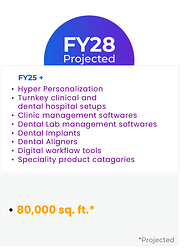

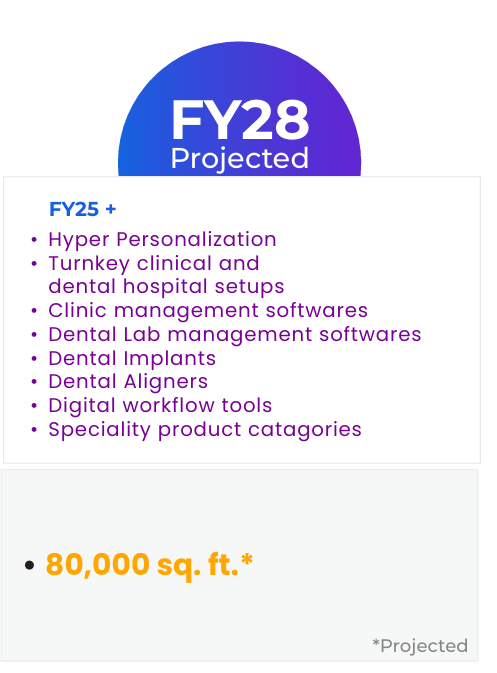

Their 2028 vision looks aggressive and showcases the management’s vision to grow far beyond the current limited TAM of consumables and selling Chinese equipment. Planning to double warehouse area.

-

They have also revamped their mobile app and website to drive more traffic and optimize conversion rates. It still doesn’t feel as smooth as some other e-commerce apps, reminds me of Aliexpress app.

-

Reducing delivery timelines has led to some increase in delivery days.

-

Company’s vision is to have 35k SKUs (currently 20k SKUs). They are inspired by Henry Schein, which is a 9.5 Bil US based company

-

Own brand mix is 50%, has been the same for past 3-4 quarters. Aim is to reach 70% by 2027-2028. This includes exclusive brand partnerships as well as white label sales. But it doesn’t matter that much because margins are same for both own branded and other products.

-

Guidance: Company had given a guidance of 70% sales growth in FY25, which seems unlikely. Promoter said that this was their internal target and he shouldn’t have disclosed this. Personally, I had invested considering a 45% sales growth by looking at their historical customer traffic, unique customers and TAM, so my thesis remains intact but still disappointing to see

-

On FY26, the promoter said a non-committal growth figure of 30% and didn’t give a solid comment on the 500 Cr sales figure for FY27 that was mentioned in a previous concall. I don’t consider this as unrealistic if their orthodontics venture takes off.

-

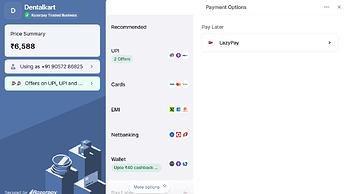

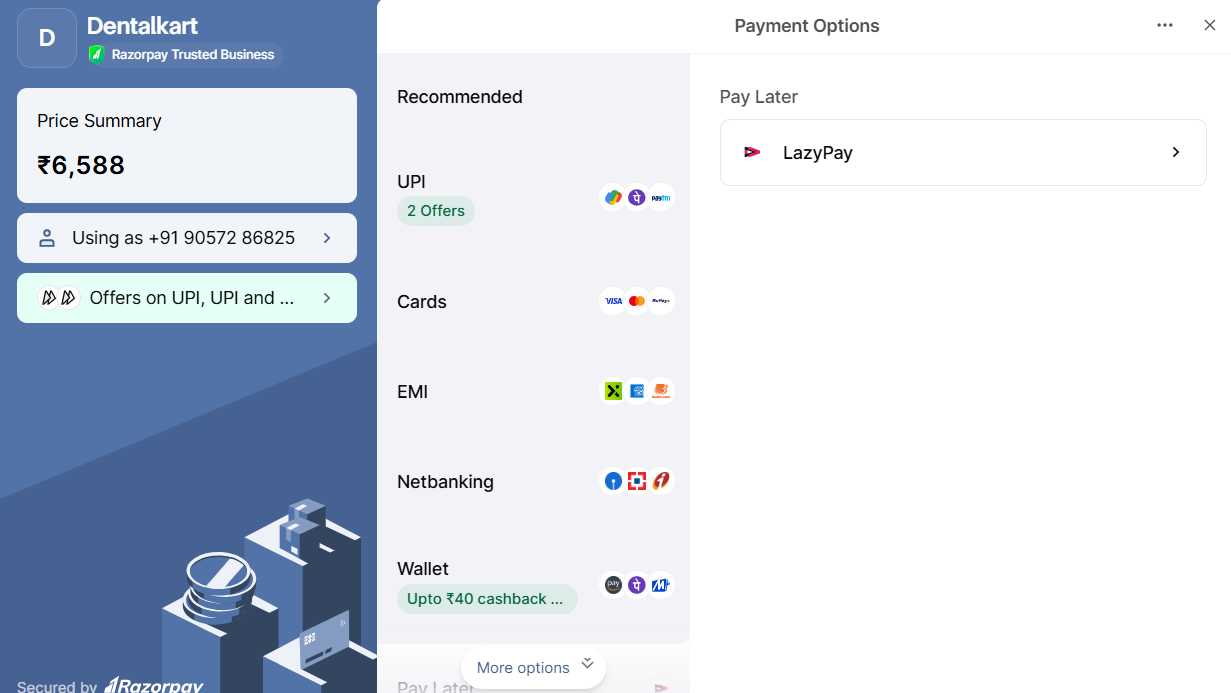

Company has launched BNPLfor 25-50k sales items and company is planning to partner with an NBFC to allow customers to finance purchases up to 10 lacs (basically setting up an entire dental clinic). But BNPL is hidden under “more options” section below other payment methods, so I am not sure if they would see the boost that they should get from this.

-

Company is planning to open service centers in Tier-1 cities for large ticket equipment

-

Main pro in this company that I feel is that the CEO is young, hungry and has clarity and vision. I know, these are all soft factors but execution is key especially in e-commerce businesses and all the TAM in the world is worthless if you can’t execute

| Subscribe To Our Free Newsletter |