IMO that is not the reason for its low valuation due to the following reasons :

-

The cumulative CFO/PAT from FY20-FY24 is 90% + as PAT IS 13CR and CFO is 12CR.

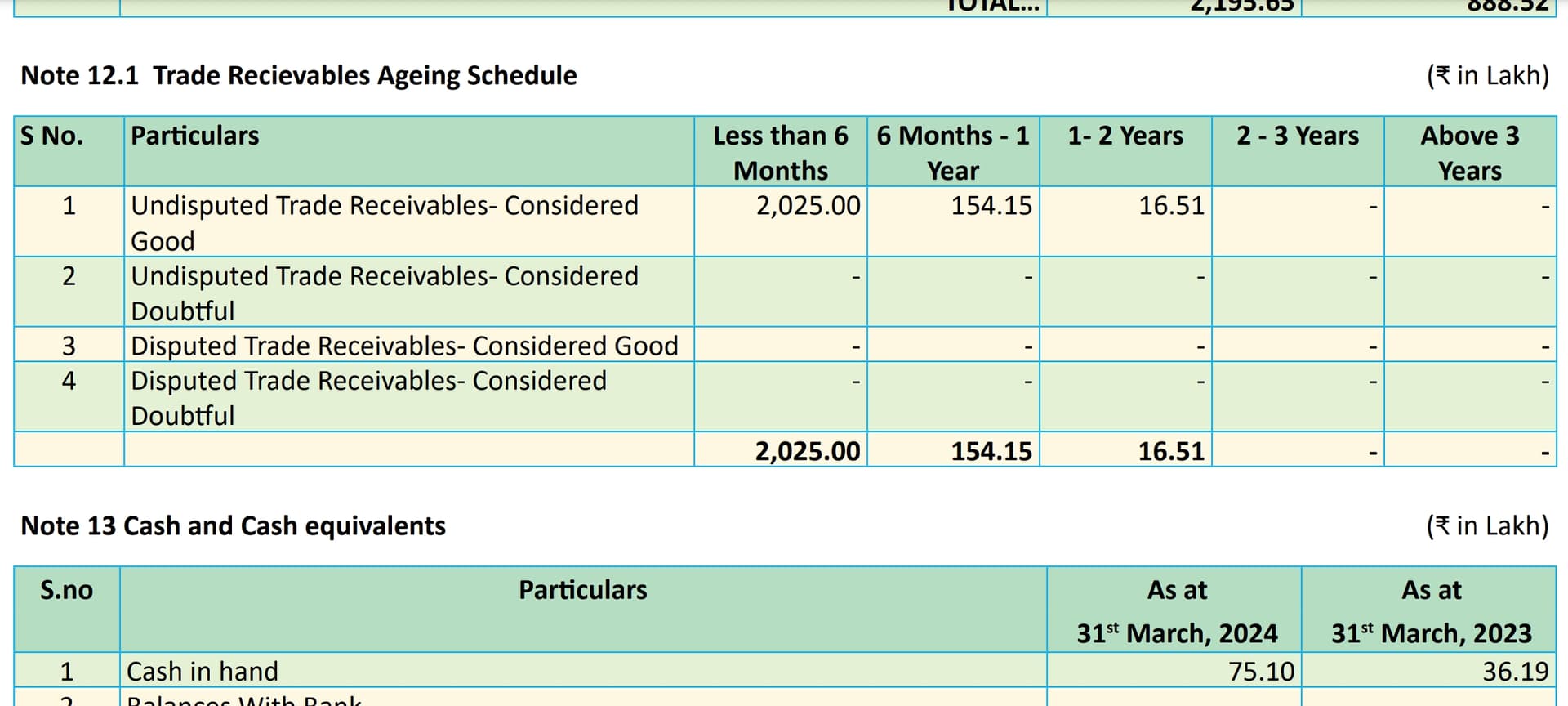

Most of the trade receivables are for a period of less than 6 months.

-

Its peer Antony waste has 30% of receivables as a percentage of sales. Urban enviro waste has 128cr sales and 34cr receivables which means it has ~26% of receivables as a percentage of sales.

-

The company is in B2G sector which is known for having high receivables but comparing with other companies its receivables still look healthy and even when most B2G companies have given negative CFO, in H1FY25 its CFO was positive.

Some more points to add

- The company doesn’t have significant related party transactions and it is in B2G sector which makes it a bit difficult compared to B2B to show fictitious sales and profits.

I would really appreciate if someone could highlight any red flag or discrepancies which this company or its management might have.

Thank you.

Disclosure not a buy /sell recommendation.

| Subscribe To Our Free Newsletter |