- True, the management also recognizes this in the annual report. See screenshot from page 47 of AR 2014-15 below:

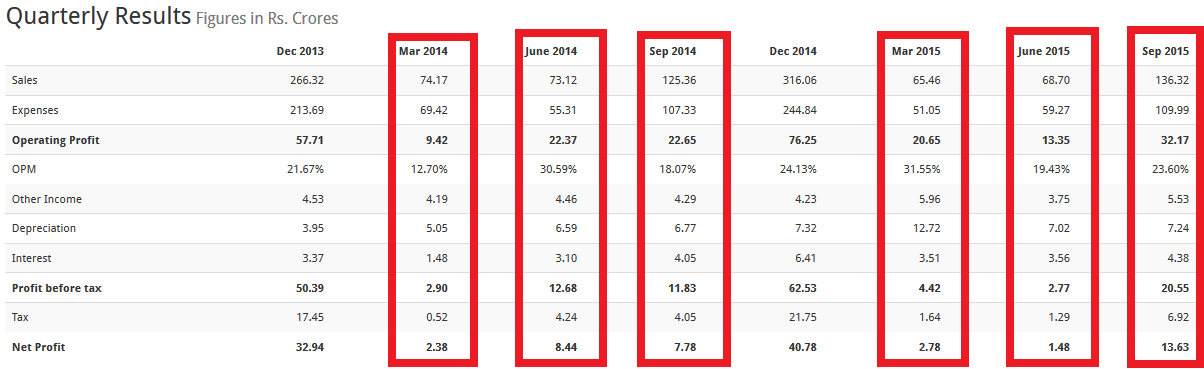

You are correct that 50% of sales are now from the cotton segment. I do not know the margin in this segment as segment-wise analysis is not available in the AR. It is likely that margins are decent. This is evident from the fact that in non-winter quarters the net profit is lower than Q3 but margins are intact(but they seem to vary a lot). Screenshot (there was an adjustment of inventory from June 2015 to Sep 2015):

I would say increase in debt is due to increased store openings. The stores have increased 10% over the last year. Also, the management has indicated in the investor presentation that the company is investing into marketing and advertisement. However, inputs welcome.

I am not very knowledgeable on the institutional arrangements. I know of a few people that buy MC without any institutional tie up. There is a positive spin to an institutional arrangement though – guaranteed sales visibility without marketing and store costs?

| Subscribe To Our Free Newsletter |