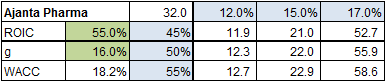

Using the formula: (1 – g/ROCE)/(WACC – g) from Valuation by McKinsey (page 66), I tried to find out a reasonable PE for Ajanta. Results are displayed in table below. Seems a lot depends on long term growth rate which the market is currently implying at 16% (PE of 32)

WACC picked up from http://www.gurufocus.com/term/wacc/NSE:AJANTPHARM/Weighted%2BAverage%2BCost%2BOf%2BCapital%2B%2528WACC%2529/Ajanta%2BPharma%2BLtd

Disclosure: Invested. Forms a significant part of portfolio

| Subscribe To Our Free Newsletter |