Irdai is intensifying scrutiny of cybersecurity lapses in the insurance sector following a major data breach at Star Health Insurance. Over 31 million customers’ data was compromised. The regulator has mandated an extensive audit of Star Health’s cybersecurity framework. The audit aims to identify control gaps and recommend measures to prevent future breaches.

Tata group listed stocks a mixed bag: Here are the top gainers on Thursday (10-10-2024)

Tata Investment rises almost 6 per cent while TCS ends a per cent lower

Tata elxsi (10-10-2024)

We need to also see the Revenue and Profit Growth of MNC IT players like Accenture, Cap Gemini and others to check if this slow growth witnessed by TCS and Tata Elxsi both is across the world or India specific.

Since the growth of 5% looks certainly low, one reason could be US elections which are round the corner and certain large deals might be on hold, which might be awarded after election results and/or start of USA New Financial Year.

Generally Q1 and Q2 are better than Q3 for IT industry due to long holidays in Q3, but if Q2 it self is slow than expectations then we need to look at other data points as well.

Just an opinion since worked in IT industry for 2.5 decades.

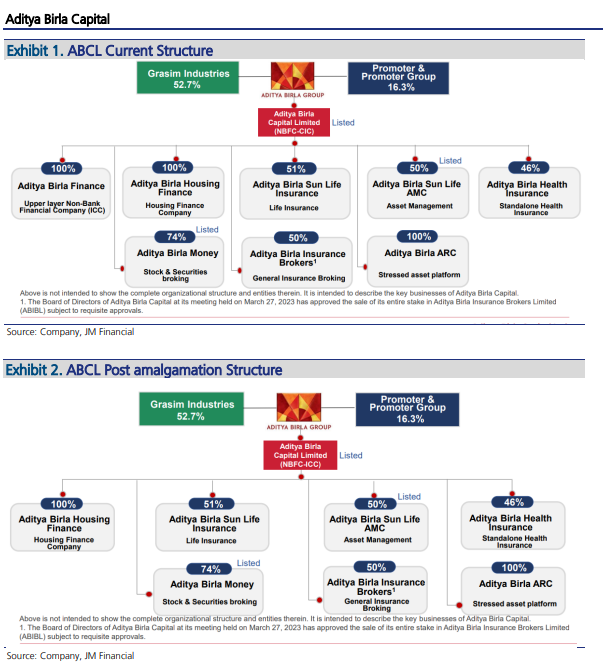

Aditya Birla Capital – A complete Financial Inclusion (10-10-2024)

Subsidiary merger a +ve for Holdco

The RBI released scale-based regulation for NBFCs (October 2021) classifying them into four categories (Base, middle, upper, and top layers). In September 2022, it identified 15 NBFCs, including ABFL, as upper-layer NBFCs. As per the scale-based regulations, upper-layer NBFCs require mandatory listing within three years of identification. Accordingly, ABFL was required to list by September 2025.

The rationale behind amalgamation scheme is:

- a) to comply with RBI’s scale based regulation which mandated ABFL to list as a

separate entity by Sep’25. - b) simplification of organizational structure (less legal entities),

- c) to set up one large finance hub with direct access to capital for the whole

organization (ABFL had to depend on ABCL for raising funds), and - d) business consolidation to offer operational synergies.

The amalgamation is subject to regulatory and other approvals. The process will result in

transfer and vesting of all assets, liabilities and entire business of ABFL with ABCL which

would take ~9-12 months.

Upon the scheme becoming effective, equity investment in ABFL by ABCL (which stands

at INR ~70bn) shall stand cancelled. There will be no change in shareholding,

management and/or control of ABCL. ABCL would continue to hold existing investments

in subsidiaries and associates subject to requisite approvals. Proposed amalgamation is tax

neutral for ABCL and ABFL. The amalgamated entity will have a CRAR ~150bps higher

than the standalone entity.

Source : Jm Financial Company update

Aditya birla sun life insurance

17% VNB CAGR for Insurance arm 15x multiple

Inflation Expected to Cool in September C.P.I. Report (10-10-2024)

The Consumer Price Index is moderating, but September’s report contained both good and bad news for policymakers.

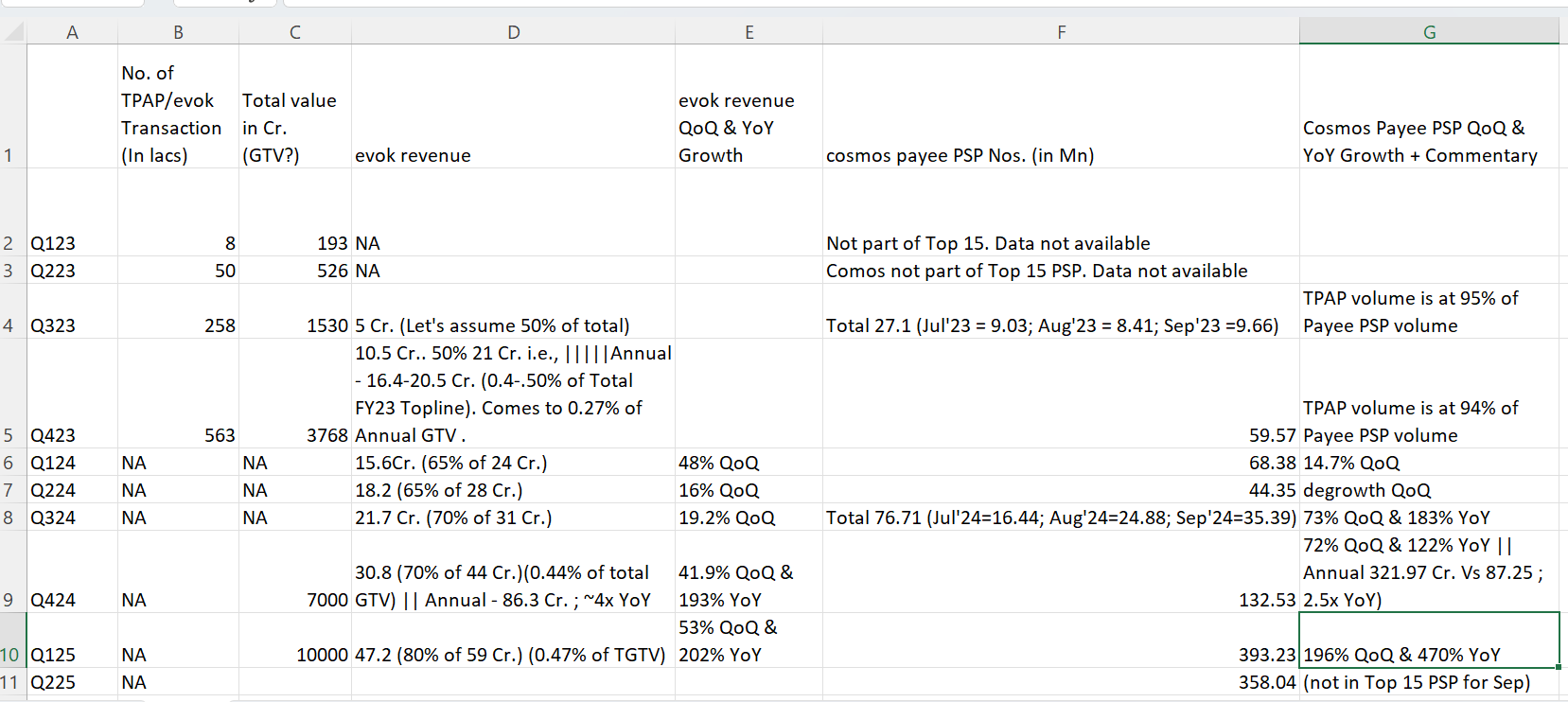

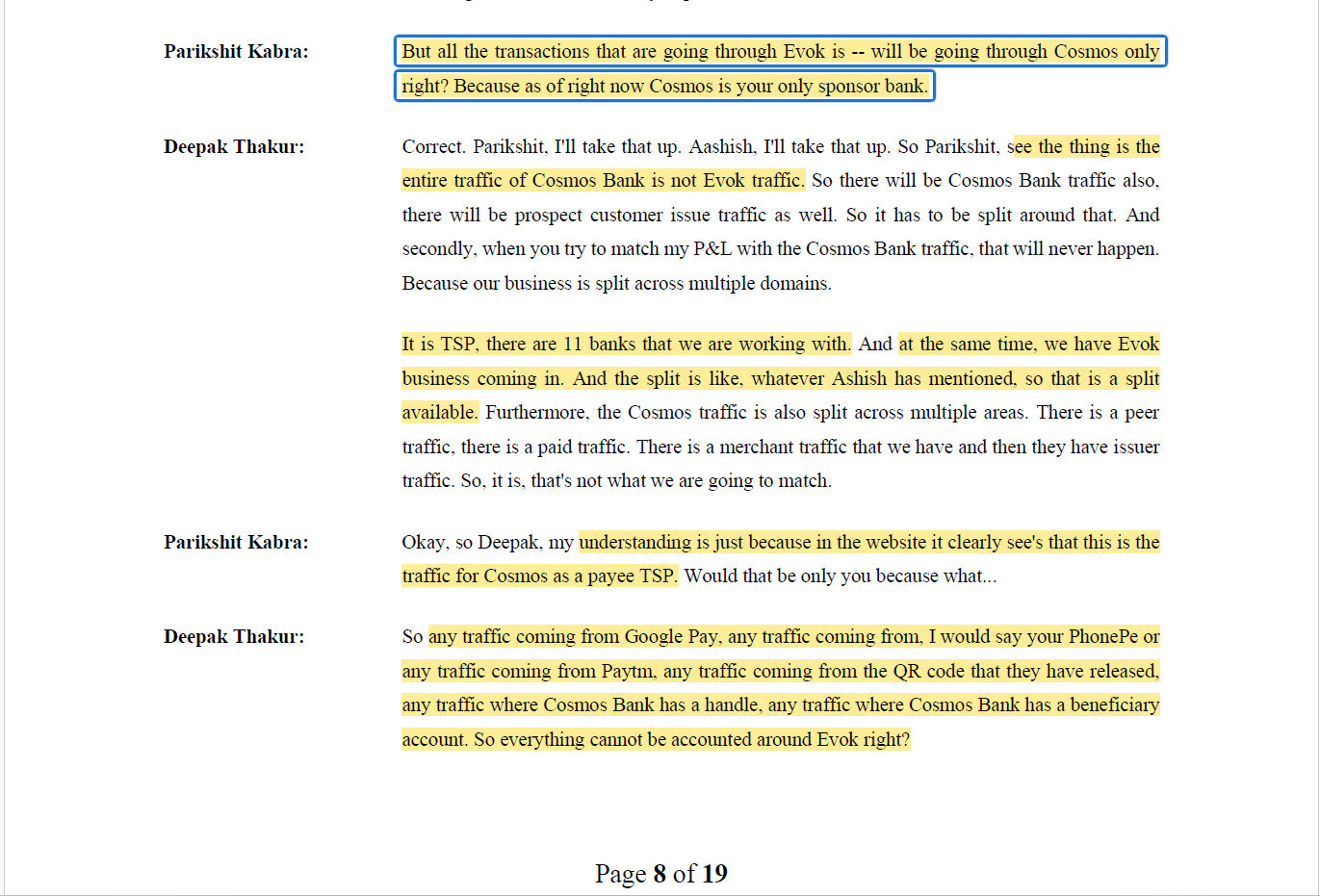

NPST – Technology Provider for UPI Tech (10-10-2024)

Hi Gaurav,

Good Point, but I am not able to reconcile few of the data points, so let’s explore further.

-

Evok was launched around Sep 2022 (Q223). You compared Q324 vs Q323 . But Payee PSP Nos. seems to have grown 183% YoY. (refer my table below). So, didn’t understand from where the 72% came from ?

-

Also, There is no point comparing the cosmos PSP data and total revenue of NPST because of the presence of other piece of business (TSP). We need to compare evok nos. vs Cosmos PSP Payee Nos to arrive at any meaningful correlation or lack of it. But evok revenue data is not readily available.

I have tried to stich together the data based on various sources, mainly calls/ NPCI and company presentation. So let’s explore that. The data is not clean and includes plenty of crude assumption. So feel free to get it clarified where it’s not clear. I wish the data was more beautiful and self explanatory. But for now, it’s not. But i hope it’s closer to truth.

-

Mgmt. is clear that all of Payee PSP Nos. not necessarily reflect the evok transaction volume. But it’s clear that evok transaction volume nos. form part of the Cosmos Payee PSP nos. %age is not clear.

-

Data present in Column B & C used to be provided by NPST in it’s initial 2 Inv Presentations till Q423. Then it was discontinued. However, the GTV (Col. C) was given out in last 2 calls as answers to questions from investors. Clearly it’s one of the most meaningful metric for Evok. Revenue contribution of evok is a %age of that GTV and rest all data is only an approximation to reach at that in absence of direct GTV nos.

-

Column D : evok revenue no. is NOT presented separately by Mgmt. But they keep mentioning the rough/range contribution from evok in almost every call. So, I have used to that to arrive at the evok revenue nos.

-

Column E: Is self explanatory, just the QoQ & YoY growth of evok revenue.

-

Column F: Taken straight from NCPI site. Let me know if you see any discrepancy there.

-

Column G: Self explanatory, Cosomos Payee PSP QoQ & YoY growth with some commentary to explain.

Few of my observations:

- For 2 Qtrs. i.e., Q323 & Q423 where we had both set of data, i.e., TPAP transaction volume & Payee PSP volume. The trend is very clear, evok transaction volume was ~95% of the cosmos PSP Nos. But alas, NPST stopped reporting the data of evok transaction volume from Q124. We can request the mgmt. to report this data in future.

- There is a trend of increase in evok revenue as %age of GTV. It has grown from being 0.23% for Annual FY23 nos. to 0.44% for FY24. Has climbed further to 0.47% in Q125. not sure what’s driving this. This could be a question to Mgmt.

- While it’s hard to pin point a direct 1×1 growth in evok revenue vs Payee PSP volume. The trend is unmistakable. While evok revenue has grown 4x in FY24 vs FY23 the Payee PSP nos. have grown 2.5x for same period.

I think, market might be worried about the degrowth in cosmos Payee PSP nos. for last 2 months, but if the concerns are genuine OR there is some explanation which we aren’t aware of, I guess only time will tell. If there is an explanation and there is no concern on growth, then am ok to hold/buy at this price. However if there are concerns on growth, then just the fact that this Qtrs nos. won’t get impacted big way may not be sufficient reason to support current price. Any inputs ?

Omar elected NC leader, gets support of four independents (10-10-2024)

Omar Abdullah is nominated as the leader of the National Conference legislative party with support from 42 MLAs. Talks with Congress are ongoing to secure backing for government formation in J&K. The combined NC and independent MLAs now total 46 out of 90 seats.