Anant Raj Limited (02-10-2024)

How does that concern you as an shareholder now in 2024?

Anant Raj Limited (02-10-2024)

There is no mention of how the land bank was divided among the companies. Any information regarding that?

Also I heard there was some governance issue in the company among the promoters? Was that pre-demerger group issue or post demerger issue only with anant raj?

Anant Raj Limited (02-10-2024)

Based on my research and limited understanding my conclusion is Anant Raj Limited and TARC are separate identities and have nothing to do with each other.

Ashok Sarin and Anil Sarin are brothers and son of Lala Anant Ram Sarin. The company was divided somewhere in 2018 and Ashok Sarin and family runs Anant Raj Limited and Anil Sarin and family runs TARC.

There are no common promoter in Anant Raj and TARC.

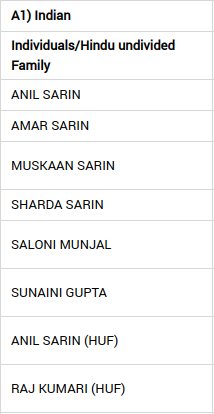

Promotes of Anant Raj Limited –

and promoters of TARC –

Someone who want to deep dive in the scheme of arrangement for division of the company and go through this document –

https://www.primeinfobase.in/z_ANANTRAJ/files/Annexure_3_Audit_Committee_Report.pdf

Listed cos log record operating cash flow (02-10-2024)

Indian companies are generating more cash than ever. The net cash flow from listed firms’ operations hit a new high of Rs 11.1 trillion in financial year 2023-24 (FY24), crossing the Rs 10-trillion mark for the first time, according to the Centre for Monitoring Indian Economy (CMIE) data going back to 1990-91. The FY24 figure represents a 19.3 per cent jump over the previous year, even as quite a few companies are yet to release their numbers.

Zomato – Should you order? (02-10-2024)

Brother,

They might expand into other categories, becoming like Amazon and Flipkart, where you can buy anything. Flipkart’s sales are ₹56,000 crore, yet they burn ₹4,800 crore. Amazon India generates ₹25,000 crore in sales but also loses money.

Imagine Blinkit, without warehouses or a pan-India distribution network, magically reaching Flipkart and Amazon’s sales levels in 10 years. That would mean ₹130,000 crore in sales from this vertical alone.

Based on these assumptions, Zomato and its subsidiaries could generate over ₹200,000 crore in sales, surpassing companies like HUL, Nestle, D-Mart, VBL, and many others. Adding Blinkit’s ₹130,000 crore would bring the total to ₹330,000 crore in sales.

With a 5% profit margin (remember, Amazon and Flipkart are losing money), they could achieve around ₹16,000 crore in profit. Using a price-to-earnings (PE) multiple of 50, their market capitalization would be around ₹8 lakh crore. This could potentially triple your investment, but it comes with significant risk. I doubt Zomato and its subsidiaries can effectively compete against BigBasket, Zepto, Instamart, JioMart, and others.

My assumptions are so absurd and exaggerated that even a child would see through them. They’re merely to highlight the irrationality of some people.

In my opinion, Zomato is unlikely to achieve substantial profits. I personally believe it will follow the path of Reliance Power, Yes Bank, or Unitech.

I urge anyone invested in Zomato to carefully consider these facts and evaluate their holdings.