The demand for copper copper’s conductivity and durability make it indispensable for electrical systems, wind turbines, and solar power generation.

China back to dominating emerging markets as MSCI weight soars (02-10-2024)

In just eight days, China regained the influence it lost over 10 months in emerging markets.

Nucleus software exports limited (02-10-2024)

Just will add another point regarding their new product in upcoming Co-Lending space.

Considering Nucleus reputation with their clients and future of Co Lending, I see this as a good growth handle along with Nucleus efforts to penetrate new global territories.

Current PE of 20 is lucrative and I am betting on a re-rating similar to Oracle Finance.

Although no direct comparison but I feel limited downside and a regular cash generating company with only organic growth is a slow and consistent compounder.

MSTC Ltd.: Growth through to E-Commerce (02-10-2024)

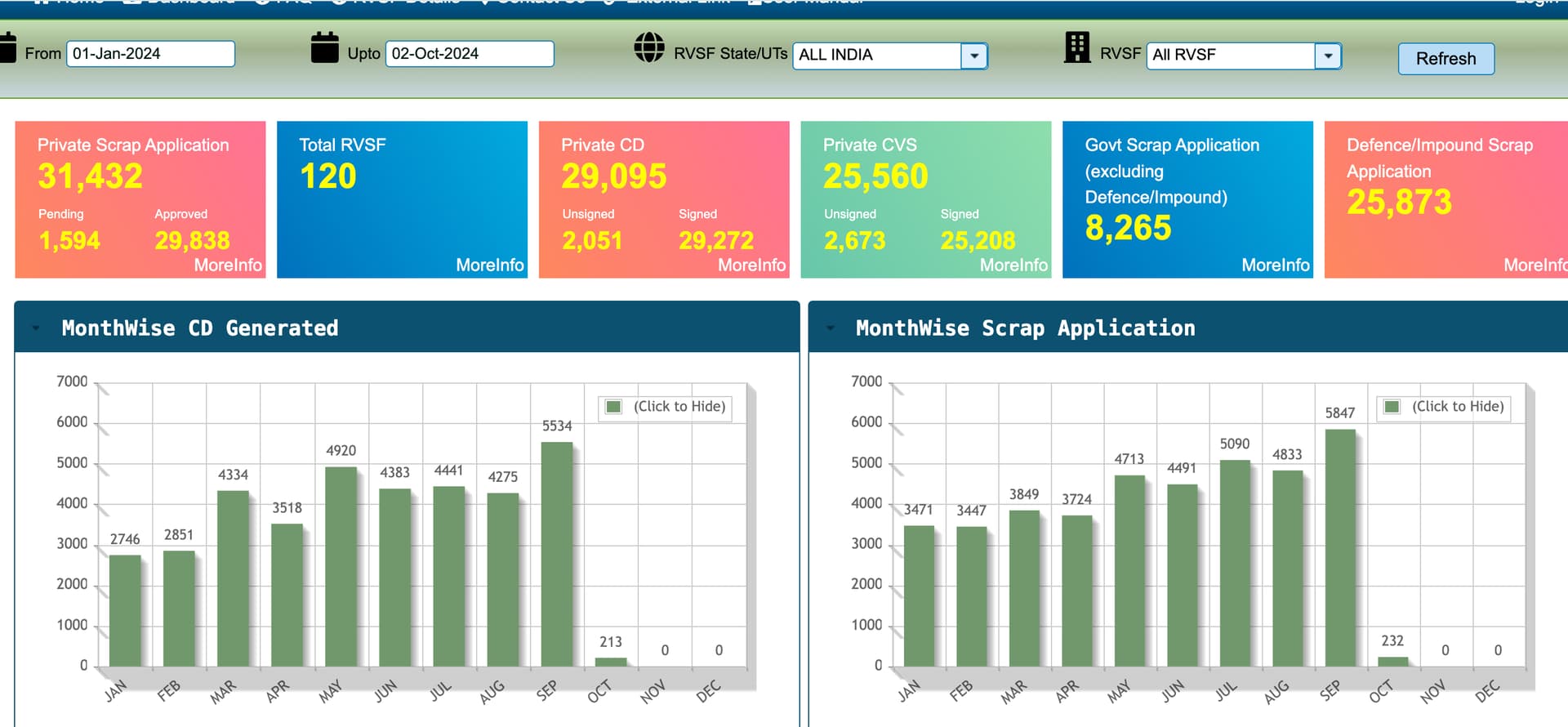

just see the actual data of vehicles scrapped, it comes to 8K vehicles this year, so your assumption of 0.7M vehicles needs to be revisited

Investing the Gandhian way: Principles for a better financial future (02-10-2024)

Six Gandhian principles like self-reliance, goal-focused investing, disciplined SIPs, patience, non-violence, and fostering financial inclusion can guide investors to achieve long-term financial stability and growth.

MSTC Ltd.: Growth through to E-Commerce (02-10-2024)

I took out this year`s scrapping data for CY24, forget about MSTC share but the total vehicles which have come for scrapping to all the 120 facilities all India (Certificate of Deposit) is 31K, whereas MSTC would have a share of around 8K so 35%

too low for any meaningful business profit.

How to register with SEBI as a Research Analyst? (02-10-2024)

Should we have thread for RIA as well? Or it’s not worth it?

Nucleus software exports limited (02-10-2024)

Positives:

- Nucleus releases a new module/update every year increasing value of product

- Being in fixed price contracts, the price escalations take time while wage inflation impacts EBITDA margins

- The contracts are usually 3-7 years long, with repricing followed at the end of the life

- Considering 2022 as the year of reprising and low EBITDA margins due to “The Great Resignation”, the same repricing can be considered to occur from 2025 to 2029

- The price charts reflect this growth over past 15 years with a flat to downward trend followed by a lumpy growth period

- ~Rs 500 crores of cash is 16.67% of the MV with no debt, allows for a downside safety in current market conditions

- The company has de-risked its business in terms of customer concentration, dependence on export sales, etc

Negatives:

- The CFO is low considering this being a tech company as the receivables is high, and the CFO could have been increased by using working capital

- The working capital to increase CFO will increase valuations and improve cost of capital, but the company is debt averse and holds cash

- The foreign subsidiaries do not make CFO as can be seen in their reported financials

- The company is dependent on BFSI doing well along with IT, both being neglected by the market

- Promoter selling stake in recent buyback, which is understandable by the fact that the promoter stake is very close to 75%. Arun Jain in non-promoter can be considered a promoter since he is with the company since 1990s. Therefore total stake is 74.3% which should come down after buyback

All-in-all, if the company is available at a good PE can purchase and hold for 4-5 years (2029) to see returns

Key US short-term rate surges amid month-end turbulence (02-10-2024)

The Secured Overnight Financing Rate (SOFR) significantly increased to 4.96% on Monday, indicating tighter liquidity in money markets at the end of the quarter. This rise signals heightened funding pressure, with analysts noting that banks’ balance sheet capacity is more constrained and expensive than expected.