Ms. Nuzzi, a former writer for New York magazine embroiled in a scandal involving Robert F. Kennedy Jr., had accused her ex-fiancé of harassment and blackmail.

Microcap momentum portfolio (12-11-2024)

Let’s brainstorm as I have built something on the similar lines.

Antony Waste – Long Term (12-11-2024)

Hi All,

I hold Antony Waste & I got a question after listening to the last concall. The current ROCE is 14% & the management says it’s not going to increase due to the capital intensity of the business. ROE is around 16% & the management stated that it will come down to 9% levels. Management is guiding for ~25% growth in the topline & said that the OPM will stay around 23% over the next 3-4 years. Debt levels as per my understanding of the past & their future guidance, management is consecutive & thus, debt should remain low to nill. In that case, can we model it like below over the next 2 years? Due to the return ratios either staying stable or coming down & the very high dependence on the small governments, the business may not be able to command higher valuations unless the revenue mix tilts more towards higher margin projects (waste processing, vehicle scrapping, waste to energy, etc).

Revenue after 2 years at 25% cagr comes to ~1450 Cr.

EBITDA at 23% margin, comes to ~330 Cr.

Interest + Dep ~110 Cr.

PBT ~220

PAT ~154

EPS (provided same share count) ~54

PE remaining between 15-25:

15 PE: ~770

20 PE: ~1080

25 PE: ~1350

So questions :

- Does it make sense to have such businesses where the probability of better profitability, return ratios over 5 years is low, in our core portfolio?

- CnT business seems a commodity & can face steep competition even from small regional players then does the management have the capability to venture into the new value added areas?

- It seems that even valuation of sub 20 levels is not cheao for these businesses, what should be a good margin of safety?

Please reply as much as you all can to enlighten all of us. ![]()

Can Trump Prevent a TikTok Ban? His Team Says ‘He Will Deliver’ (12-11-2024)

When asked about whether President-elect Donald Trump would prevent a TikTok ban in the United States, a spokeswoman told The New York Times: “He will deliver.”

Volkswagen and Rivian Form Joint Venture, Deepening Alliance (12-11-2024)

The new agreement builds on an earlier announcement in which the German automaker said it would invest up to $5 billion in Rivian, a maker of electric vehicles. The new venture brings them closer.

US Regulators Seek to Block UnitedHealth’s $3.3 Billion Purchase of Home Care Company (12-11-2024)

The Justice Department and four Democratic state attorneys general argued that United’s takeover would limit competition and harm consumers needing home or hospice care.

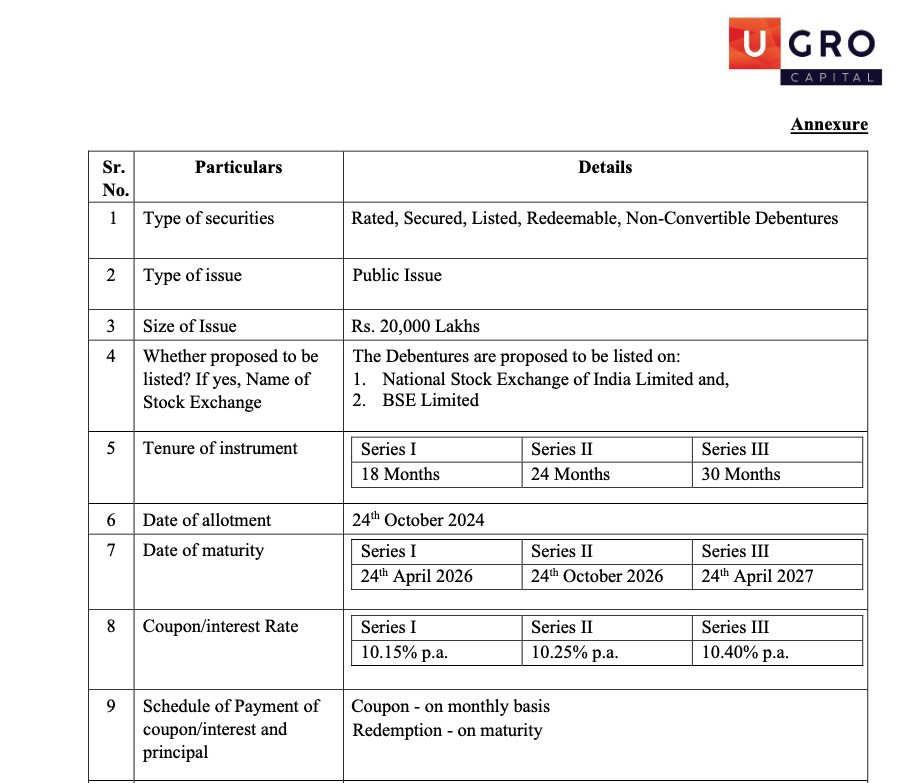

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (12-11-2024)

YTM is a complicated calculation and fluctuate overtime. It’s calculated after discounting the future coupon payment. Kinda DCF method.

I would just focus on annual coupon rate. Post rating upgrade, it’s evident that their incremental CoB has been reduced. Since, only new funds are being borrowed at the lower rate and the older borrowing was at higher rate, it will still take some to see the material change on the aggregate CoB.

Attaching screenshot of the recent fund raised via allocating 200cr worth of NCDs in October 2024. Check for yourself the Coupon rate, which is materially lower than the aggregate CoB.

Why Trump’s Victory Is Fueling a Market Frenzy (12-11-2024)

Investors have been comforted by a clear election result and are anticipating tax cuts and deregulation from a second Trump administration.

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (12-11-2024)

Thank you for clarifying the distinction between Yield to Maturity (YTM) and the annual coupon rate. You may be right regarding the current coupon rate being below the aggregate cost of borrowing at 10.7%.

However, I noticed that previous bonds were trading at less than 11% YTM, whereas these new bonds are now offering an 11.5% YTM. Doesn’t this indicate an increase in the cost of borrowing compared to past issuances? This higher YTM could reflect a shift in market conditions or perhaps a change in U Gro’s funding strategy.

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (12-11-2024)

@Akash_Padhiyar I think you miss-understood the concept of yield to maturity. It is not same as Annual Coupon Rate or annual yield.

The annual coupon rate here is approx. 10.5%. On the contrary, the cost of borrowing here is lower than their current aggregate CoB which is 10.7% (as per Q2 earnings).

Community please feel free to correct me, if you disagree!