can u give detailed calculations for the specter

how to use this extension, interpretation I mean?

Posts tagged Value Pickr

Screener Specter – Companion for screener.in (15-08-2024)

Kilburn Engineering – Huge undervaluation (15-08-2024)

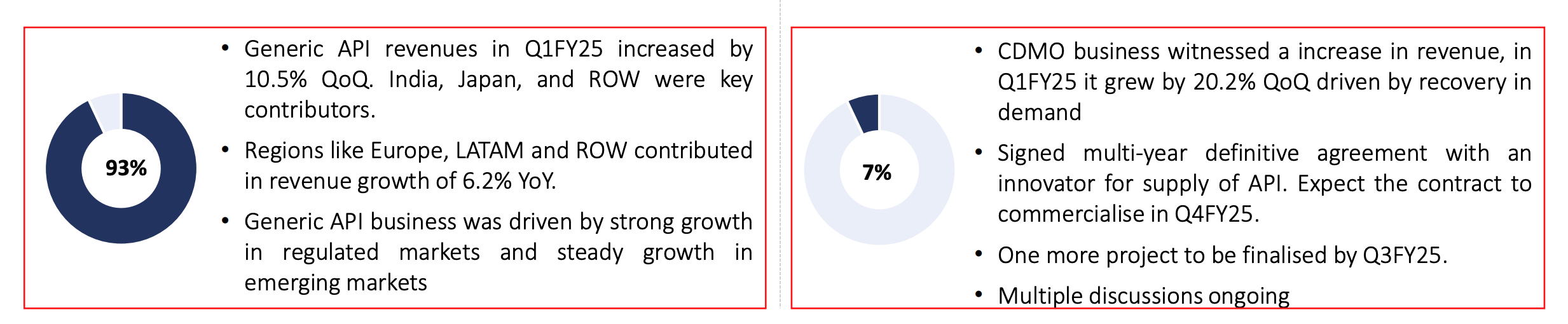

Notes from Q1 FY 25 call

- Q1 FY 25 Standalone revenue: 64 Cr, Consol. revenue (post-acquisition of ME Energy) at 85 Cr

- Total order book 370 cr

- 50-60% of the order book comprises repeat customers, indicating strong client relationships and satisfaction.

- Deferred orders impacting revenue: Two orders delayed, worth approx. ₹40 crores

- Enquiry pipeline is 2000 cr +

- Focusing on projects with higher revenue and higher margins

-

At a group level, order intake of 500 cr expected for whole year

-

Capex outlook

- 5 to 10 cr for M.E. Energy

- 22 cr to acquire additional factory unit

- Acquisition of factory unit in Ambernath for 22 cr, subject to due diligence

- Expected revenue of ₹100 crores.

- Process likely to be completed in 2-3 months

-

With the acquisition of additional factory unit, some of projects being executed from existing Kilburn plant likely to move there and the core Kilburn plant likely to be used for more value added projects like – manufacturing of titanium equipment to be used in defence and other customized equipment

-

Guidance of 500 cr revenue and 20%+ profitability on consolidated basis for FY 25

- Due to economies of scale and operating efficiencies

- Ability to scale up to 700 to 750 cr of revenue in the next 3 years or so –

- Depending on the order mix that company gets though

Disc: Invested from lower levels, biased

Sky Gold ltd. – Will it reach the sky? (15-08-2024)

Below is the concall by Sky Gold.

Sky Gold Ltd Q1 FY2024-25 Earnings Conference Call

I hope you find it useful.

This one latest YouTube video covering Sky Gold

Sky Gold – The No.1 Jewellry Stock | Sky Gold Stock Analysis | Sky Gold Q1FY25 Result Analysis

And here is the latest Nuvama report of Sky Gold

https://www.nuvamawealth.com/research/stock-specific-reports-1/sky-gold–q1fy25-result-update-ef968c

Now my personal opinion – It’s just a wild thought. I am trying to kind of ’ CONNECT THE DOTS’

Sky Gold can be / may be the Dixon Tech. of the Indian Jewellery industry.

This means it has a similar business model and has the same 3-5% OPM.

Yes. This OPM is less, but mind you, this kind of works as an entry barrier for new players.

At present, there are hardly any institutional holdings. So if it delivers above-average sales growth, it can become the next Dixon tech.

This also has a large size of opportunity and long runway as Bharat Shah sir says.

Negatives – Large borrowings, negative cash flow, equity dilution due to recent fund raising.

Just my personal opinion.

Not invested but biased. May invest in future.

dr.vikas

Red Tape Ltd. – The next fashion giant? (15-08-2024)

Honestly what frustrates is company’s lack of quarterly presentations and concalls. For the brand RedTape is (I liked redtape leather shoes from early 2000s), they need to improve their IR big time. AGM cannot be the only place to interact with management.

We don’t know how Bangladesh issue would impact them either. I hope inventory provide(d) some buffer this quarter(??).

Arman Financial Services Ltd (15-08-2024)

Results q1 fy25

86f22aa3-d9e3-4303-a027-a6ee05cff09e.pdf (2.8 MB)

Piccadily Agro Industries Ltd (15-08-2024)

That is the age of the cask not the age of the liquid inside. Brand new casks are very rarely used for aging whisky. Most probably never. There are things you can age in brand new casks and there are things you “cannot” age in brand new casks. Single malt whisky is one of them. Bourbon is always aged in brand new oak casks. Most of the time whisky distillers buy used casks from the United States that was once used for aging bourbon (like Jack Daniels) so that some of the flavor of bourbon is passed on to the whisky. That is why you hear terms like ex bourbon, ex sherry ex wine etc. A finished product is often a blend from ex bourbon, ex sherry, ex wine casks.

PS : Wishing all our members a very happy Independence Day.

Glenmark Life Sciences (15-08-2024)

Yes. GLS may be re-rated now after the management change.

The simple thing was that with GP promoters, GLS was mainly a CMO and now it’s trying to become CDMO. But it has a very ‘LONG LONG’ way to go. Check below the CMO & CDMO percentages of sales.

This is taken from the Aug 24 Investor Presentation.

Currently not invested.

dr.vikas

Aptus Value Housing : Is valuation justified or just another HFC? (14-08-2024)

Thanks @Shivam_Jindal for the detailed response. You are right in highlighting why the stock price has been correcting. I agree with you on the same. I am not so much focused on the stock price as long Aptus is not short on liquidity

My question was whether Aptus is likely to face any liquidity crunch as banks and nhb are big sources of capital. While Aptus is well capitalised at the moment I understand nhb refinancing happens every year after an audit exercise by the nhb team. Would that be seen as a risk going forward. It may not be so.

The management does seem seasoned and conservative in underwriting (and control over NPAs), and gearing is low as compared too others.

PS: took a meaningful position in Aptus yesterday.

Red Tape Ltd. – The next fashion giant? (14-08-2024)

Crisil rating also revised to positive

Aptus Value Housing : Is valuation justified or just another HFC? (14-08-2024)

@Pulak I think the overhang due to the mentioned large investor sell off is bringing down the price. This generally happens with all IPOs 2-3 years into the listing. Early PE investors sell their stake.

Another reason for weakness is sector sentiment. NBFCs and all banks are going through this because the banks are going through slow deposit growth phase. I am not sure if you had followed this whole discussion on people moving from term deposits to equities. If banks face this pressure they are going to cut down on their lending to NBFCs. Aptus borrows from banks and the exposure is probably 15-20%. There was a news article as well on this issue, just google it.

Lastly, I can see concerns in unsecured lending (microfinance) as NPAs are slowly rising and RBI issued a circular few weeks back on microfinance. Though this should not apply to Aptus as much because its dominantly a HFC. Their SME financing is also collateralized probably as I remember they mentioned LTV on these loans of 42% (need to check again this).

I think once the market sentiment improves its going to be a clear value buy, aptus at 300 is super cheap. They are growing AUM at 30%.

Disclosure: invested and biased