Posts tagged Value Pickr

Sirca Paints India Limited (11-08-2024)

Demand for wood coatings was significantly impacted during the quarter primarily because of General Elections and severe heat wave across North India which delayed the ongoing recovery in the residential real estate sector and renovation activities. April and May month was quite weak as labour has gone back to their respective places due to heat wave and general elections. However we saw

gradual recovery in demand from June onwards and improvement in market sentiments which is still continuing.

Our sales has grown from INR 73 cr to 79 cr ( increase of 7% y-oy) , EBITDA has contracted from INR 17 Cr to 14 Cr ( y-oy ) and PAT has contracted from INR 13 Cr to 10.20 Cr ( y-oy ).Ebitda margin has contracted from 20% to 18% ( q-oq ) primarily due to unreasonably high one off expense in logistics cost ( 2-2.5 Cr ) of shifting our Centralised Mother Warehouse ( carrying 80% of inventory ) from existing location to a new location within a short span of time frame ( 15 days ) because of closure of chemical units in that particular area by state govt. Adjusting for this one off impact our EBITDA margins have improved from 20% to 21% ( q-q ) which is very well within our guidance range.

Our acquisition of Welcome Brand and JV with Oikos is shaping up well with our strategy of growing these 2 brands in a meaningful manner going forward. We expect these 2 segments to play a big role in Sirca’s growth story in next 3 years with a more focus on premium products and expanding our distribution network to enter into new markets and capture more market share.

Rudra’s PF and Information attic (11-08-2024)

Import note from Delhivery CEO on quick commerce and why it will have huge challenges sustaining the current growth rate once the $40-50 million monthly burn reduces

Rudra’s PF and Information attic (11-08-2024)

Coming from Sanjeev Sanyal this assumes significance as EPFO will have an elevated role in the overall economic strategy and skill development

Rudra’s PF and Information attic (11-08-2024)

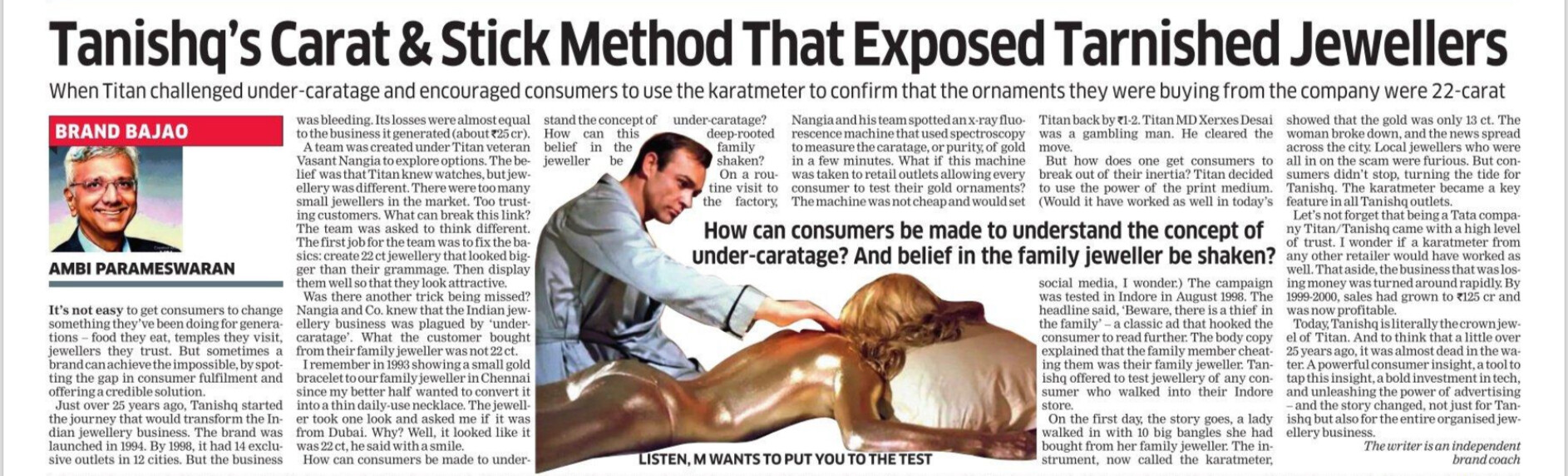

An interesting read on how Tanishq created awareness and shift from Unorganized to Organized in Gold Jewellery retailing

Vishnu prakash R Punglia LTD(VPRPL)-“Steering India’s Water Management Future” (11-08-2024)

Ok. I was under that impression. Thanks for bringing clarity.

Shivalik Bimetal Controls Ltd (SBCL) (11-08-2024)

After some more reading and speaking to some-people involved in the value chain, the understanding I have is that:

- There is a tech-edge and barriers to entry when it comes to the Auto business (as there is a long approval process and products are also more sophisticated)

- Same true for their bimetal business esp when they are supplying to the likes of Scheider etc

Though, when it comes to enery meters (and smart meters) it seems that there could be some local competition that may emerge. Also companies might still import from China as it works out to be cheaper even after duties.

Would be keen to gather thoughts from others on these.

Shivalik Bimetal Controls Ltd (SBCL) (11-08-2024)

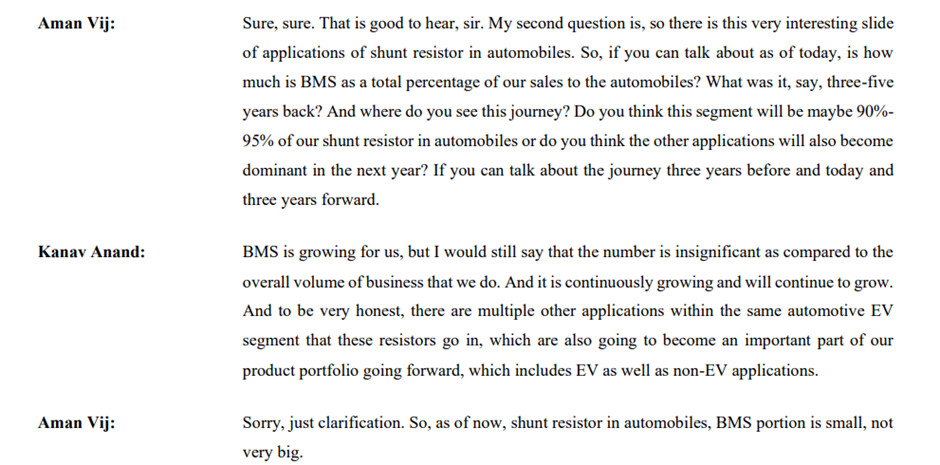

A quick question here: company in some of the earlier calls had mentioned that Shunts revenue coming from BMS applications is quite small (from Mar-23 call) but since then some of the posts had mentioned that BMS’s contribution within shunts revenue is quite high. any one can please clarify this anamoly?

RACL Geartech Limited (11-08-2024)

-

RACL Geartech Limited held its Q4 FY2023-24 earnings conference call on June 21, 2024

-

Completed shift of Noida plant to a larger 32,000 sq ft facility without production loss

-

Investing in Project Titan to become a Tier 1 supplier for a premium German car manufacturer

-

Creating buffer capacity in gear grinding to avoid previous year’s constraints

-

Focusing on growing domestic business to improve working capital cycle

-

Continued focus on exports (73% of revenue) despite longer working capital cycles

-

Investing ahead of demand for future projects like electric vehicles

-

Adding new customers every 2-3 years to supplement organic growth

-

Growing opportunities in passenger vehicles and commercial vehicles segments

-

Shift of manufacturing from Europe to India by global players like ZF

-

Some weakness in European demand and inventory corrections

-

Challenges in availability of skilled manpower

Revenue Growth and Margins:

-

FY24 revenue of ₹423 crores, up 15% YoY

-

EBITDA margin of 24.09% in FY24, slightly down from 24.69% in FY23

-

Targeting revenue of ₹550 crores for FY25, implying 30% YoY growth

-

Working capital cycle: Management stated higher cycle is factored into product costing

-

Dividend policy: Small dividend maintained for investor sentiment despite growth phase

-

Capacity constraints: New investments made to create buffer capacity

-

Revenue target of ₹550 crores for FY25

-

EBITDA margin guidance of 20-23% range as business scales up

-

Capex plan of ₹60 crores for FY25

-

Focus on reducing long-term debt in FY25

-

Capex of ₹60 crores planned, substantial portion for Project Titan

-

Opportunities in passenger and commercial vehicle segments

-

Risk of continued working capital pressure due to export focus

scales

The Anti-Portfolio (11-08-2024)

Appreciation in house value is 90%, and in folio value is 200%, pretty good margin, over past 3 years. ![]()