Hi Vikas,

Thanks for sharing this. On a lighter note, what has been the appreciation in house value in percentage terms? I’m sure you are better off having invested in the market than buying a house 3 years ago ![]()

Hi Vikas,

Thanks for sharing this. On a lighter note, what has been the appreciation in house value in percentage terms? I’m sure you are better off having invested in the market than buying a house 3 years ago ![]()

hi,

thanks for wonderful reply

Brigade Enterprises Q1 FY25 Analysis: Key takeaways!!

Brigade Enterprises reported solid performance in Q1 FY2025, driven primarily by its real estate segment. The company achieved real estate sales of 1.15 million square feet with a sales value of INR 1,086 crores at an average realization of INR 9,483 per square foot, which is their highest to date. This reflects strong demand for premium properties with spacious layouts and high-end amenities. The company’s multi-domain approach across residential, commercial, hospitality, and retail segments positions it well to capitalize on various market opportunities.

Strategic Initiatives:

Trends and Themes:

Industry Tailwinds:

Industry Headwinds:

Analyst Concerns and Management Response:

Competitive Landscape:

Brigade’s focus on premium projects and diversified portfolio helps differentiate it from competitors. The company’s strong brand presence in South Indian markets, particularly Bangalore, provides a competitive edge.

Guidance and Outlook:

The company maintained its previous outlook on project launches. Management expects the launch trajectory to remain similar to previous quarters, with more activity in the second half of the fiscal year.

Capital Allocation Strategy:

Brigade continues to invest in land acquisitions and new project launches across segments. The company maintains a balanced approach between residential, commercial, and hospitality investments.

Opportunities & Risks:

Opportunities:

Risks:

Regulatory Environment:

The recent announcement of indexation benefit for capital gains on realty investments is seen as a positive move for the sector.

Customer Sentiment:

Customer sentiment appears strong, with continued demand for both residential and commercial properties. The trend towards premiumization indicates customer willingness to invest in higher-quality projects.

Top 3 Takeaways:

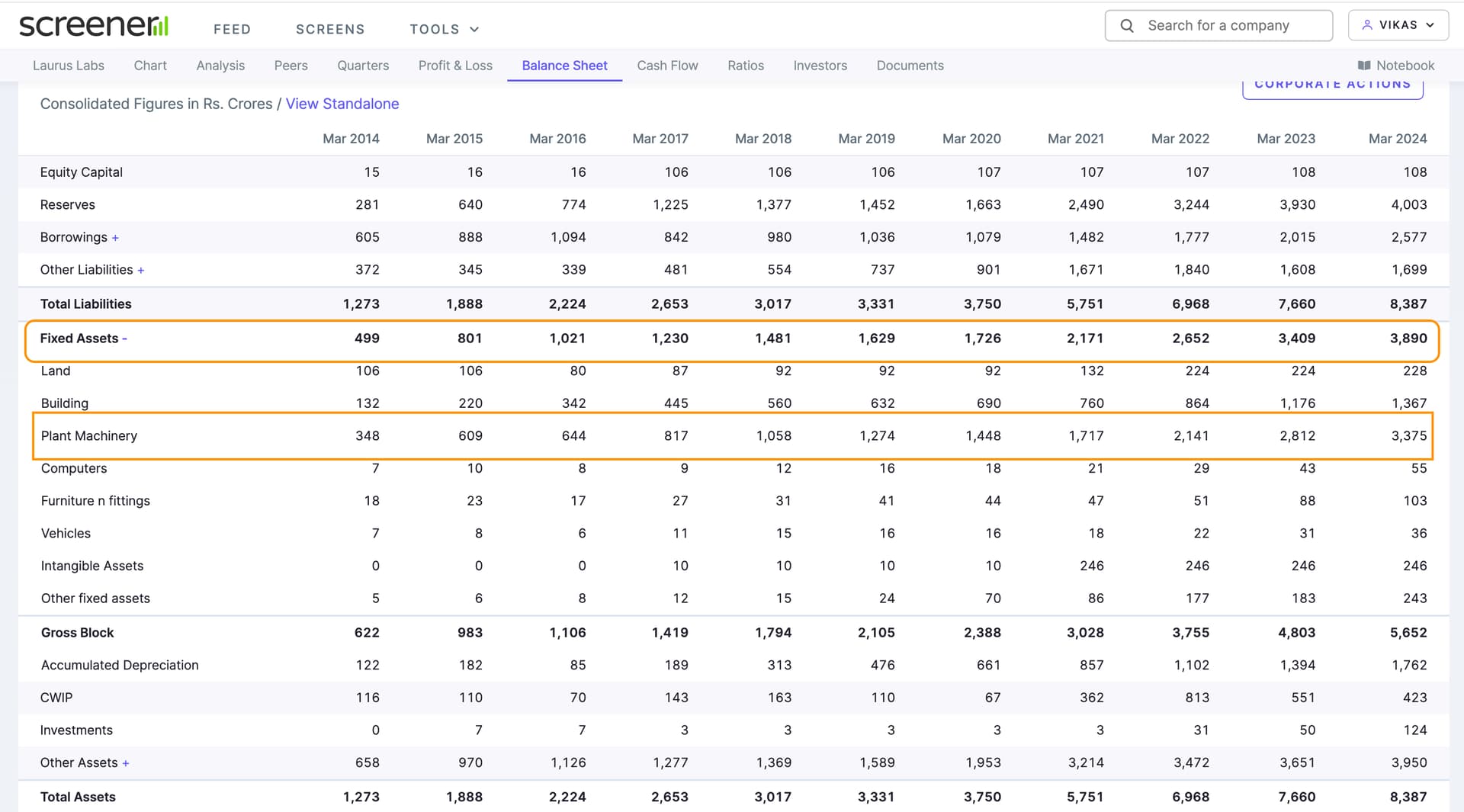

This is looking marvellous on the balance sheet.

But when will it convert into earnings in the big Q!!!

dr.vikas

Praveg business model from Sep to Feb (6 months), so good revenue Quarter Q3 and Q2 and Q4, 70-75% as compared to Q3. If Q3 will be poor, at that point is the addressable!!!

Has been trying to analyze the company after recent runup as it has become > 10% of my PF.

Looks like this still has a long-runway ahead. Reports predict 9.3-18.4% growth in core banking software till 2030.

Also, OFSS has only 6.5-8% market share based on above reports.

Another +ve point is that OFSS has insignificant market share in US which is 50% of global market. OFSS is likely to gain market share supported by its parent.

Given above scenario, OFSS can easily clock 10-12% of revenue and 15% of profit growth for next decade.

Here is an interview with Srinivasa Reddy, good insights. Enjoy.

#S2E1 I Synergy Green : Is Wind Energy the next breakout? I Srinivasa Reddy

And the Corporate Video:

Here is an interview with Srinivasa Reddy, good insights. Enjoy.

#S2E1 I Synergy Green : Is Wind Energy the next breakout? I Srinivasa Reddy

And the Corporate Video:

Barbeque-Nation Q1 FY25 Analysis: Key takeaways!!

Barbeque-Nation faced a challenging operating environment in Q1 FY25, with negative same-store sales growth (SSSG) of 7.4%. However, the company is seeing gradual month-on-month improvement in SSSG numbers over the last 4 months. Management expects things to improve further during the rest of the year, particularly from Q3 onwards. The company remains focused on maintaining best-in-category guest experience to drive dine-in footfalls.

Strategic Initiatives:

Trends and Themes:

Industry Tailwinds:

Industry Headwinds:

Analyst Concerns and Management Response:

Concern: Negative SSSG and its impact on profitability.

Response: Management highlighted improving trends in recent months and expects further improvement from Q3. They are focusing on cost control measures to mitigate the impact of negative operating leverage.

Concern: Impact of rising vegetable prices on margins.

Response: Management clarified that vegetables form a small part of their overall purchase basket, and the impact on gross margins is minimal. The meat basket (chicken, prawn, mutton, fish) has a more significant impact on margins.

Competitive Landscape:

The company faces increased competition in the casual dining segment. However, Barbeque-Nation believes its strong tech-driven backend processes give it an advantage in scaling brands efficiently.

Guidance and Outlook:

Capital Allocation Strategy:

The company is focusing on maintaining robust EBITDA to cash conversion. They delivered around INR 20 crores of cash profit in Q1, an increase of 17.4% compared to the same period last year.

Opportunities & Risks:

Opportunities:

Risks:

Customer Sentiment:

Management noted a shift towards premium dining experiences, while value segments face pressure due to inflationary impacts on consumer spending.

Top 3 Takeaways:

Barbeque-Nation Q1 FY25 Analysis: Key takeaways!!

Barbeque-Nation faced a challenging operating environment in Q1 FY25, with negative same-store sales growth (SSSG) of 7.4%. However, the company is seeing gradual month-on-month improvement in SSSG numbers over the last 4 months. Management expects things to improve further during the rest of the year, particularly from Q3 onwards. The company remains focused on maintaining best-in-category guest experience to drive dine-in footfalls.

Strategic Initiatives:

Trends and Themes:

Industry Tailwinds:

Industry Headwinds:

Analyst Concerns and Management Response:

Concern: Negative SSSG and its impact on profitability.

Response: Management highlighted improving trends in recent months and expects further improvement from Q3. They are focusing on cost control measures to mitigate the impact of negative operating leverage.

Concern: Impact of rising vegetable prices on margins.

Response: Management clarified that vegetables form a small part of their overall purchase basket, and the impact on gross margins is minimal. The meat basket (chicken, prawn, mutton, fish) has a more significant impact on margins.

Competitive Landscape:

The company faces increased competition in the casual dining segment. However, Barbeque-Nation believes its strong tech-driven backend processes give it an advantage in scaling brands efficiently.

Guidance and Outlook:

Capital Allocation Strategy:

The company is focusing on maintaining robust EBITDA to cash conversion. They delivered around INR 20 crores of cash profit in Q1, an increase of 17.4% compared to the same period last year.

Opportunities & Risks:

Opportunities:

Risks:

Customer Sentiment:

Management noted a shift towards premium dining experiences, while value segments face pressure due to inflationary impacts on consumer spending.

Top 3 Takeaways: