Posts tagged Value Pickr

Awfis Space Solutions: Flexing its Muscles in the Market (10-08-2024)

Financials & disclosure of your holding is missing. Please add the same.

TechnoFunda with anshu (10-08-2024)

We already have few threads on this. Please move your posts there as this thread will be deleted in two days.

Kovai Medical Center and Hospital – Health and Wealth (10-08-2024)

LOOKS JUSTIFIED

20000 rs per sq ft for highway plot in metro is very reasonable.=110 cr

plus 30 cr construction cost assuming 50% construction ,7floors + basement.

DELHIVERY – One stop solution for shipping and parcel delivery (10-08-2024)

Dabur India Q1 FY2025 Analysis: Key takeaways!!

Business Outlook:

- Delhivery had a steady and profitable start to the fiscal year, with revenue growth of 13% Y-o-Y and improved profitability across core businesses.

- Express Parcel service maintained stable EBITDA margins at 18%, while Part Truckload (PTL) business saw continued improvement in service EBITDA margins to 3.2%.

- Supply Chain Services (SCS) business grew 26% Y-o-Y, driven by a seasonally strong quarter for air conditioning customers.

Strategic Initiatives:

- Delhivery is launching a network of shared dark store warehousing to cater to the growing quick commerce opportunity, providing multi-tenant fulfillment and rapid local delivery services.

- The company is also expanding its franchise network to deepen its reach and capture SME volumes across India.

- Delhivery is focusing on integrating its PTL and Express networks to drive synergies and improve cost efficiencies.

Trends and Themes:

- The e-commerce industry is seeing a shift, with some players like Meesho insourcing a portion of their logistics.

- The PTL market in India is highly fragmented, presenting an opportunity for Delhivery to capitalize on the industry’s movement towards formalization.

- Demand for integrated supply chain services, including B2C and B2B offerings, is on the rise.

Industry Tailwinds:

- The continued growth of e-commerce and the need for reliable, high-quality logistics services.

- Increasing focus on supply chain optimization and integration among businesses.

- Ongoing shift from unorganized to organized players in the logistics industry.

Industry Headwinds:

- Volatility in the e-commerce industry, with some players insourcing logistics operations.

- Potential pricing pressure from traditional logistics players in the D2C segment.

- Uncertainty around the long-term strategy of key customers like Meesho.

Analyst Concerns and Management Response:

- Analysts were concerned about the impact of Meesho’s insourcing on Delhivery’s volumes and market share. Management highlighted that Delhivery remains a reliable and cost-effective partner for all its customers, and the company is focused on diversifying its customer base and expanding its service offerings.

Competitive Landscape:

- Delhivery maintains its position as the largest 3PL player in the market, with a strong integrated network and a diversified customer base.

- The company is differentiating itself through its technology-enabled solutions, multi-tenant fulfillment capabilities, and ability to provide end-to-end supply chain services.

Guidance and Outlook:

- Delhivery expects continued growth in its steady-state volumes, in line with the overall e-commerce market growth of 15-20% annually.

- The company is confident about its ability to maintain stable EBITDA margins in the Express Parcel business and improve margins in the PTL and SCS segments.

Capital Allocation Strategy:

- Delhivery is focused on optimizing its existing network and infrastructure, with no significant capacity additions planned in the near term.

- The company is investing in technology and automation to drive operational efficiencies and improve profitability.

Opportunities & Risks:

- Opportunities: Expanding its presence in the PTL market, capitalizing on the quick commerce opportunity, and leveraging its integrated network to cross-sell services.

- Risks: Volatility in e-commerce volumes, potential pricing pressures, and uncertainty around the strategies of key customers.

Customer Sentiment:

- Delhivery continues to maintain a strong relationship with its diverse customer base, with the number of customers increasing from 33,000 to 35,000 in the quarter.

Top 3 Takeaways:

- Delhivery’s diversified business model, with strong performance across Express Parcel, PTL, and SCS segments, positions the company well to navigate industry challenges.

- The company’s strategic initiatives, such as the dark store network and franchise expansion, demonstrate its ability to identify and capitalize on emerging opportunities.

- Delhivery’s focus on operational efficiency, technology integration, and a customer-centric approach suggest a positive long-term outlook, despite some near-term industry headwinds.

Trent — A value unlocking story from the house of TATA (10-08-2024)

What a performance. Good growth across formats.

Getting seriously difficult to sell this one.

Dabur: “Chawyanprash” with characteristic of “Real” “honey”, improving quality with age (10-08-2024)

Dabur India Q1 FY2025 Analysis: Key takeaways!!

Dabur India demonstrated solid performance in Q1 FY2025, with consolidated revenue growing by 9.8% in constant currency and 7% in INR terms. The India business, including Badshah, grew by 7.3%, underpinned by volume growth of 5.2%. The company’s diversified portfolio continued to thrive, achieving market share gains in 95% of its product categories. The International business exhibited strong growth of 18.4% in constant currency terms, backed by market share gains in most categories.

Strategic Initiatives:

-

Portfolio Diversification: Dabur is focusing on expanding its total addressable market (TAM) by introducing new products and entering new categories. For example, the company launched Hajmola Mr. Aam, extended Odomos into the LVP segment, and introduced Odonil in various formats beyond PDCB blocks.

-

Distribution Expansion: The company added 50,000 outlets to its direct reach and increased its presence in 21,000 additional villages. It also added 3,300 Yoddhas (rural sales representatives) to strengthen its rural distribution network.

-

Premiumization: Dabur is working on introducing premium offerings in various categories, including Oral Care, to improve its product mix and margins.

-

Digital Focus: The company has increased its digital advertising spend to more than 30% of overall media spends, reflecting its focus on reaching consumers through digital channels.

Trends and Themes:

-

Rural Recovery: Dabur is witnessing a gradual pickup in rural markets, with sequential improvement in volume growth over the past three quarters.

-

E-commerce and Modern Trade Growth: These emerging channels posted robust double-digit growth and now contribute to around 20% of Dabur’s India business.

-

Health and Wellness: The company continues to see strong demand for health supplements and ayurvedic products, reflecting the ongoing trend of health-conscious consumer behavior.

Industry Tailwinds:

-

Favorable Government Policies: Rural-centric budget initiatives focusing on infrastructure, agriculture, and employment are expected to boost rural demand.

-

Normal Monsoon: The timely arrival of monsoon is expected to have a positive impact on rural consumption.

-

Declining Inflation: The moderation in inflation is expected to improve consumer sentiment and drive demand.

Industry Headwinds:

-

Competitive Intensity: The FMCG sector is witnessing increased competition, particularly in categories like hair oils and beverages.

-

Currency Devaluation: Emerging markets like Egypt, Nigeria, and Turkey have experienced currency devaluations, impacting Dabur’s international business performance in INR terms.

-

Weather-related Challenges: Extreme weather conditions, such as the recent heatwave, can impact demand for certain products like Chyawanprash.

Analyst Concerns and Management Response:

-

Concern: Slow growth in the Juices and Nectars category.

Response: Management acknowledged the challenges in this segment due to increased competition from carbonated beverages. They are focusing on expanding their presence in the drinks and carbonated segments to address this issue. -

Concern: Margin sustainability.

Response: Management expects to maintain or slightly improve margins through a combination of cost-saving initiatives, premiumization, and selective price increases. -

Concern: Performance of the Namaste business.

Response: Management reported progress in achieving corporate separateness for Namaste, reducing legal costs, and negotiating with insurance companies to potentially recover some legal expenses.

Competitive Landscape:

Dabur faces intense competition across various categories:

- Oral Care: Competing with market leaders like Colgate and other ayurvedic players like Patanjali.

- Hair Oils: Facing increased competition from players like Bajaj, particularly in the coconut oil segment.

- Juices and Nectars: Competing with established players like Tropicana and new entrants in the carbonated beverages segment.

Guidance and Outlook:

The management expressed optimism about the gradual uptick in FMCG demand, driven by good monsoon, improving macroeconomic indicators, and rural-centric government spending. They expect subsequent quarters to show better performance than the current quarter.

Capital Allocation Strategy:

The company remains committed to investing behind its brands, with A&P expenditure increasing by around 16% in the quarter. Dabur is also investing in manufacturing capabilities and digital advancements to drive sustainable growth.

Opportunities & Risks:

Opportunities:

- Expansion in the Home Care segment, targeting to reach INR 1,000 crores in revenue.

- Growth in e-commerce and quick commerce channels.

- Potential for market share gains in the ayurvedic and natural products segments.

Risks:

- Continued pressure on the Juices and Nectars category due to competition from carbonated beverages.

- Currency volatility in international markets.

- Potential inflationary pressures in the second half of the fiscal year.

Regulatory Environment:

The company mentioned increased scrutiny of spice exports to international markets, particularly the UK, following recent quality concerns in the industry.

Customer Sentiment:

Management indicated improving consumer sentiment, particularly in rural areas, driven by government initiatives, normal monsoon, and moderating inflation. However, they noted that South India continues to face pressure in terms of demand.

Top 3 Takeaways:

- Rural recovery and portfolio diversification are driving Dabur’s growth.

- The company is successfully expanding its market share across 95% of its portfolio.

- Dabur is focusing on premiumization and expansion into new categories to drive future growth and margin improvement.

Clean Science and Technology Limited (CSTL) – A clean and green future ahead (10-08-2024)

Clean Science Q1 FY25 Analysis: Key takeaways!!

Clean Science and Technology Limited reported encouraging Q1 FY25 results with 16% year-on-year revenue growth, primarily driven by volume increases across segments. The company is seeing stable demand and pricing environment, with capacity utilization at 60-65% for most products. Management expects continued volume-led growth in the coming quarters.

Strategic Initiatives:

-

HALS Expansion: CSTL has commercialized three new HALS products (622, 944, 783) in July 2024, with HALS 119 expected in August. This expanded portfolio will help target new customers and markets.

-

New Performance Chemicals Capex: The company announced a INR 150 crore capex for a novel process to manufacture a performance chemical, addressing 15% of global market demand.

-

Additional Capex Plans: Two more projects are underway – a INR 30 crore pharma intermediate plant and another INR 150 crore performance chemical plant for water treatment applications.

Trends and Themes:

- Volume-led Growth: CSTL is experiencing growth primarily through increased volumes rather than price increases.

- Import Substitution: New capex projects aim to capture market share from imports in various segments.

- Green Initiatives: The company is investing in a 6 MW solar plant to reduce power costs and improve its environmental footprint.

Industry Tailwinds:

- Recovery in Demand: Post-destocking phase, demand is picking up across segments.

- Import Substitution Opportunities: Indian manufacturers are benefiting from the push for local manufacturing.

Industry Headwinds:

- Pricing Pressure: Realizations remain stable to slightly lower, offsetting some volume growth.

- Global Economic Uncertainty: Potential impact on export markets.

Analyst Concerns and Management Response:

Concern: Slow ramp-up of HALS capacity

Response: Management expects faster adoption with the full basket of HALS products now available. They aim to reach 70-75% market share in India and expand in global markets.

Concern: Profitability of new investments

Response: Initial margins may be lower due to high fixed costs, but are expected to improve as capacity utilization increases.

Competitive Landscape:

CSTL faces competition from Chinese and European manufacturers in the HALS segment. However, the company believes its differentiated technology and expanded product basket will help it compete effectively.

Guidance and Outlook:

- HALS Volume: Target of 150-200 tons per month in the next 3-4 months

- FY25 HALS Volume: ~2,000 tons

- FY26 HALS Volume: 2,500-3,000 tons (50% capacity utilization)

- HALS Pricing: $7-8 per kg average realization

Capital Allocation Strategy:

The company is investing heavily in capacity expansion, with INR 330 crore already invested in HALS and additional INR 300 crore planned for new projects over the next 18-24 months.

Opportunities & Risks:

Opportunities:

- Full-basket HALS offering to capture larger market share

- New performance chemical products with potential for high returns

- Export market expansion

Risks:

- Slower than expected ramp-up of new capacities

- Pricing pressure from global competitors

- Regulatory changes affecting key products

Customer Sentiment:

Customers are showing increased interest with the expanded HALS portfolio. Large customers were waiting for a full basket of products before committing to larger volumes.

Top 3 Takeaways:

- HALS expansion is progressing well, with potential for significant market share gains

- New capex projects in performance chemicals offer growth opportunities

- Volume-led growth continues across segments, offsetting pricing pressures

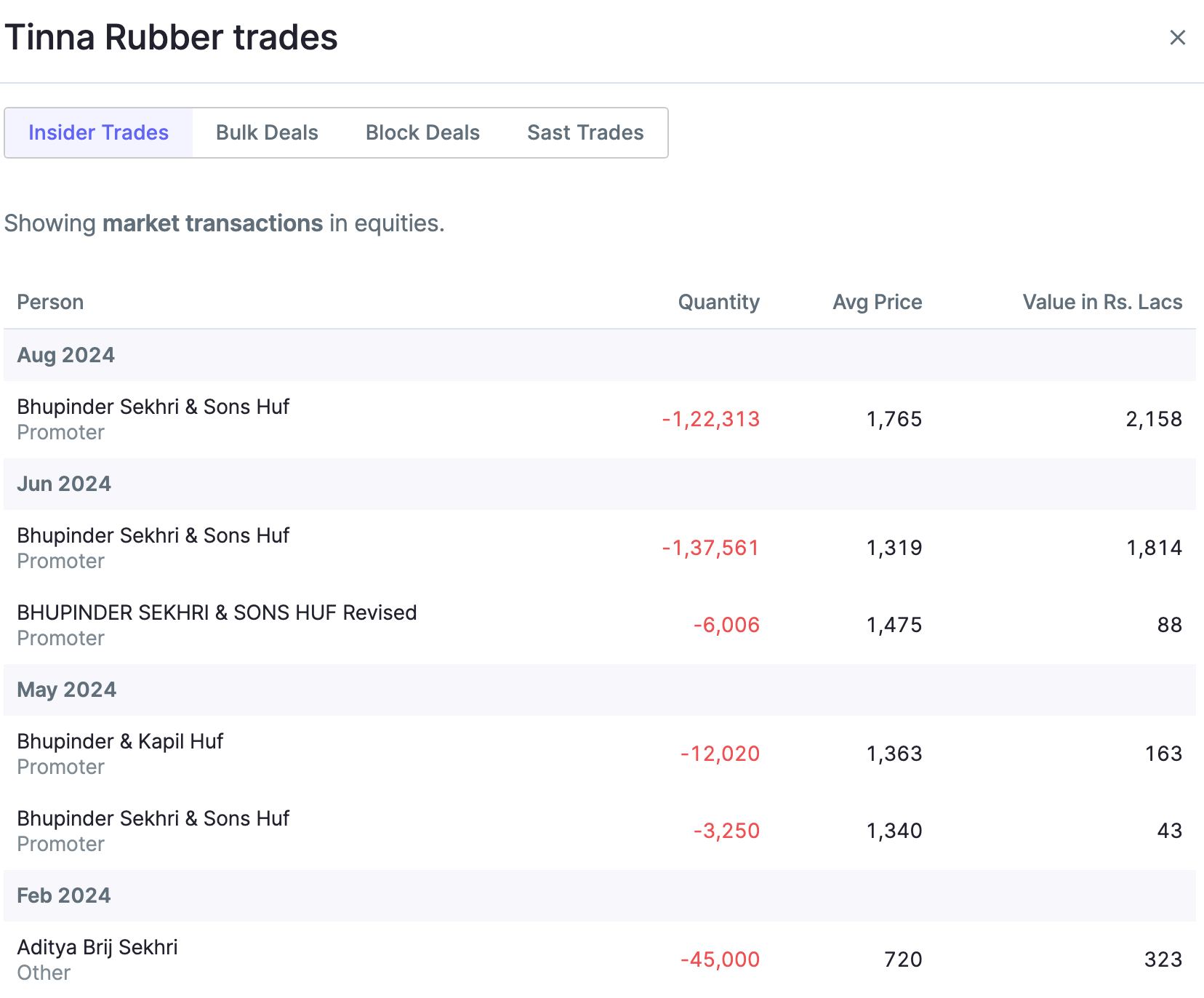

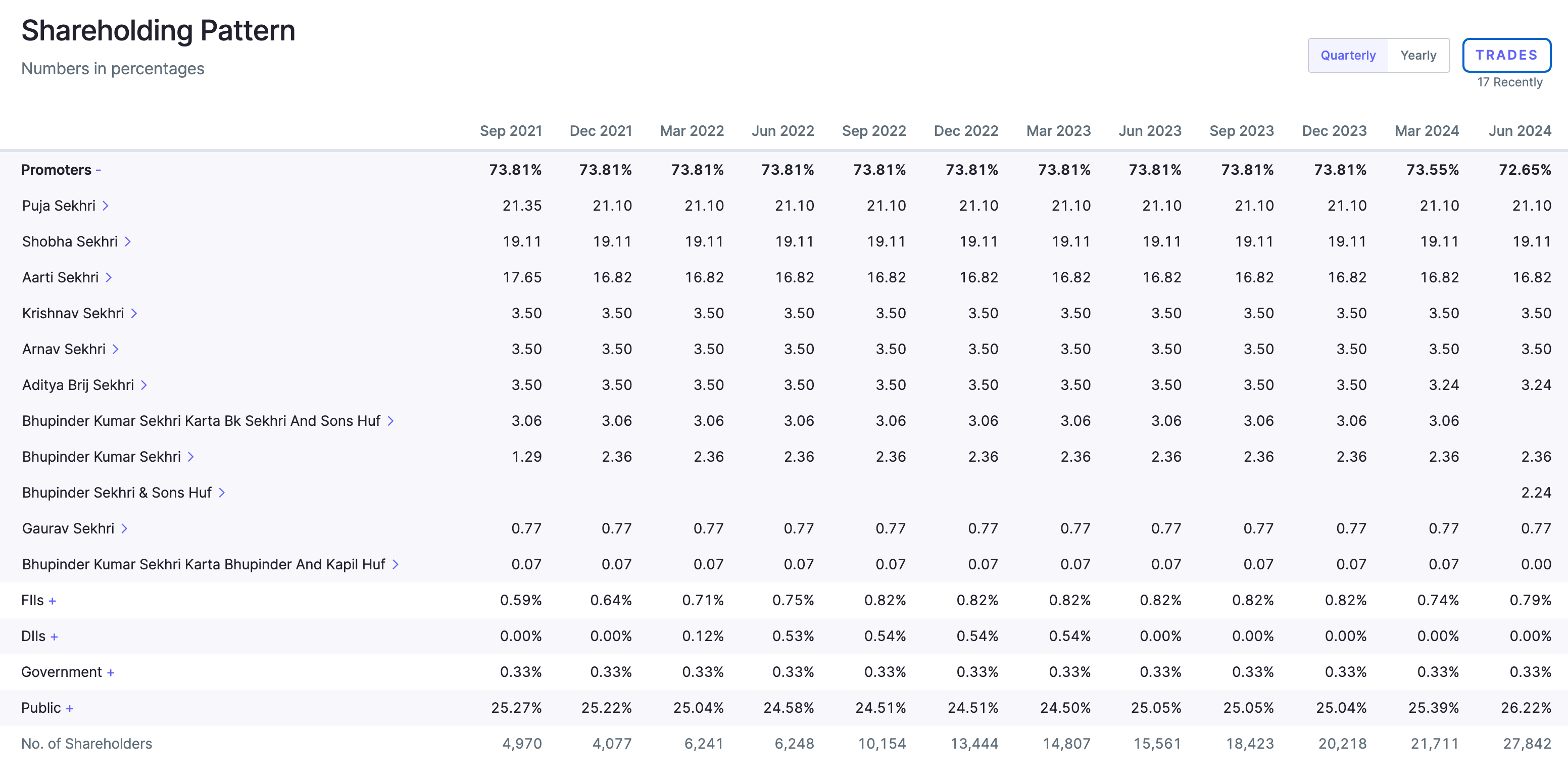

Tinna rubber – recycling a rubbery growth path (10-08-2024)

True. I don’t know the reason. I am just sharing the snapshots from the screener.in

And a very interesting shareholding pattern by promoters.

Insights or analysis from Financial Statements: Balance Sheet, Income Statement and Cash Flow Statement (10-08-2024)

@HarshVijay Sire: Not taking new enrollments. Thanks.