Hi Shreya!

As per the management in todays concall, they will be able to sustain margins above 20% (as per me they can do 20-22% margins on yearly basis this year). Seasonality led by demand from the SCF segment led to 25% margin in Q1. Rest, the topline guidance of 2000cr for FY25 and 2500 cr for FY26 remains intact.

Posts tagged Value Pickr

Garware Hi-tech films (Earlier Garware polyester) (09-08-2024)

Dreamfolks services limited( DFS) (09-08-2024)

Good Q1 results. Sales increased by 20% and company has given guidance of 20% for the year. Margins are stable… hope margins increase once the new business increase volumes.

This seems to be the steady state growth and in case they are able to expand globally it will be a huge jump.

FIIs have been decreasing holding and DII increasing for past 1 year – I think the price stagnation was due to this change in hands. hopefully it will move up now.

Disclosure – invested recently and biased.

Hariom Pipes Ltd: A Capex Play! (09-08-2024)

The result should be compared yoy. Qoq comparison is not right in this one

Vaibhav Global ~ Vertically integrated value e-tailer of Jewellery and Lifestyle Products (09-08-2024)

Vaibhav Global Q1 FY25 Earnings Analysis: Key takeaways!!

Business Outlook:

- Revenue grew 15% YoY to Rs. 756 crores, driven by digital growth and recent acquisitions

- Gross margin expanded significantly to 66.1% from 61.2% last year

- EBITDA margin contracted to 8.7% from 10% due to higher marketing and broadcasting costs

- Management reiterated FY25 revenue growth guidance of 14-17% with operating leverage

- Mid-teens revenue growth projected for future periods with continued operating leverage

Strategic Initiatives:

- Focusing on “4R Strategy” – Widening Reach, New Customer Registration, Customer Retention, and Repeat Purchases

- Investing in digital marketing and better TV channel positions to drive growth

- Integrating recent acquisitions Ideal World and Mindful Souls

- Leveraging VGL’s supply chain to improve profitability of acquired businesses

- Exited low-margin apparel manufacturing business

Trends and Themes:

- Shift towards digital channels – now 40% of revenue and 45% of volume

- Budget Pay EMI option contributing 38% of B2C revenue

- Expanding customer base – unique customers up 37% YoY to 636,000

- Focus on sustainability – using renewable energy, rainwater harvesting

Industry Tailwinds:

- Growth in online retail industry, especially in the US

- Recovery expected in UK and German economies as interest rates moderate

Industry Headwinds:

- Cautious consumer sentiment in UK due to economic uncertainty

- Overall jewelry market seeing negative growth in US

- Election cycle in US may impact viewership

Analyst Concerns and Management Response:

- Rising content and broadcasting costs (20% of revenue in Q1)

Management: Expects to moderate to 18% for full year, sees operating leverage ahead - Slow growth in core US/UK markets

Management: Expects improvement as macro conditions stabilize, mid-teens growth sustainable

Competitive Landscape:

The company positions itself as vertically integrated with quick turnaround times

Guidance and Outlook:

- FY25 revenue growth of 14-17% with operating leverage

- 200 bps gross margin expansion expected YoY

- Germany to be profitable at operating level by H2 FY25

- Mid-teens revenue growth expected in future periods

Capital Allocation Strategy:

- Declared interim dividend of Rs 1.5 per share (90% payout)

- Focused on organic growth and integrating recent acquisitions

- No immediate plans for further geographic expansion

Opportunities & Risks:

Opportunities:

- Further digital penetration and customer migration from TV to digital

- Geographic expansion (e.g. Japan in 3+ years)

- Margin improvement as acquisitions integrate

Risks:

- Macro uncertainties in key markets

- Rising customer acquisition costs

- Integration challenges with acquisitions

Customer Sentiment:

- Strong in US, cautious in UK, improving in Germany

- Overall retention rate of 40%, repeat purchases of 24 pieces per annum

Top 3 Takeaways:

- Digital growth and acquisition integration driving revenue, but near-term margin pressure

- Management confident in mid-teens growth sustainability with operating leverage

- Focus on customer acquisition and retention through omnichannel strategy

My portfolio expert advise needed _/\_ (09-08-2024)

I am not that great in doing fundamental analysis ![]()

Tata Steel – Would be merger be of any value? (09-08-2024)

Tata Steel Q1 FY2025 Earnings Analysis: Key takeaways!!

Tata Steel faces a challenging global steel demand environment due to subdued economic activity and tight monetary policies. However, the company remains bullish on India as a growth market and is strategically expanding its capacity to leverage this opportunity. The management expects steel demand in India to remain stable, despite some short-term impacts from elections and seasonal factors.

Strategic Initiatives:

-

Capacity Expansion: Tata Steel is progressing with its Kalinganagar expansion, with the blast furnace startup expected by end of September 2024. This will add 1.7 million tonnes of production capacity.

-

UK Operations Transition: The company is transitioning its UK operations to a more sustainable model by ceasing blast furnace operations and moving towards electric arc furnace (EAF) technology.

-

Netherlands Decarbonization: Tata Steel is in discussions with the Dutch government for support on a decarbonization project, which includes replacing a blast furnace with a Direct Reduced Iron (DRI) plant and an EAF.

-

NINL Expansion: Plans are underway to expand the Neelachal Ispat Nigam Limited (NINL) capacity to 5 million tonnes per annum.

-

Focus on Value-Added Products: The company is enhancing its downstream capabilities, including a new continuous annealing line and cold rolling mill complex.

Trends and Themes:

-

Decarbonization: Tata Steel is actively pursuing decarbonization initiatives across its global operations, particularly in Europe.

-

Digitalization and Automation: The company is leveraging technology to improve operational efficiency and customer engagement.

-

Shift towards Electric Arc Furnaces: This aligns with the global trend of moving towards more flexible and environmentally friendly steel production methods.

Industry Tailwinds:

- Growing steel demand in India

- Government focus on infrastructure development

- Potential for import substitution in high-end steel products

Industry Headwinds:

- Global overcapacity and Chinese exports pressuring steel prices

- Rising raw material costs

- Stringent environmental regulations increasing compliance costs

Analyst Concerns and Management Response:

-

Concern: Impact of potential retrospective mineral cess in India

Response: Management acknowledged the complexity of the issue and is engaging with the government to address industry-wide concerns. -

Concern: Funding for European operations decarbonization

Response: The company is seeking government support and exploring project financing options to minimize the impact on the parent company’s balance sheet. -

Concern: Delay in capacity expansion plans

Response: Management reaffirmed its commitment to the expansion roadmap, with flexibility to pace investments based on market conditions.

Competitive Landscape:

Tata Steel maintains a strong position in the Indian market, particularly in value-added segments like automotive steel. The company faces competition from other major Indian steelmakers and global players, especially in export markets.

Guidance and Outlook:

- India operations expected to see a reduction in net realizations by Rs. 1,500 per ton in Q2 compared to Q1

- Netherlands operations projected to have a £60/t reduction in net realizations in Q2

- UK operations expected to break even or turn slightly positive on EBITDA basis after the closure of the second blast furnace in 2H FY2025

Capital Allocation Strategy:

- Focus on growth investments in India

- Decarbonization investments in European operations, largely supported by government grants and internal accruals

- Continued deleveraging efforts at the consolidated level

Opportunities & Risks:

Opportunities:

- Expansion in high-growth Indian market

- Potential for value-added product mix improvement

- Cost savings from operational efficiencies and decarbonization efforts

Risks:

- Global economic slowdown impacting steel demand

- Volatility in raw material prices

- Regulatory changes affecting mining operations in India

Regulatory Environment:

The recent Supreme Court judgment allowing states to levy cess on mineral rights has created uncertainty in the Indian mining sector. Tata Steel is closely monitoring the situation and engaging with authorities to mitigate potential impacts.

Customer Sentiment:

The company reported strong growth in key segments like automotive (9% YoY) and engineering goods (19% YoY), indicating positive customer sentiment in these sectors.

Top 3 Takeaways:

- Tata Steel remains committed to its India growth story, with strategic expansions underway despite global challenges.

- The company is making significant progress in transitioning its European operations towards more sustainable production methods.

- Management is actively addressing regulatory and cost pressures through operational improvements and strategic initiatives.

Hariom Pipes Ltd: A Capex Play! (09-08-2024)

I find it decent to good. PBT is actually lower QoQ. But this does not change the long term thesis. I am confident about it.

NOCIL Limited ~ One-Stop-Shop for Rubber Chemicals in India (09-08-2024)

NOCIL is high risk medium return. the Q1 numbers prove that. it seems to be facing a lot of competition which will prevent it from making profits… valuation is too high.

Tata Steel – Would be merger be of any value? (09-08-2024)

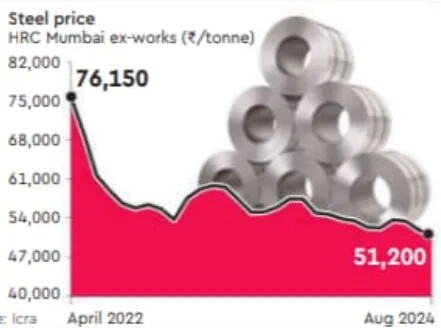

The Domestic Steel Price Plunge

In the surprising turn of events for the past 3-4 years, domestic steel prices in India have fallen to a 45-month low , despite a strong underlying demand. For a nation like India which has a goal to achieve 300 million tonne per annum (mtpa) steel-making capacity by 2030 , might derail its ambitious goal in the steel industry. Let’s decode what is happening in the sector.

What’s happening?

Over the past few months, steel prices have taken a steep dive, reaching ₹51,200 per tonne in August 2024, down from ₹76,150 per tonne in April 2022. This significant drop comes even as India witnesses strong steel consumption growth , which rose by 13.4% year-on-year in FY23.

So, what’s driving this decline?

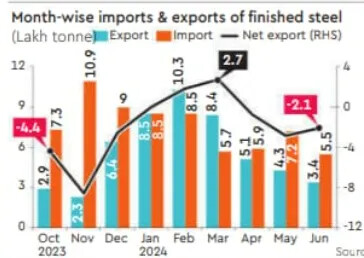

One of the primary reasons behind the price plunge is the growing imbalance between steel imports and exports . In the past, India was a net exporter of steel, which means it exported more steel than it imported. However, in recent times, this trend has reversed. India has now become a net importer of steel, with imports exceeding exports by 0.83 million tonnes (MT) in FY24. In FY24, imports grew 38%, where as exports rose just by 11.5% over FY23.

The reason behind this is cheaper imports, especially from countries like China and South Korea, have flooded the Indian market. According to steel ministry data, China contributed 30.5% of India’s total imports during the April-June period, compared with 28.4% a year ago. The increase in China’s Steel exports by 24.7% year-on-year for FY24, has resulted in significant drop in export volumes of Indian steel Companies. This has affected the pricing dynamics within the Indian Industry.

Analysts have given three main reasons for the worsening of steel trade balance which are mentioned below

- Weak global demand mainly due to tightening monetary policies and geopolitical tensions.

- Low priced imports from steel surplus countries obviously, China.

- A slowdown in Chinese economy majorly due to the real estate crisis, to which steel is the basic raw material for the real estate sector.

What does the experts say?

TV Narendran, CEO and MD of TATA Steel Ltd ., quoted that “These prices aren’t sustainable. We expect the trend to reverse in the next few weeks.”

“Indian steel prices have fallen to their lowest levels in over three years, largely due to shifts in the global market. A notable slowdown in China’s economy has triggered a correction in global steel prices, with Chinese export prices dropping to a four-year low. This decline has led to a surge in HRC imports from Vietnam and China into India,” said Dhruv Goel, CEO, BigMint.

Domestic firms also allege that the Indian steel sector is in a structural disadvantage due to various taxes, duties and levies. Other exporting countries like China, Japan, Korea, ASEAN, etc. are not prone to these taxes.

Conclusion

India’s journey towards becoming a steel powerhouse is fraught with challenges, but with the right policies and industry support, it’s a journey that can still lead to success. As the country moves forward, balancing the dynamics of steel sector will be crucial in ensuring that its steel sector remains competitive and capable of achieving the ambitious targets set for the coming decade.

Your thoughts and views is highly appreciated.

Rishi Laser- A Precision Fabricator (09-08-2024)

Does anyone know or can anyone share who owns the rest of the business?