Excellent results from Hariom

Total Income of ₹344.20 Crore, up 43% YoY

• EBITDA of ₹45.57 Crore, up 56% YoY

• PAT of ₹17.51 Crore, up 14% YoY

I dont know why market took it negative i see upside once people understand the results correctly i think this will be last quarter for major interest burden

Posts tagged Value Pickr

Hariom Pipes Ltd: A Capex Play! (09-08-2024)

Tanla Platforms ~ Leading player in the fast-growing CPaaS market (09-08-2024)

Yesterday, Tanla declared that it has onboarded Axis Bank for its Wisely ATP platform.

This is great news but surprising the stock price did not move as expected.

I am reducing position size here and raising some cash. I will see how growth pans out over the next few months to decide to add back or reduce further or exit.

Biocon – The ultimate biosimilars play! (09-08-2024)

Can anyone please explain what does that mean? how loss of significance results into gain?

Why dumb Mr. Index is so tough to beat? Let’s discuss it’s alpha (09-08-2024)

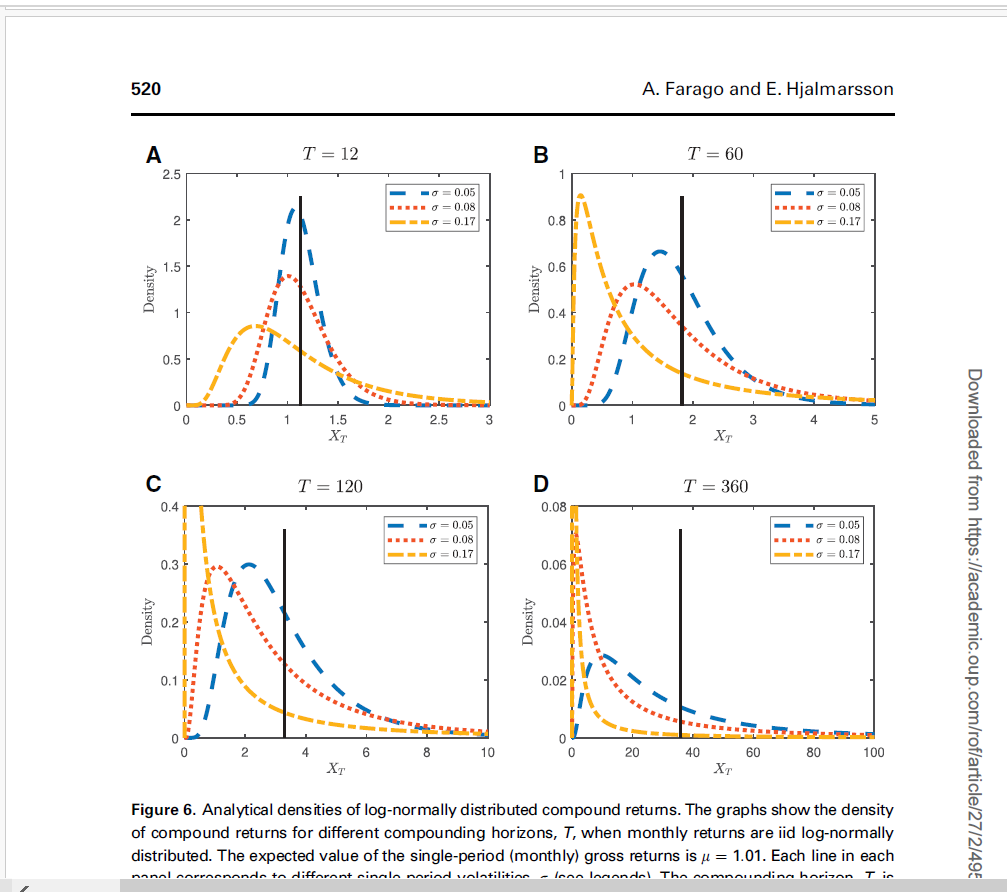

Stock returns are positively skewed over an extended period of time. Randomness holds [bell shaped normal curve] only on the first period. Sharing the graph from Farago- Hjalmarsson study of 2022-

It happens because good investors of one time period has a better chance of doing good in next periods (to hell with the efficient market hypothesis). Well, ultimately the return curve over an extended period of time looks like 80-20 curve (power curve). Hardly 20% of investors can beat the average.

Even among the 20% winners, power law operates. 80% of those 20% can merely beat the market with 1-2-3% margin which may not be sufficient to take the stock picking endeavour. 4% of the investors [20% of 20%] can beat the market handsomely, 1% can be extremely extremely successful and a few will be outliers like Rakesh Jhunjhunwala.

Thus, most of the people not beating the index is a statistical certainty.

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (09-08-2024)

Reasons for Muted Q1 Results for UGRO Capital (Q1 FY25)

- Income on Co-Lending/Direct Assignment Decline:

- There was a significant decrease in income from co-lending and direct assignments, falling by 59% quarter-on-quarter, which impacted total income and profitability.

- Credit Costs Increase:

- Credit costs rose by 58% year-over-year, driven by increased provisioning, which affected the bottom line.

- Higher Interest Expenses:

- Interest expenses grew by 47% YoY, narrowing the net interest margin, contributing to a more muted net total income.

- Operational Expenses:

- Despite a moderate increase in employee costs (48% YoY), other operational expenses showed only an 8% YoY rise, which helped maintain control but did not offset the drop in income from co-lending.

- Lower Loan Origination:

- The overall net loan origination was modest, with adjustments due to reduced disbursements in supply chain financing, which typically contributes to the company’s higher-yield segments.

- Tax Impact:

- A significant reduction in tax expenditure (-60% QoQ) was recorded, primarily due to deferred tax write-offs, which provided some relief but did not significantly boost the PAT.

- Overall Net Income Decline:

- The net total income saw an 18% decline quarter-on-quarter due to the factors mentioned above, leading to a more muted performance compared to previous quarters.

These elements combined led to more subdued results for UGRO Capital in Q1 FY25, despite ongoing efforts in branch expansion and operational scaling.

Tanla Platforms ~ Leading player in the fast-growing CPaaS market (09-08-2024)

(post deleted by author)

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (09-08-2024)

During the Q4 FY24 earnings call, UGRO Capital discussed its experience and strategy regarding supply chain financing:

- Focus on Last-Mile Financing: UGRO emphasized its strength in financing the last leg of the supply chain, particularly from distributors to retailers. This segment is well-suited to UGRO’s data-driven and digital underwriting capabilities.

- Challenges with Anchor Financing: The company found challenges in providing financing for larger, anchor-led supply chains, which are dominated by larger NBFCs and banks. UGRO’s higher cost of funds and the competitive nature of these segments led to some negative selection and higher NPAs.

- Strategic Shift: Due to the complexities and risks associated with financing larger entities, UGRO decided to focus on the more granular last-mile retailer financing. This segment offers better yields and aligns with UGRO’s digital and physical infrastructure strengths. The company plans to gradually reduce exposure to the higher-risk segments of the supply chain while building out its retailer finance portfolio.

- Risk Management: UGRO acknowledged that the higher NPAs in its supply chain financing were due to the inclusion of lower-rated customers. They plan to manage this by focusing on segments that align better with their core competencies and by increasing the granularity of their portfolio.

Anchor-Led Supply Chain Financing:

What It Means:

- Anchor: In supply chain financing, an anchor refers to a large, reputable company (usually a big manufacturer or retailer) that serves as the central point in the supply chain. Smaller suppliers or distributors work with or supply goods to this anchor company.

- Anchor-Led Financing: This type of financing involves financial institutions extending credit to the suppliers or distributors based on their relationship with the anchor company. The credit is often secured against the invoices or purchase orders issued by the anchor.

Why It’s Competitive:

- Lower Risk Profile: Anchors are typically large, creditworthy entities. Financial institutions perceive lending against their receivables as lower risk, making it highly attractive.

- Lower Margins: Due to the lower perceived risk, the interest rates (or yields) on these loans are generally lower. Large banks and established NBFCs (Non-Banking Financial Companies) dominate this space as they can afford the lower margins due to their lower cost of funds.

- Volume and Scale: Large institutions are often better equipped to handle the high volumes and operational requirements of anchor-led supply chain financing, giving them a competitive edge.

UGRO’s Approach: UGRO found that competing in this space was challenging due to its relatively higher cost of funds and the pressure to compete on price (interest rates). Consequently, they faced negative selection, where they ended up financing lower-rated companies willing to accept higher rates, leading to higher NPAs.

In response, UGRO shifted its focus towards last-mile financing, where it could leverage its data-driven approach and physical distribution capabilities, thus avoiding direct competition with larger, more established financial institutions in the anchor-led space.

Beta Drugs Limited (09-08-2024)

Can someone please share their insights into what the future prospects of beta Drugs looks like??

KEI Industries Ltd – A consistent performer over the last decade (09-08-2024)

KEI Industries Q1 FY25 Analysis: Key takeaways!!

KEI Industries continues to demonstrate robust growth, with Q1 FY25 net sales increasing by 15.72% year-over-year to INR 2,060.50 crores. The company’s EBITDA grew by 24.55% to INR 232.41 crores, while profit after tax increased by 23.77% to INR 150.25 crores. The management expects to maintain a CAGR of 15-16% in the coming years, indicating a positive business outlook.

Strategic Initiatives:

- Capacity Expansion: KEI is undertaking significant capacity expansions, including:

- Brownfield expansion at Chinchpada for wires and house wires

- Greenfield/Brownfield expansion at Pathredi for LT power cables

- Major Greenfield expansion in Sanand, Gujarat for LT, HT, and EHV cables

-

Export Focus: The company is actively working to increase its footprint in international markets, particularly in the U.S. and Europe.

-

Product Mix Optimization: KEI is focusing on high-margin products like extra high voltage (EHV) cables and expanding its presence in sectors such as solar, wind, and oil & gas.

Trends and Themes:

- Increasing B2C Sales: The company’s distribution network sales (B2C) grew by 29% YoY, contributing 53% of total sales in Q1 FY25.

- Growth in Real Estate Sector: Strong demand for wires and flexibles from the real estate and rental markets.

- Shift towards Renewable Energy: Increasing demand for cables in solar and wind power projects.

Industry Tailwinds:

- Government infrastructure push

- Growing renewable energy sector

- Increasing industrial capex

- Revival in real estate sector

Industry Headwinds:

- Fluctuations in copper prices affecting short-term demand

- Logistical challenges in exports

Analyst Concerns and Management Response:

- Export Decline: Management clarified that the 24% decline in exports was due to logistics issues and expects to make up the shortfall in Q2.

- Margin Expansion: The company expects margins to improve by 1% in the next 3-4 years due to economies of scale from capacity expansions.

Competitive Landscape:

KEI Industries maintains a strong position in the cable and wire industry with an estimated 12% market share. The company’s focus on direct exports differentiates it from competitors who are shifting towards distributor-based models.

Guidance and Outlook:

- Revenue growth guidance of 16-17% for FY25

- EBITDA margin guidance of around 11% for FY25, with potential expansion to 12% by FY27

- Expectation of INR 200-300 crores revenue from the U.S. market in FY25

Capital Allocation Strategy:

- Total planned capex of INR 1,400-1,600 crores over FY25 and FY26 for the Sanand project

- Financing mix of INR 300-500 crores in term loans and the rest from internal accruals

Opportunities & Risks:

Opportunities:

- Expansion into new export markets

- Growing demand from renewable energy sector

- Potential for margin expansion with scale

Risks:

- Fluctuations in raw material prices

- Dependency on government infrastructure spending

- Intense competition in the wire and cable industry

Customer Sentiment:

Strong customer sentiment in both B2B and B2C segments, driven by infrastructure development, real estate growth, and industrial capex.

Top 3 Takeaways:

- Robust growth across segments with a focus on high-margin products and B2C sales

- Significant capacity expansion plans to support future growth

- Strong export potential, particularly in the U.S. market, with expectations of substantial growth in FY25

Zomato – Should you order? (09-08-2024)

“E-commerce is growing faster than modern trade, and modern trade is outpacing general trade, a trend that seems secular. E-commerce is segmenting into different models, including beauty commerce, grocery commerce, and quick commerce. E-commerce is about 7% of our overall sales, Q-commerce is one-sixth of that and continues to grow,” Jawa told Moneycontrol.

@Divyanshu_Parganiha, it clearly says Ecom is growing faster than modern and general trade.