overall with my mf and stocks it is around that level

Posts tagged Value Pickr

My portfolio expert advise needed _/\_ (03-08-2024)

overall with my mf and stocks it is around that level

BEW Engineering- A proxy play on pharma and chemical sector (03-08-2024)

I think they talked about 300 Cr as peak potential revenue at full capacity utilization (including the new capex)

BEW Engineering- A proxy play on pharma and chemical sector (03-08-2024)

I think they talked about 300 Cr as peak potential revenue at full capacity utilization (including the new capex)

RACL Geartech Limited (03-08-2024)

I have been following RACL for ~6 quarters now (with no purchases) and the company seems to be growing consistently and delivering consistent margins in the low 20s. The high gross margin is also great. The key issue here is that the return on capital is terrible and has consistently been in the mid-teens which does not point to a high quality manufacturer with significant pricing power but almost feels like they are buying business by holding inventory for their customers. There is also the question of how much of this inventory is real vs needs to be written off (since inventory days have doubled from 200 days to 350 days in 5 years). Even if one normalizes for growth, the cash flow conversion in this business is no more than 20% of EBITDA, which is quite poor. How do other folks who are invested / have spent time evaluating RACL consider this? Is it just a necessary evil in an auto anc business / fast growing company which is unable to manage inventory properly or does it point to some potential issue in the financials at a later date / structural issue in the business?

RACL Geartech Limited (03-08-2024)

I have been following RACL for ~6 quarters now (with no purchases) and the company seems to be growing consistently and delivering consistent margins in the low 20s. The high gross margin is also great. The key issue here is that the return on capital is terrible and has consistently been in the mid-teens which does not point to a high quality manufacturer with significant pricing power but almost feels like they are buying business by holding inventory for their customers. There is also the question of how much of this inventory is real vs needs to be written off (since inventory days have doubled from 200 days to 350 days in 5 years). Even if one normalizes for growth, the cash flow conversion in this business is no more than 20% of EBITDA, which is quite poor. How do other folks who are invested / have spent time evaluating RACL consider this? Is it just a necessary evil in an auto anc business / fast growing company which is unable to manage inventory properly or does it point to some potential issue in the financials at a later date / structural issue in the business?

Shriram AMC – Waking up after a hibernation. Mcap 300cr (03-08-2024)

Market seems to have finally realized this co now. However advising caution since Q1 results may not be good and I feel they have hardly gathered any Equity AUM in Q1.

Have liquidated 25% of the holdings at these levels.

Shriram AMC – Waking up after a hibernation. Mcap 300cr (03-08-2024)

Market seems to have finally realized this co now. However advising caution since Q1 results may not be good and I feel they have hardly gathered any Equity AUM in Q1.

Have liquidated 25% of the holdings at these levels.

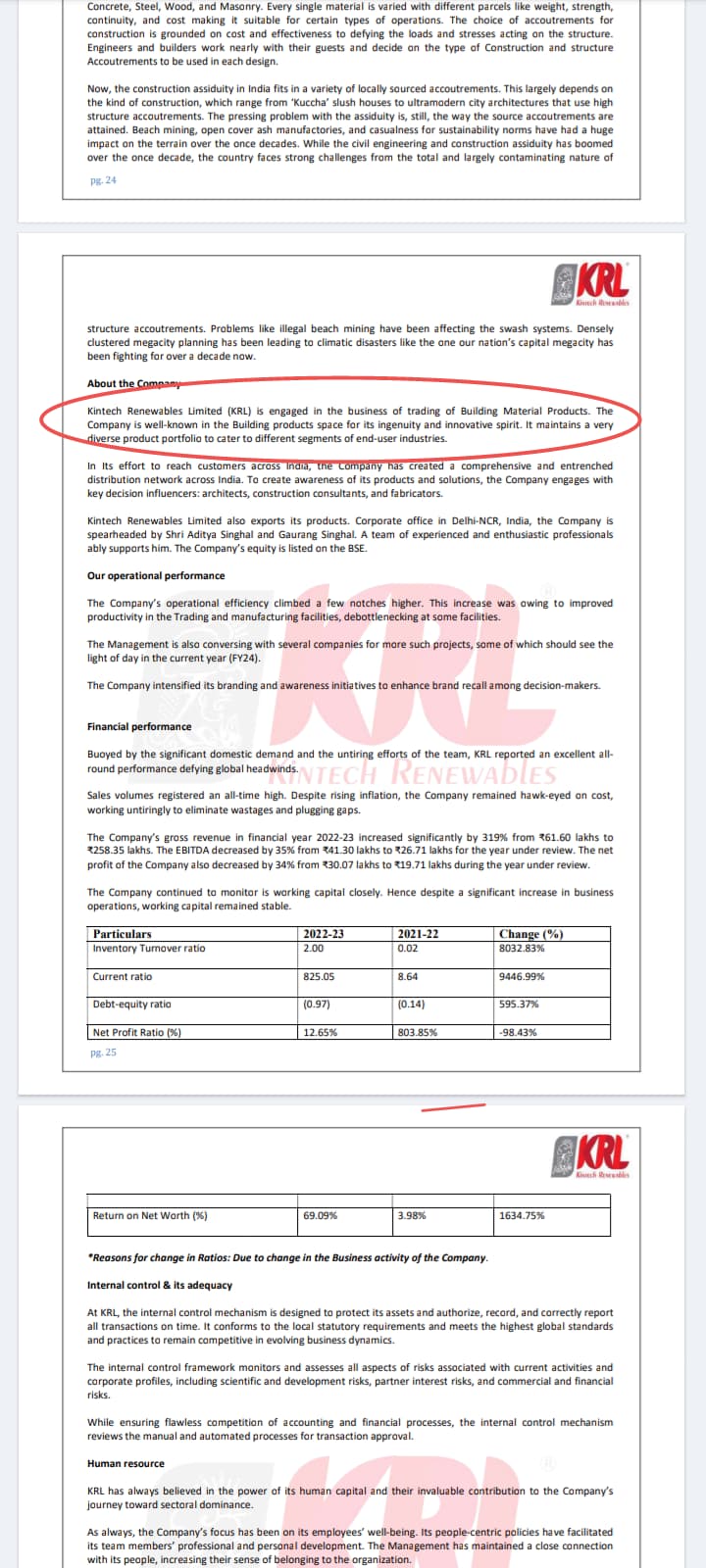

SG Mart- Can it successfully create a marketplace? (03-08-2024)

It’s also mentioned that they trading the building materials.

SG Mart- Can it successfully create a marketplace? (03-08-2024)

It’s also mentioned that they trading the building materials.