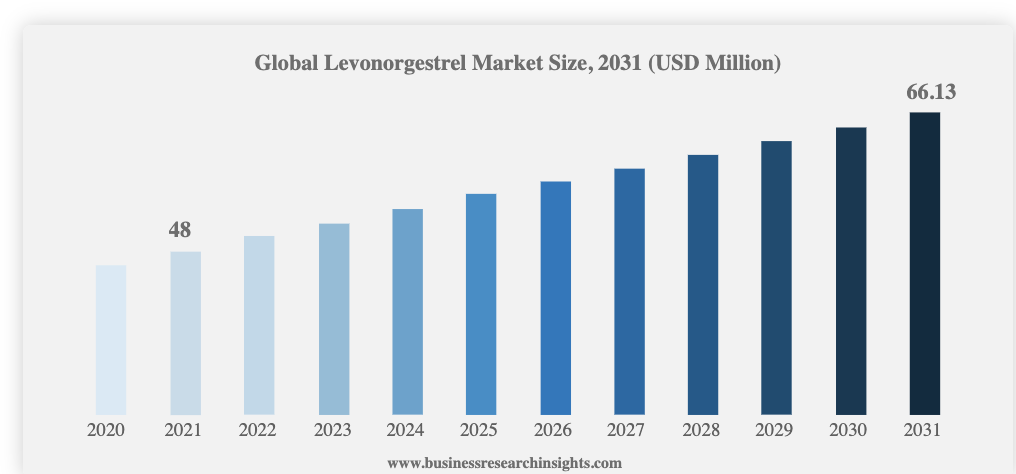

Global levonorgestrel market size was USD 48 million in 2021 and market is projected to touch USD 66.13 Million By 2031, exhibiting a CAGR of 3.3% during the forecast period.

Global levonorgestrel market size was USD 48 million in 2021 and market is projected to touch USD 66.13 Million By 2031, exhibiting a CAGR of 3.3% during the forecast period.

Global levonorgestrel market size was USD 48 million in 2021 and market is projected to touch USD 66.13 Million By 2031, exhibiting a CAGR of 3.3% during the forecast period.

What is the market size for this drug?

What is the market size for this drug?

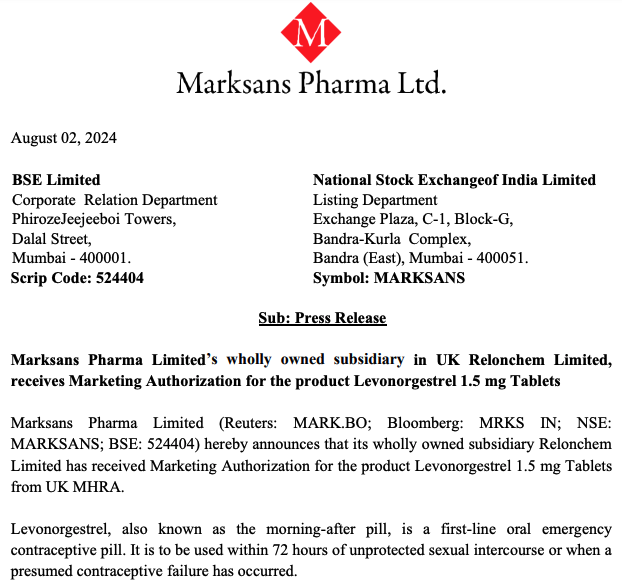

Received marketing auth

Received marketing auth

Hi Vishal, Yes I used Perplexity and then checked the numbers. I already narrated that my knowledge is limited and I am trying to use the available modern tools. If you find flaws in the content, kindly enlighten me. I am trying to learn from this platform and by using available modern tools. What I found that it picked numbers from Tijori and numbers are correct.

Holding neuland labs since 2021 , A quick update on Q1FY25 result

Total Revenue: ₹444.4 crores, up 21.7% from ₹365 crores in Q1 FY24.

EBITDA: ₹128.6 crores (excluding exceptional items), with a margin of 28.9%, an increase of 174 bps from Q1 FY24.

Gross Margin: 56.1%, compared to 55.2% in Q1 FY24 and 58.8% in Q4 FY24.

Profit After Tax (PAT): ₹98.3 crores, compared to ₹62.2 crores in Q1 FY24. This includes an exceptional gain of ₹30.6 crores from the sale of surplus properties.

Earnings Per Share (EPS): ₹76.6 per share.

Free Cash Flow: ₹50.9 crores generated in Q1 FY25.

Net Debt: Negative net debt position of ₹110.2 crores, with partial debt repayment of ₹8.7 crores.

Capital Expenditure: ₹59.1 crores invested in Q1 FY25.

Revenue Characteristics: ₹235 crores in Q1 FY25; variability in quarterly revenue. Annual trends are a better indicator of performance.

Revenue Drivers: Commercialization of key molecules, influencing lumpiness in revenue.

Specialty APIs: Dorzolamide and Donepezil: Niche therapeutic areas with strong performance.

Prime Products: Key Products: Mirtazapine, levetiracetam, escitalopram, providing stable revenue.

Ezetimide Transition: Transition from specialty to prime segment affects specialty segment performance.

Growth and Margins: Modest growth anticipated, with normalized margins. Focus on operational efficiency and consolidating investments.

Impact of Investments: Ongoing capital investments and product lifecycle may impact revenue growth.

Manufacturing Facilities: New facilities and commercialization of new molecules expected to drive growth.

R&D Pipeline: Strong pipeline with promising molecules in development.

BioSecure Act: Limited immediate impact but optimistic for long-term prospects.

Big Pharma Acquisitions: Opportunities and challenges as biotech clients are acquired by large pharmaceutical companies.

Order Flow: Strong order flow with confidence in medium and long-term prospects.

Influencing Factors: Product performance, foreign exchange rates, and raw material costs.

Unit 3: Timeline: Expected operational by end of FY25, with commercial production starting H2 FY26.

Capacity Utilization: Initially at 30-40%; expected to increase as more CMS molecules are integrated.

Units 1 and 2: Current Utilization: Near full capacity; acquired land for future expansion.

Short-Term Capex: Small additions to meet increased demand for GBS products.

.

Pelivaradon: Limited competition, niche market.

Penta Capone: Moderate competition, with Indian and European players.

Dozen Lite and Apex Bar: Market competition varies by therapeutic demand.

Unit 3 Utilization: 30-40% in Q1 FY25, expected to rise with increased CMS molecules.

Cost Reduction: Reduced manufacturing expenses by 30-40%.

Historical ROA: 10-15% for similar expansions; future ROA dependent on market conditions.

Current Clients: Increased engagement from existing biotech clients bringing additional molecules.

New vs. Existing: Growth from both new and returning clients.

Focus Shift: Biotech companies being acquired by larger pharma companies; potential for expanded collaborations.

API Model: Continued success with PurePlay API model, significant growth potential.

Market Opportunity: API market valued over $120 billion; company still in early stages of market capture.

Growth: Focus on API model for GBS and CMS.

Diversification: Explore new technologies and innovations within the API space.

Objectives: Enhance drug development and manufacturing processes.

Supply Chain Issues: Reducing dependence on Chinese suppliers; exploring alternative sources.

Geopolitical Risks: Impact from events like the Russia-Ukraine conflict.

Currency Risks: Monitoring fluctuations as part of risk management.

Consideration: The stock split idea under review; discussions ongoing with advisors to determine feasibility.

Historical Margins: Historically 14-15%, with peaks around 28-30%.

Normalization: Aiming to normalize margins without specific past performance references.

Business Model Shift: Reduction in reliance on prime products affecting margins.

External Factors: Variations in raw material costs and exchange rates.

Chronic Kidney Disorders: New peptide molecule in development.

New Developments: Six to seven new molecules in various stages, with a focus on specialty areas.

Specialty Focus: Many new molecules have longer development cycles.

as they need sun and some bare minimun man power for monitering and cleaning.

Q1 FY2025 Concall Highlights:

Opening Remarks:

Revenue Growth 12% YoY.

PAT Growth 67% YoY.

Company continue to add value.

This year may be best ever. Will be 3 years in row.

EBIDTA to sales also moving up.

Debt is increased to lock in raw material prices, which are favorable.

11lac crores for infrastructure by govt. is music for us.

#Jindal Hunting Energy Services Limited:

In First quarter it self, capacity utilization is 85%. Profitable in Q1 it self.

Joint Venture may have some announcement, because order book is full for rest of the year and all boxes are ticked.

Oil Country Tubular Goods (OCTG) company wants to make India Atma Nirbhar.

# Sathavahana Ispat Limited:

Profitable. De-bottlenecking will increase capacity by 10 to 20% at least.

Creating special niche for small diameter which have high demand and high value.

Orderbook:

Oil & Gas is 30 to 35%. Water is 70%. Others is 5%.

UAE is only water facility, DI facility. Supply not only to middle east, all over world in 33 countries.

1.6 billion Dollars. 16 lac tons.

Saw pipe demand not squished. More then 5 lac Ton order for large diameter pipe.

Govt. of India come up with balance scheme, where state has to bring contribution. That makes projects are on track.

Export:

Export is 70%, which is sweet spot. Water pipes mostly in middle east. Oil and Gas is all over world.

CAPEX:

No plans yet. Conserving money.

Conclusion:

Many questions were not answered due to confidentiality and coemption etc.

Value addition projects are going on.

Valuations are lucrative at 12 PE.

As per management, FY2025 will be again best ever.

Financial Highlights:

D: Invested