Just sharing the company update.

I hope you find it useful

dr.vikas

Just sharing the company update.

I hope you find it useful

dr.vikas

@sammy11 If you could share some insights and rationale for your investment it could help build a good starting point for discussion . Also how much of an impact the RBI priority sector lending changes do you think it could have on Arman and the sector ?

Can someone please provide any views that they might have on Markobenz Ventures Ltd? Deep insights would be appreciated for this penny stock. Does it have a massive upside at the current stage?

Same Question!!! I also would really appreciate a deep analysis into this stock…

Here is the link i got after an email request.

Can the members provide their view on Titan Intech stock?

Yes, HFCL is another example of Atma Nirbhar Bharat , but HFCL had a chequered past.

Related-party transactions are certainly a red flag, investors should be concerned.

Apart from that, the company is in a very niche space rapidly expanding. The number of Airports, flights etc. will almost certainly go up leading to greater business opportunities to the company. Further the company is in a space related to safety, the business is sticky for the airport operators.

The company has started doing the assembly work for some of the products. It has the first-mover advantage here. It will also increase the company’s margin compared to the supply of imported products.

Intermittently the company is declaring various orders.

Today the company declared Bridgehill AS Norway, world’s largest Car Fire Blanket manufacturer.

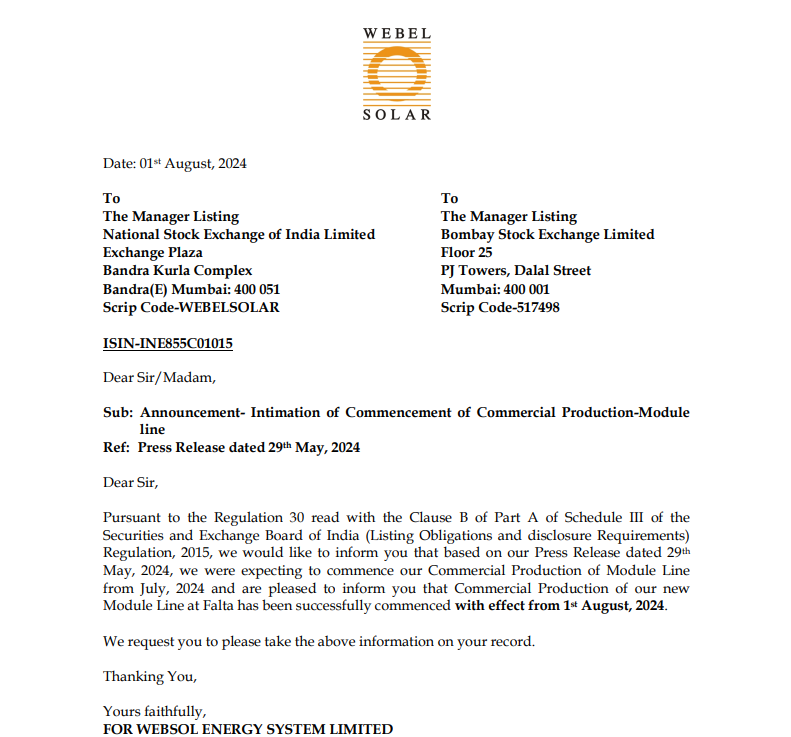

ANLON_01082024135438_Reg30.pdf (105.0 KB)

The market Anlon is operating is niche, very small. Thus, I don’t think any big competition is coming in the area. Further, the niche is likely to grow at a fast pace, giving a sweet spot to the company. The margin maintained by the company is impressive. Make in India is favoring the company. Hopefully, the management will utilize these tailwinds for the company’s growth.

[Disclosure- Invested and biased]

Co-origination and co-lending generally refer to similar processes where two financial institutions (typically a bank and an NBFC) collaborate to issue loans. In this setup, both banks (lenders) and NBFCs (originators) share the risk in a predetermined ratio (typically 80:20). [Specifically, 80% of the loan is with the lender, and a minimum of 20% is with the originator (https://www.go-yubi.com/blog/what-is-co-origination-and-how-does-the-co-origination-model-work/)

The net loan origination appears muted across all buckets except for the micro enterprise loan-book. Here could be some potential reasons: