The management is focussed on there business there is no doubt. It’s just after two high growth years they are seeing some dip in footfalls. They are doing fund raise to fuel growth for next 7-8 years comprising 5 park. They are don’t need fund for Chennai park. They have moat in there business as they manufacture and install there own rides. I think next ten year all we see a new wonderla. I think they will raise approx 1500 – 2000 cr for atleat 2 big parks like Chennai and Bangalore(500 cr each) and 3 tier 2 parks like orissa and kochi (200 cr each)

Posts tagged Value Pickr

EFC – Entrepreneurial Facilitation Centre (01-08-2024)

Came across this term Lease liabilities and Right of use assets on balance sheet of Awfis ~ indicatively 570 cr of lease liabilities and Rs 580 cr of Right of Use assets as on Mar 2024. I understand that lease liabilities are the present value of lease payments to the landlord/commercial space owner over the lease term. Any idea if this is net of the lease payments to be received from the client by the occupier. Thanks a lot

Focus Lighting & Fixtures Limited (SME) (31-07-2024)

There are couple of large public shareholders who have been cutting their stake for last few quarters, I am guesssing they are exiting. Such volumes can come from only large holders.

Jash Engineering – Is it a multibagger (31-07-2024)

Allotment of Plot at SEZ Pithampur, District Dhar (Madhya Pradesh)

https://nsearchives.nseindia.com/corporate/JASH_31072024145049_JASHLANDALLOTMENT.pdf

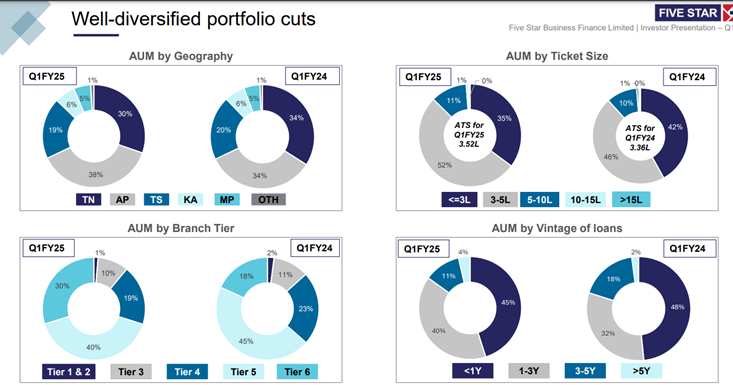

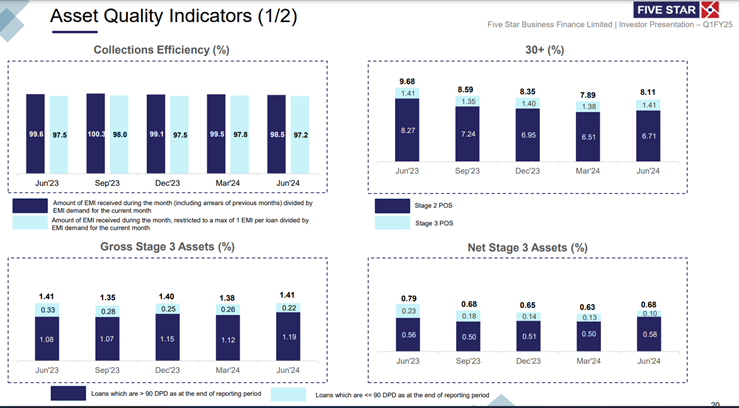

Five Star Business Finance – Financing Bharat! (31-07-2024)

Good set of results from Five Star. Consistent growth stable asset quality.

Only worry is a large % of the book is unseasoned.

Lag asset quality numbers are encouraging though (when looked at wrt yields)

Investor-Presentation-for-the-quarter-ended-June-2024.pdf (1.7 MB)

Archean Chemical – Specialty Chemical Leader (31-07-2024)

detailed initiating coverage report on Archean chemical by DRChoksey.

DRChoksey_Initiating_Coverage_on_Archean_Chemical_Ltd_with_24%_UPSIDE.pdf (876.4 KB)

next leg of growth will come from bromine derivatives, 50% capex spending is done and benefits will come from FY25.

below is valuation summary

Archean Chemical demonstrated strong resilience in FY24,

maintaining a 35% margin despite revenue and profit growth

moderation. The industrial salt segment’s robust performance

offset declines in bromine revenue. With INR 130-140 crore

already spent on capex, benefits from the bromine derivative

business are expected to materialize starting FY25E. We

project a CAGR of 34% in revenue and 44% in net profit

during FY24-FY26E, driven by volume recovery and new

product lines. Valuing the stock at a P/E multiple of 17.5x

on FY26E EPS, we recommend a BUY with a target price of

INR 943.

Nirlon- Forgotten Story or A sleepy compounder? (31-07-2024)

The problem with this company is that they have a huge debt in the books as a result, the interest payment is eating into their profits. However, as the company wants to declare more dividend, basically they are distributing dividend from the reserves and hence the reserves are depleting. Not sure whether it’s a good decision to invest in this company. Unless the management has a plan to boost their revenue, just by looking at the dividend yield or the property base, it is not advisable to put one’s hard earned money into this stock.

L&T – Bluechip, Value play, Digital giant in making (31-07-2024)

a) Q1 FY25 results: The company’s Q1 FY25 revenues stood at Rs 55,100 crores, up 15% YoY, whereas EBITDA stood at 5,620 crores, up 15% YoY. EBITDA margins stood at 10.2%, flat YoY. PAT stood at Rs 2,800 crores, up 12% YoY. The company’s TTM ROE stood at 14.7% versus 12.8% YoY, partially due to the buyback. Other income was lower due to lower investments pertaining to the share buyback.

P&M EBITDA margins stood at 7.6% versus 7.4% YoY. International revenues constituted 48% of the total revenues in Q1 FY25 (versus 40% YoY). The revenues for the P&M segment were up 18% YoY in Q1 FY25. The company’s CFO stood at negative Rs 500 crores versus negative Rs 990 crores YoY. This is majorly due to the buildup in working capital. Net debt/equity ratio stood at 0.67 versus 0.64 QoQ.

B) Order book status: The company’s order inflows stood at Rs 70,900 crores in Q1 FY25, up 8% YoY aided by strong momentum in the Middle East. The company’s orderbook stood at Rs 4,90,900 crores versus 4,12,600 crores in Q1 FY24, up 19% YoY (and 3% QoQ). 90% of the total order book comes from infrastructure and energy. Slow moving orders are less than 1% of the total order book.

International orders comprised 46% of the total order inflow during the quarter. Of the international order book(38% of the total order book), 92% are from the Middle East, 1% from Africa, and the remaining 7% from Southeast Asia. Of the domestic order book, 14% orders are from the Central Government, 28% are from the state government, 37% are from public sector enterprises, and 21% are from the private sector.

C) Segmental results: Following are the detailed segmental results:

- Infrastructure Project Segment (48.8% of revenues):

a) Segmental revenues stood at Rs 26,908 crores, up 22% YoY. EBITDA margins stood at 5.8% versus 5.1% YoY due to cost savings.

B) Order inflows during the quarter stood at Rs 40,053 crore, flat YoY. International orders constituted 49% of the total order inflow during the quarter.

- Energy Projects Segment (15.41% of revenues):

a) Segmental revenues stood at Rs 8,495 crores, up 27% YoY aided by ramp-up in international projects in the hydrocarbon business. EBITDA margins stood at 8.7% versus 9.1% YoY. However, margins here would be increasing going forward. Hydrocarbon margins were affected due to stage of execution.

B) Order inflows during the quarter stood at Rs 8,792 crores, up 21% YoY. International orders constituted 22% of the total order inflow during the quarter.

C) With regards to nuclear power projects, the company has full scale capability in this segment having worked with the NPCIL across most of their nuclear power plant installations across the country.

- Hi-Tech Manufacturing Segment (3.34% of revenues):

a) Segmental revenues stood at Rs 1,845 crores, up 4% YoY. EBITDA margins stood at 17.4% versus 16.8% YoY.

B) Order inflows during the quarter stood at Rs 3,677 crores, up 100%+ YoY with a receipt of a high value order. Exports constituted 8% of the total order inflows.

- IT & Technology Services Segment (20.8% of revenues):

a) Segmental revenues stood at Rs 11,505 crores, up 6% YoY due to subdued global macro-outlook which impacted discretionary spend. The EBITDA margin for the segment stood at 20% versus 20.6% YoY.

B) The share of this segment in consolidated revenues and operating profit in FY24 stood at 20% and 34% respectively. This segment is a high-margin and less capital-intensive business than the EPC segment, resulting in higher ROCE.

- Others segment (2.5% of revenues):

a) The others segment comprises of (a) Realty (b) Industrial Valves (c) Construction Equipment & Mining Machinery and (d) Rubber Processing Machinery.

B) Segmental revenues stood at Rs 1,375 crores, a de-growth of 37% YoY due to lower handover of residential units in the realty business. EBITDA margins stood at 23.4% versus 18.6% YoY.

D) Outlook: The following is the outlook provided by the management:

-

To enhance its presence in the semiconductor sector, the company has recently entered into a share purchase agreement with SiliConch Systems, a Bengaluru based chip design company.

-

With the change of government in the UK, and a hung parliament in France, the concern about the European economic recovery remains.

-

Countries in the Middle East remain focused on investments in Oil & Gas Infrastructure, Industrialization and Energy Transition.

-

The company has a total prospect pipeline of Rs 9.07 trillion for the remaining nine months of FY25 versus 12 trillion QoQ. This sharp drop is due to the decrease in the hydrocarbons prospect pipeline and some orders that the company did not secure. However, the management has maintained its 10% order inflow guidance as previously stated. A 22-23% hit rate would help meet the order inflow guidance.

-

The company is pursuing EPC opportunities in the Middle East in the oil to chemicals space where investments would be made by the clients.

-

The company has an order book of Rs 5,000 crores in the thermal power business which it will execute, but it will get repurposed to gas-based plants over a period of time. Also, the company has ventured into the offshore wind business and secured the first order. With respect to the green hydrogen, the company will bid for the IOCL tender through its JV with IOCL only.

-

The management aims to maintain a slight improvement in the margin momentum. It has given 8.2% P&M margin guidance for FY25.

-

Over the next 3 years, the bridge from 15% to 18% ROE will be filled through:

-1% from breakeven in the Hyderabad Metro which is currently making losses

-1% from improving margins in the P&M segment

-1% on account of higher payout to shareholders (will now have to evaluate buyback)

-

With regards to the Hyderabad Metro, Rs 2,100 crores are yet to be received from the government.

-

On domestic solar EPC, the company is less aggressive on winning the bids as project size in international geographies is larger. The company is getting traction domestically in the pumped storage project space.

-

With regards to an uptick in domestic revenues, H2 will make up for the lion’s share.

-

Capex for the year would be around Rs 4,000 crores. As of FY24, the company had cash and cash equivalents of Rs 33,200 crores excluding financial services business. And as per CRISIL, the company will earn net cash of Rs 10,000 crores in FY25

E) Key risks: Here are some of the risks that the company faces:

-

All international projects are fixed-price contracts. Volatility in input prices or delays in execution could hurt margins.

-

Losses in the Hyderabad metro remain a key monitorable.

Bharat Electronics Limited (BEL) – Investment & Warfare (31-07-2024)

Company profile: BEL is a leading aerospace and defense electronics company and primarily manufactures advanced electronic products such as radar missile systems, electronic warfare and avionics, anti-submarine warfare, etc.

-

Q1 FY25 results: The company’s revenues stood at Rs 4,105 crores, up 19.10% YoY. EBITDA stood at Rs 948 crores, up 40% YoY. EBITDA margins stood at 22% versus 19% YoY. PAT stood at Rs 776 crores, up 46.2% YoY aided by higher other income. Revenues were aided by the pick-up in execution of the LRSAM order as supply chain disruption to the ongoing conflict in Israel eased in the current quarter. On a QoQ basis, revenue declined 50.4% and EBITDA margin contracted 400 bps as Q4 is the strongest quarter.

-

Order book: The company’s order book stood at Rs 76,705 crores versus 75,934 crores QoQ. The company received orders worth Rs 5,000 crores in Q1 FY25, down 39% YoY due to the elections. Ordering activity however picked up in July’24. Around 10% of the company’s current order book depends on supply of raw materials from Israel.

-

Management commentary: Here is the management commentary post Q1 FY25 results:

-

The management has retained its earlier guidance of 15% revenue growth along with an EBITDA margin guidance of 23-25% along with order inflows of Rs 25,000 crores. This indicates a pickup in margins and execution in the coming quarters.

-

Currently, 80% of the company’s order book are nomination contracts. Margins on these contracts are 7.5% and BHEL enjoys a 12.5% spread over these margins due to cost control and operating efficiencies.

-

The company has indicated five programs each worth Rs 1000 crores which will be the key to order inflows in FY25.

-

In FY26, the company expects Rs 50,000 crore of order inflows led by the Rs 25,000 crore QRSAM order and multiple base orders, which includes MRSAM and HAL’s planned Sukhoi fleet upgrade. The QRSAM order is expected to be placed by Q1 FY26.

-

Non-defense contribution stood at 16% in Q1 FY25 versus 19% in FY24 due to the contribution of EVM and VVPAT machines.

-

The company has planned an annual capex of Rs 700-800 crores for the next 3-4 years for modernizing its facilities and capacity expansion.

-

Other expenses increased by 30% YoY on account of higher liquidated damage provisions.

-

In the non-defense segment, the KAVACH system is also expected to be a big opportunity for the company.

-

The share of defense electronics spending on the total electronics spending is on a rise and BEL will be the beneficiary of the government’s indigenization focus.

Piramal Pharma Limited (31-07-2024)

Company Profile: The company has 17 manufacturing sites with presence in 100+ countries, 500 CDMO customers, 6000+ CHG hospitals and 180k ICH hospitals. As of FY24, the geographical revenue diversification is as follows: North America-41%, Europe-25%, India-20%, Japan-4%, Others-10%.

a) Q1 FY25 results: The company’s Q1 FY25 revenue from operations stood at Rs 1951 crores, up 12% YoY. EBITDA stood at Rs 224 crores, up 31% YoY, whereas EBITDA margins stood at 11% versus 10% YoY driven by operating leverage, cost optimization, and superior revenue mix… Net loss stood at Rs 89 crores versus 99 crores YoY. The company successfully closed the USFDA inspection at the Lexington facility with zero observations. As per CARE ratings, the company’s business intensity (revenue from operations divided by sum of net worth and debt) is expected to improve to 0.85x in FY26 versus 0.6-0.65x in the last three years.

B) Segmental Performance: Following is the detailed segmental performance overview of the company’s business:

CDMO Business (54% of revenues):

-

This segment’s revenues grew 18% YoY.

-

The business continues to witness steady order inflow momentum, particularly for on-patent commercial manufacturing. Management is also seeing early signs of a pick-up in biotech funding with increase in customer enquiries and visits, especially for differentiated offerings.

-

Profitability improved due to healthy revenue growth, better business mix and cost optimization initiatives. The company is also seeing YoY improvement in demand for its generic APIs.

-

Future investments will be geared towards differentiated offerings in ADC, peptides, and on-patent API development and manufacturing.

-

CDMO segment EBITDA margins have improved from 10% in FY23 to 15% in FY24. With around 34% of development revenue from phase III molecules, there is a high probability of these transitioning to product registration and commercial production. Also, 50% of the revenues came from innovation-related work and 64% revenues come from big pharma and emerging pharma. This provides visibility and stability on sales increasing by 10-15% in the near term and improvement in EBITDA margins by 100-200 bps.

-

In FY24, five of the company’s manufacturing facilities which contribute to over half of the CDMO revenues successfully cleared the USFDA inspection.

Complex Hospital Generics (32.3% of revenues):

-

This segment’s revenues grew 2% YoY.

-

The company saw robust demand for Sevoflurance (80% of the global IA market) and Isoflurane in emerging markets like Asia, Europe and RoW, which was partly offset by lower pricing in Sevoflurane in the US. 67% of FY24 CHG revenues came from inhalation anesthesia products and 51% came from the USA.

-

The company is undertaking capacity expansion in the inhalation anesthesia to meet the growing demand. The expected commercialization is in FY26.

-

The growth in the intrathecal portfolio (15% of FY24 CHG revenues) is led by new customer conversion. The company continues to command a 70% market share in intrathecal baclofen in the USA.

-

The company is also investing in portfolio expansion by developing specialty products and signing-in new licensing deals. It has a current pipeline of 24 new products which are at various stages of development and have an addressable market of $2 billion.

India Consumer Healthcare (13.5% of revenues):

-

This segment’s revenue grew 10% YoY.

-

The company added 7 new products and 10 new SKUs in its portfolio in Q1 FY25.

-

Power brands grew 19% YoY in Q1 FY25 and contributed 48% of ICH sales.

-

The company looks to widen its reach across general trade and is also strengthening its presence in alternate channels of distribution.

-

Profitability margins in this segment are in the low single digits. With the increase in sales, CARE ratings expect profitability margins to improve going forward.

C) Debt & Capex: The company’s capex plans for FY25 stand to the tune of Rs 650-750 crores, which would be majorly debt funded. The debt obligations for FY25 stand at Rs 900 crores and the company has prepaid Rs 200 crores worth of NCDs in Q1 FY25. The company has cash and liquid balances of Rs 500-600 crores as of FY24. The company’s net debt-to-EBITDA stood at 2.8x versus 2.9x QoQ.

D) Management Commentary: The following is the management commentary post its Q1 FY25 results:

-

With respect to the profitability in the CDMO business, the management intends to increase it over the medium term through increased capacity utilization and higher contribution from differentiated offerings and innovation-related work.

-

Recent changes in regulations, along with the needs of supply chain diversification are expected to provide medium- to long-term growth opportunities for the CDMO business.

-

In the CHG segment, the company is looking to build a pipeline of limited competition specialty products through investments in R&D and in-house product development capabilities.

-

For FY25, the management has guided for early teens increase in revenue and EBITDA with a meaningful improvement in PAT.

-

The management is seeing early signs of customer enquiries due to the effect of the US BioSecure Act, which aims to source low-cost generic medicines from companies maintaining high quality standards and also encourage R&D on new innovator drugs.

-

With regards to cashflows, the Indian Consumer Healthcare business funds itself, whereas investments in the CDMO and Complex Hospital Generics segment will be managed through internal accruals.

-

In the Complex Hospital Generics business, the company has 5 products approved and 17 are under various stages of approval.

E) Monitorable risks: Here are the key monitorable with respect to the company:

-

Although the company has a clear track record with respect to successfully clearing USFDA inspections, regulatory risk in this industry remains.

-

The company only hedges 45% of its net foreign currency exposures through forward contracts as a part of its hedging policy.

-

Raw material pricing remains a risk which was witnessed in FY22 and FY23 financials leading to moderation in operating margins.

-

The company’s revenues and EBITDA still remain skewed towards H2 of the year. In FY24, 55% of the revenue and 65% of the EBITDA for the full year was earned in H2 FY24.

-

In the CHG business, Sevoflurance constitutes 67% of the total segmental revenues. However, the company is working on reducing this dependence.