Thanks for correction. By mistake mentioned that way though in my mind H2 expected orders was 1200 cr.

Posts tagged Value Pickr

Piccadily Agro Industries Ltd (09-11-2024)

I have found another unexplained discrepancy in the Cash Flow statement. The balance sheet for q2fy25 shows an increase of 229 crore in cash and bank balances compared to balance sheet of q4fy24.

There is no corresponding entry in the Cash flow statement for this increase in the Cash.

Also, like ‘trade receivable’ if the company has any other “Other Receivable” same should be reflected in the ‘Current Assets’ section of the balance sheet which is missing.

Radiant Cash Management Services – Asset Light Play On Cash Logistics (09-11-2024)

RPF is my concern too, in previous years revenue flow averaged to around 16% but in FY 24 there is sudden spike of 4%,

Arkade Developers <> a small cap real estate player (09-11-2024)

In case anyone is interested in listening, I’ve also recorded a podcast on this topic here

Tips Industries Limited – Ready to RACE ahead! (09-11-2024)

This is my Excel for your reference. – Not a very detailed financial model.

Tips Music Valuation.xlsx (21.1 KB)

But, works fine for me for quick decision makings. The key is predicting the growth rate of Tips industries.

MSTC Ltd.: Growth through to E-Commerce (09-11-2024)

Thanks @AkshayBharde for sharing your thoughts.

Could you perhaps list down the anticipated growth triggers and unexpected negative triggers?

ps – I am currently studying the business and trying to build conviction. thanks!

Piccadily Agro Industries Ltd (09-11-2024)

An outlier but good observation in the times when focus is on earnings growth and price momentum. It’s a big jump and does raise curiosity.

- Might be a Typo.

- Might be selling-off receivables to a 3rd party (Factoring) to manage working capital. However, increase in the current assets on the balance sheet excluding Inventory is way lesser than the amount shown under other receivables. So, it can’t be all from the working capital.

I think management should have provided some disclosure in the results. However, It’s best to ask for clarification from the investor relations spoc.

Disc: No position.

Dreamfolks services limited( DFS) (09-11-2024)

Dreamfolks Services Ltd Q2FY25 earnings call summary:

- Highway dining: Benefits based on consumer cards. Issuer will communicate to consumer about outlets where cards can be used.

- Highway dining service is an asset lite model where it is managed by third party.

- Airport lounge footfall is 5.29 Mn for H1FY25.

- At least a year until banks will lift restrictions from their credit cards to spend more on lounge services. Company management unable to comment to revenue commitments from the past.

- Recent technical glitch: Ongoing international integration with a client due to which there was a glitch. Upgrade cycle issue.

- Increase in trade receivables by 140Cr. This was due to cost increase from client. Client exhausted budget for customer expenses.

- Don’t want to be dependent on one client or one service. Long gestation period to see improving revenue from corporate (4-5 yrs).

- Decline seen in customers using lounge services. One bank increased its spending limit on lounge services from Rs. 35,000 to Rs. 75,000.

- Gross margin guidance will remain unchanged i.e. 20%. Will it be reduced? Here management refused to comment.

- Company is providing benefits to card holders. However, service also depends with airlines, corporate, OTS. However, majority sales are from complimentary card holder. Amazon was also selling cards with 25% discount to access the lounge.

Investing Basics – Feel free to ask the most basic questions (09-11-2024)

I have query which is off the topic of investing basics…but may be related to idea ,on market intelligence services.

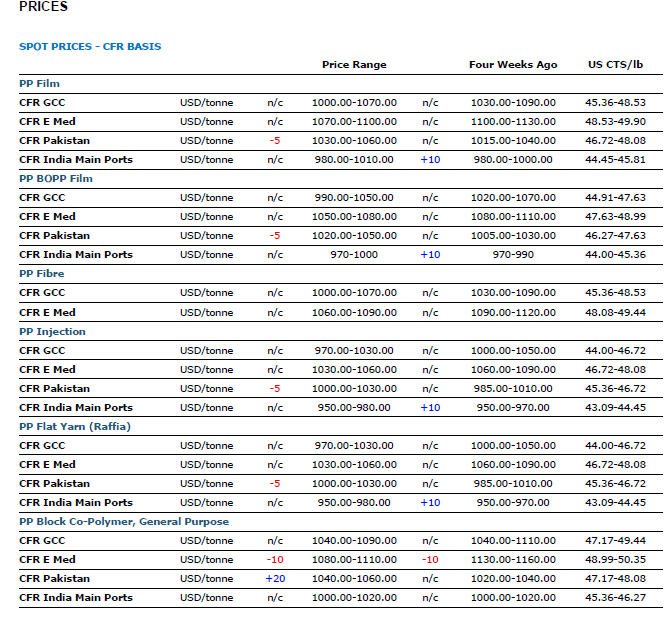

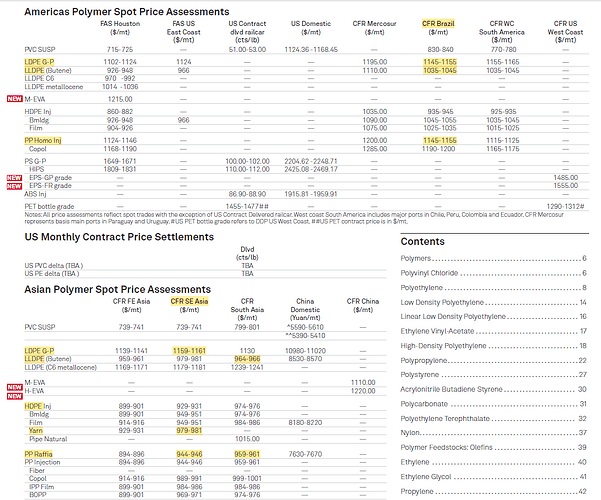

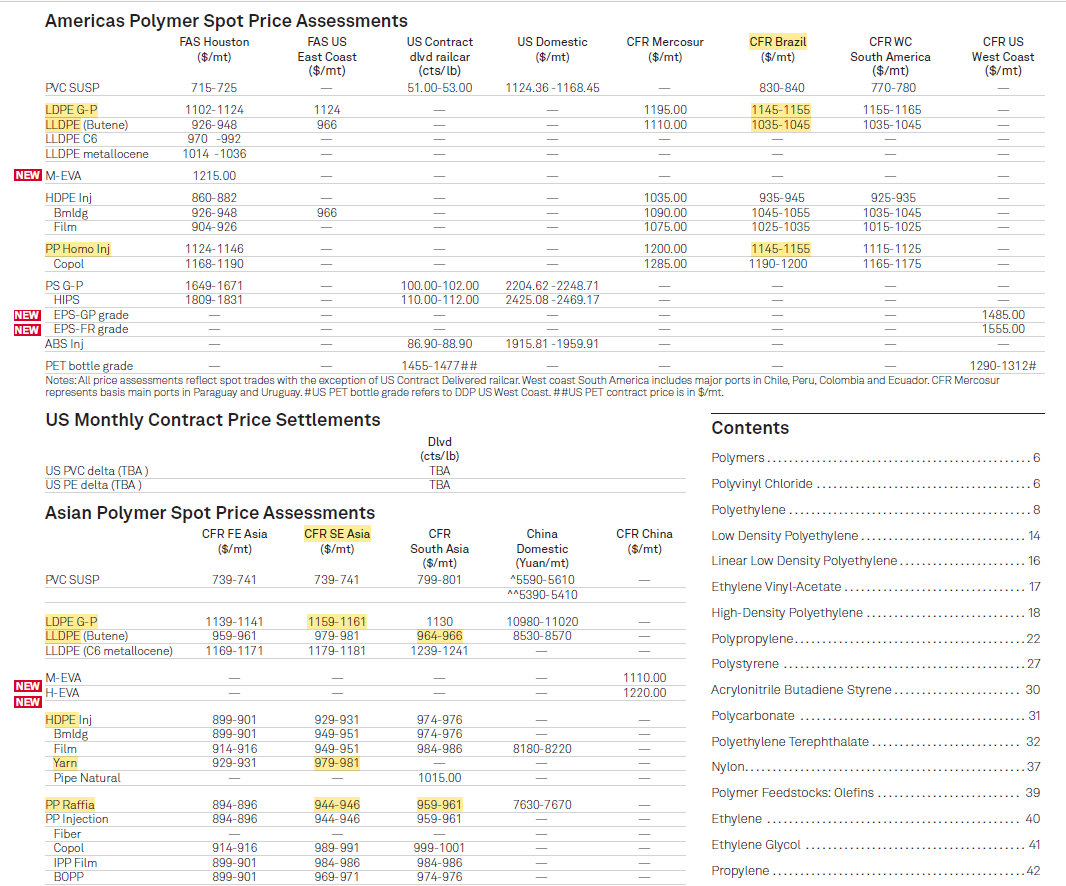

Anyone know, if There is/are any indian service provider who offers polymer market insights.

- Insights by icis – report looks like this.

2.Insight by S&P Platts – Report looks like this

Purpose of asking is to explore an idea, if India has such service providers.

Most of these service providers at present are British/Americans with extremely absurd terms of use.(even though you paid for subscription, if u discontinue subscription you have to delete all the past data, even the data from last 10-15 years ![]() you heard me right, one has paid but data is their property

you heard me right, one has paid but data is their property ![]() )

)

Pricol limited – OEM automotive (09-11-2024)

Pricol Limited Earnings Call Summary – Q2 and H1 FY25

Financial Performance

- Q2 FY25: Revenue from operations reached 6,500 million with an EBITDA of 871 million (13.4% margin). Profit after tax (PAT) was 450 million (6.93% margin), resulting in an EPS of 3.70 Rupees per share.

- H1 FY25: Total sales were approximately 12,530 million, with an EBITDA of 1,677 million (13.39% margin) and a PAT of 906 million (7.23% margin). EPS for the half-year stood at 7.44 Rupees.

- The company reported zero long-term borrowings and maintained comfortable cash reserves as of September 30th.

- Year-over-year growth for both the quarter and half-year was around 15.5%, despite a slowdown in the automotive industry during Q2. EBITDA grew by approximately 24% for the quarter and 23% for the half-year.

Margin Guidance

- Management aims to maintain an EBITDA margin of 13-13.5%.

- Margins are expected to improve by approximately 50 basis points with the resumption of exports, which were significantly lower than expected this quarter due to US election-related factors.

- Wage increases implemented on July 1st have impacted margins, but productivity improvements are expected to offset this in the future.

Business Segment Performance

- The company experienced muted sales in the automotive industry during Q2, reflecting a broader industry trend.

- Exports were significantly weaker than anticipated due to policy changes under the new Republican government in the US, impacting both revenue and margins.

- Disc brake production has commenced, with supplies to six manufacturers. A ramp-up phase and significant volume increases are expected in FY26.

- Battery management system (BMS) products are still in the testing phase and have not yet generated revenue. Management is cautious about the BMS market’s fragmentation and unclear trajectory.

- Smart cockpits and connected vehicle solutions are showing traction and are considered a significant growth opportunity.

- Mechanical clusters currently contribute approximately 30% of revenue but are expected to decline, with LCD and TFT displays gaining prominence.

Future Guidance

- Management maintains its target of reaching 3200 crores in revenue by FY26 through a combination of organic and inorganic growth.

- The company is actively exploring inorganic opportunities in the railway and defense segments to drive higher margins and growth. However, these initiatives are in the early stages.

- Pricol is open to acquisitions in allied areas and is comfortable raising up to 300 crores in debt to fund strategic acquisitions.

- Capital expenditure (CAPEX) for the full year is expected to be around 200 crores, consistent with the previously stated plan of 600 crores over three years. The CAPEX allocation includes building new plants, expanding existing facilities, upgrading production lines, and investing in new machinery.

Key Risks & Industry Outlook

- Muted demand in the domestic automotive industry is a key risk, with Q3 FY25 anticipated to be particularly weak.

- Uncertainty surrounding export demand due to US policy changes poses a challenge to revenue and margin projections.

- The slow adoption of EVs is not a significant concern as Pricol’s products are propulsion-agnostic. The company is collaborating with various EV manufacturers.

- The fragmented BMS market presents challenges in predicting future revenue.

Disc: Invested