Don’t trust the numbers blindly. Check Manpasand Beverages for example, during its growth years. On the top of it, Deloitte was its auditor throughout all the years when Manpasand was showing phenomenal year on year growth. A similar company in today’s time will be Mishtann foods. It might trigger all the right flags, but you still shouldn’t invest in it

Posts tagged Value Pickr

Nuvama Wealth Management: Proxy to Affluent India (29-07-2024)

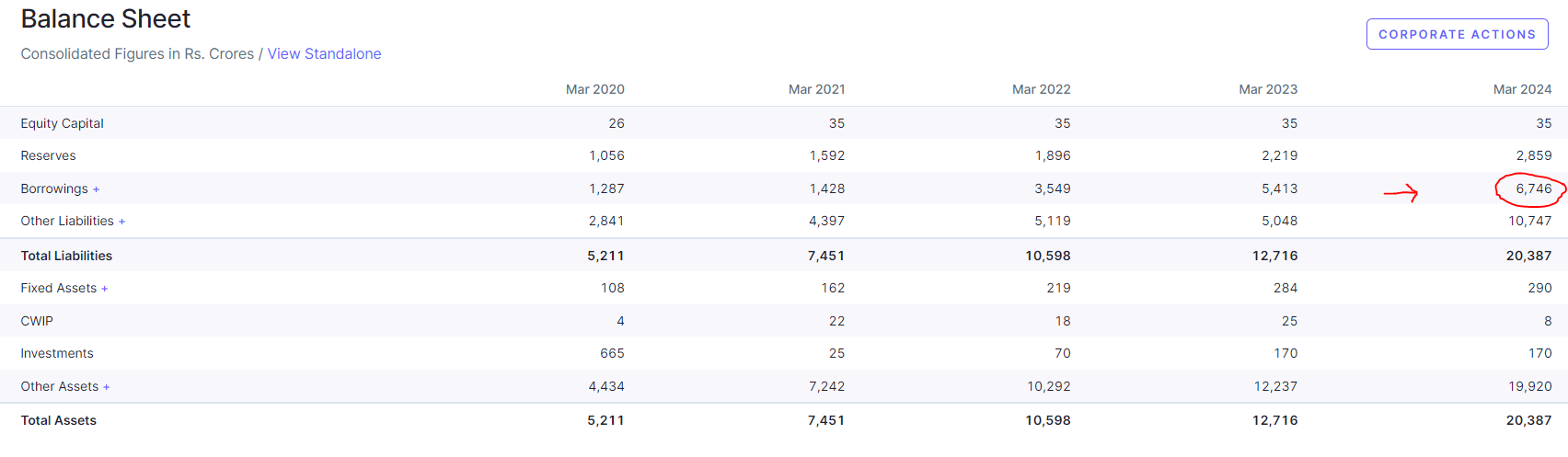

Hi Guys, I am studying this company. I got stuck at borrowing parameter. Can anyone help me to understand, having such big borrowing 6,746 is it concerning? Or I am missing something ?

Panchsheel Organics Ltd (29-07-2024)

Hello Investors,

I am creating this post since could not able to find a dedicated thread on Panchsheel Organics Ltd. (POL).

Industry Overview

• Panchsheel Organic Ltd. operates in the pharmaceutical industry.

• The current market size of this industry is ₹ 543 lakh Cr. (US$ 65 billion). India’s

pharmaceuticals industry is expected to reach US$ 130 billion by 2030, and US$

450 billion by 2047.

• During FY18 to FY23, the Indian pharmaceutical industry logged a compound

annual growth rate (CAGR) of 6-8%.

• Major competitors of POL are Hikal, Aarti Drugs, Gujarat Themis Biosyn, etc.

Company Overview

• Panchsheel Organics Ltd is a manufacturer of Bulk Drugs and Intermediate.

• Panchsheel an ISO CERTIFIED, GMP (Good Manufacturing Practices) approved, maintaining WHO Standards, a public listed company (listed on BSE) are manufacturer and exporter of Active Pharma Ingredients (APIs), Intermediates & Finished Formulations (both Human & Veterinary) having a wide experience of more than three decades in the healthcare field.

• The company has its corporate office in Mumbai and has two multipurpose manufacturing unit is situated in Indore (120 TPA to manufacture APIs) and Pithampur.

Products Categories

• Bulk Drugs & API Intermediates

• Steroids & Hormones

• Pharma Pellets of all ranges with different potencies.

• Pharma Formulations (Finished Products).

• Veterinary Products

• Agri Biotech products. (Bio Fertilizers, Bio Stimulants, Growth Promoters)

• Probiotics & Enzymes

Capex Plans

Phase 1:

- This capex plan is comprised of ₹ 40 Cr. at Pithampur, Indore (MP) for Probiotics & Enzymes.

- Capacity of 36-40 TPA.

- The funds were sourced through a mix of preferential allotment and warrants in September 2022 and the remaining done through Internal Accruals.

- Revenue potential is around ₹40-50 cr. once the full capacity is available in FY25.

Phase 2:

- This capex plan is comprised of an initial investment of ₹50-70 Cr. at DMIC Vikram Udyogpuri Biotech Park Near Indore (MP) for fermentation-based and API-based pharmaceuticals.

- Capacity for fermentation-based pharmaceuticals is around 36-40 TPA and for API-based pharmaceuticals is around 120 TPA.

- The funds were sourced through a mix of preferential allotment and warrants, Internal Accruals, and Debt/Equity (if needed).

- Revenue potential for fermentation is around 40-50 Cr. and up to 100-120 for API.

Corporate Actions

• The company has issued and allotted 17,75,950 Equity Shares on a preferential basis in September 2022.

• The company has also undertaken the bonus issue of shares in a 1:1 ratio in December 2021.

• The company is very regular in dividend payments with an average of 12-15% over the last 10 years.

SWOT Analysis

Strength:

• Very low debt (6 Cr. 3.7% of Balance Sheet).

• Constant growth in revenue and net profit.

• The pharma industry is expected to reach 130 billion US$ by 2030 which is currently at 65 billion US$ (More potential for revenue and profit).

• Rise in Cash Flow from Operation activity.

• Zero promoter pledge.

Weakness:

• Decrease in RoE (17% to 13%) this year.

• Decreases in RoCE (27% to 17%) this year.

• Dependency of products on the availability of raw materials.

Opportunity:

• Upcoming Capex plans help to generate more revenue and net profit.

• The Company has a wide range of pharmaceutical products in its portfolio.

• Export market opportunities.

Threat:

• Continues decrease in promoter holding.

• Rise in the cost of raw materials.

Key Clientele

• Swiss Granier Life Science

• Abbott

• Madras Pharma

• Akums

• Zydus

• Hetero Healthcare

• Ajanta Pharma Limited

• MacLeod’s Pharmaceutical Ltd.

• Aristo Pharmaceutical Pvt Ltd.

• Intas Pharmaceutical Pvt Ltd.

Key Financials

• Market Cap – 331 Cr

• Current Price – ₹ 281

• High / Low – ₹ 288 / 160

• Stock P/E – 23.4

• Book Value – ₹ 106

• ROE – 13.1 %

• ROCE – 17.4 %

• Price to book value – 2.64

• D/E – 0.05

• EPS – 11.98

• Promoter Holding – 56.12%

• Sales – 105 Cr.

• PAT – 14 Cr.

• Balance Sheet – 159 Cr.

• Borrowings – 6 Cr.

• Working Capital – 79 Cr.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (29-07-2024)

I am a little confused here. As per my understanding 71.15 Cr of NCDs (43.65 from NCD-1 and 27.5 Cr from NCD-2) was left. This clearance should only be a part of the NCD clearance or are they saying both the NCDs are cleared?

Company has certainly delivered on their promise of NCD clearance by July / Aug and their pledge has also cleared. Re-rating seems likely in the near future

Aavas Financiers :: Banking on the unbanked (29-07-2024)

Q1FY25 Concall Summary

Business Updates

- The AUM was up by 22% yoy and this aligns with the company’s guidance of 20-25% yoy

- In terms of liability the company continues to maintain a diverse mix and have started exploring co lending

- The borrowing rates have peaked out and incremental borrowing costs went up by 17 bps yoy

- 30 million additional houses will be included in the PM Aawas scheme which was announced in the recent budget

- The overall borrowing costs went up by 1 bps qoq during the quarter

Participants

Equirus

Elara Capital

Ambit Capital

B&K Securities

Philip Capital

Citigroup

Oxbow

Dolat Capital

MSA Capital Partners

QnA

- The growth was lower because disbursements were lower than sanctions

- The sanctions to disbursements ratio will pick up to the earlier ratio of around 87% in the next few quarters which will lead to disbursements picking up

- A lot of borrowings is linked to repo rates so as the rates start to come down it will also have a downward impact on cost of borrowings

- The guidance will remain at the earlier stated target of 20-25% on the AUM going forward as well

- There is a one time setoff and the ESOP cost has gotten reversed which led to the decline in employee costs

- In last few years the company has gone through a technology transformation through both Salesforce and then Oracle changing the whole experience for the company and customer

- The company has upgraded and changed some peripheral softwares as well and this will lead to a total capitalization of around Rs 45 crores and this will benefit over the next decade

- This is the final year of capitalization and combined amount over 2 years is Rs 45-50 crores

- There is no change in the way NIM is being reported and in Q1 the reason why NIM is lower is because of muted assignment income and higher incremental cost of borrowings and a consequent fall in spreads

- The company has never had the objective of building a loan book based on subsidy scheme announcements by the government and idea will be to go for the same customer profile of those building homes for self usage

- The clear focus remains on self construction in Tier 3-5 towns and the growth projections are not based on any subsidy scheme

- The four main states are Rajasthan, Gujarat, Madhya Pradesh and Maharashtra and of the 371 branches there are 108 branches in Rajasthan

NPST – Technology Provider for UPI Tech (29-07-2024)

How much stock will rally is not a proxy of how much it has already grown but rather the growth rate and valuation it is at right now. While trailing PE for the stock is quite high 2 years forward-looking looks very justifiable for a high growth company.

Cera SanitaryWare Ltd (29-07-2024)

ConCall Summary – May 2024

FINANCIAL PERFORMANCE

- Revenue increased by INR 547 crore during the quarter, reflecting a growth of 2.6% compared to the same period in the previous year

- EBITDA and EBITDA margins notably increased in Q4 FY 2024

- Gross margin declined due to higher discount offers but offset by cost optimization efforts

- Cash and cash equivalents as of March 31, 2024, increased by 20.5% compared to the previous year

MARKET CONDITIONS AND STRATEGY

- Management anticipates sluggish demand conditions to continue in Q1 FY 2025

- Sales target recalibrated to March 2027 due to market conditions

- Focus on premium and luxury segments expecting growth in luxury segment

- Introduction of new products with innovative designs for luxury customers

- Launching dedicated brand stores for premium offerings

- Commitment to traditional segments while advancing in premium market stance

- Increase in new design and product launches, accounting for 30-35% of total sales

OPERATIONAL UPDATES

- Company maintained and slightly improved its sales compared to the previous year despite challenging market conditions

- Strong track record of retaining top talent at Cera

- Introduction of an ESOP scheme to motivate and reward key human resources

- Multiple initiatives underway including capacity expansion, product development, advertising, and marketing

OUTLOOK AND GROWTH INITIATIVES

- Optimistic that demand situation will improve post Q1 FY 2025

- Real estate upswing expected to positively impact projects and demand

- No price rise in sanitary ware for the past 20 months, recent 2% increase in February 2024 to offset input costs

- Cost-saving program and margin improvement efforts expected to continue in FY 2025

SALES AND DISTRIBUTION

- Dealers common for sanitary ware and faucet ware

- Continuous process of enrolling new dealers to reach new areas

- Slow demand affecting sales despite increased distribution touchpoints

- Market size estimates for sanitary ware and faucet ware

- No significant loss of market share expected despite sluggish market conditions

PRODUCT SEGMENTS

- Premium mix percentages for different product segments

- Explanation on decline in gross margins and offsetting initiatives

COMPETITION

- Competition from new players entering the industry

- New competitors sourcing from outsourcing partners, limited dealer network

- Management plans to rejuvenate the Senator brand and focus on the luxury segment

FINANCIAL GUIDANCE

- Target for luxury brands to contribute 8% to 10% of total turnover by 2,900

- Premium for luxury brands compared to Cera premium brands expected to be 60% to 70%

- Price hikes dependent on market conditions and competitor reactions

- Focus on cost optimization to protect margins in the current market scenario

- Margins expected to improve as demand situations improve

- Cash reserves around INR 828 crores as of March 2024, with approved dividends of INR 60 per share

- Revenue CAGR guidance of 16% based on volume increase of 10% to 13%, mix benefit of 4% to 6%, and price impact of 2% to 3%

FUTURE PLANS

- Routine capex for the next financial year around INR 25.4 crores

- Greenfield expansion for sanitary ware estimated at INR 150 crores

- Capacity utilization and expansion plans

Vimta Labs Ltd (VLL) (29-07-2024)

ConCall Summary – June 2024

MANAGEMENT TEAM

- Ms. Harita Vasireddi – Managing Director

- Mr. Satya Sreenivasa Neerukonda – Executive Director

- Mr. Narahari Naidu – Chief Financial Officer

- Ms. Sujani Vasireddi – Company Secretary

COMPANY VIEWS AND COMMITMENTS

- Emphasis on quality and innovation in the life sciences sector

- Commitment to quality and innovation in the life sciences sector

- Focus on growth drivers and maintaining margins

FINANCIAL HIGHLIGHTS

- Revenue, EBITDA, and PAT figures for Q1 FY ’25

- EBITDA margin improved by 50 basis points YoY

- Profit after tax increased by 0.7% YoY with a PAT margin improvement of 40 basis points

- Cash and cash equivalents stood at INR 324 million with total borrowing of INR 130 million

- Debt-to-equity ratio at 0.04x

- Capex for the quarter was INR 164 million

BUSINESS GROWTH AND EXPANSION

- Stable business growth despite capacity constraints

- Successful FDA remote audit with no observations

- Received grants for upgrading food testing laboratories

- Plans to double capacity with new buildings at the Life Sciences facility in Hyderabad

- Restrategized services portfolio for growth in various sectors

FUTURE PLANS

- Commercialization of the new Life Sciences plant facility by Q2 of the financial year

- Focus on improving efficiencies and productivity for stable margins

- Majority of upcoming capex allocated to pharma and food segments

- Investing in infrastructure for future growth

INDUSTRY OUTLOOK

- Positive outlook on the electronics industry in India

- Confidence in the industry’s vibrancy and potential for growth

- Expectation of revenue growth and proliferation of labs in South and North India

COMMERCIAL PRODUCTION

- Commercial production at the new facility expected to start in Q2 of the current year

- Ramp-up in production planned but exact percentage increase for the next financial year not specified

FOCUS ON OPERATIONS AND EFFICIENCY

- Management is focused on efficient operations and minimizing impacts on the business.

- The company has incurred INR 275 crores in capex for facility expansion and growth.

- The company does not have internal R&D but focuses on developing more efficient methods for customers.

GROWTH EXPECTATIONS

- The company expects growth from food, electronics, and pharma sectors.

- The Indian analytical services market is growing faster than the global industry.

RESEARCH AND DEVELOPMENT

- The company is involved in new molecule research from concept phase to clinical trials.

- The company directly works with companies at the clinical trial stage.

SHIFT IN FOCUS

- The company has shifted focus from supporting the generic industry to also supporting clinical trials in the patient population.

- The company has doubled its capacity in the last 2 years and is adding a new chamber for electronic business.

FINANCIAL OUTLOOK

- Management’s focus is on pushing the top line while aiming to maintain margins.

- Despite being in a human resource-intensive industry with growing input costs, the company has been focusing on profit-making services and maintaining margins.

EXPANSION PLANS

- The company is considering adding the next chamber in a different city, with Pune and Bangalore being good options.

- The new facility is capable of handling NCEs.

CLINICAL TRIALS OPERATIONS

- Clinical trials are multisite trials conducted at third-party hospital setups.

- Revenue recognition for clinical trials is based on performance completion milestones.

MARGIN IMPROVEMENT

- The company expects margins for the new trial to be in line with existing margins and is putting efforts to improve margins going forward.

- The company aims to maintain or improve margins going forward.

Titan Intech Limited: Empowering Data Center Infrastructure (Turnaround story?) (29-07-2024)

Yeah that makes sense! Thanks for simplifying tge underlying tone for me… but still if you see the PnL statement of the co the OP both short and long term are constantly on the rise…

Motilal Oswal Financial Services (29-07-2024)

Motilal is 4x from last year when I explained there is huge margin of safety. These opportunities come very rarely and you should allocate heavy and then let compounding do it’s magic. It was my top allocation and yes you could always add more in hindsight but it had reached my maximum allocation. Yes all its earnings are linked to market but it was great play to FnO mania that’s going on. You are casino owner and collect money from gamblers.