Can anyone is having 20 Microns Ltd pure peers list in india

Posts tagged Value Pickr

SG Mart- Can it successfully create a marketplace? (27-07-2024)

HI can you please quote the source of this data? Thanks

SG Mart- Can it successfully create a marketplace? (27-07-2024)

HI can you please quote the source of this data? Thanks

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (27-07-2024)

I was meaning to post a detailed analysis of this company for sometime now. Let me know in case of any feedback or something I can add to my analysis ![]()

- What does the company do?

-

Company has 5 decades of experience in hotels, first hotel started in Mumbai

-

Headed by Vishal Kamat (3rd generation) since 27th May ‘23

-

Hotels:

- 16 in 4 and 5-star categories

- 1637 keys

- 372 owned, 36 on mgmt. contract and 48 in Goa is free holding meaning the company owns the hotel, land (currently used as collateral for loan)

- Rest 72% are leased; model is asset light similar to LemonTree which has ~60% owned or leased hotels and similarly Indian Hotels also has 60% leased or managed

- ARR: 6,500

-

Owns 5 brands:

-

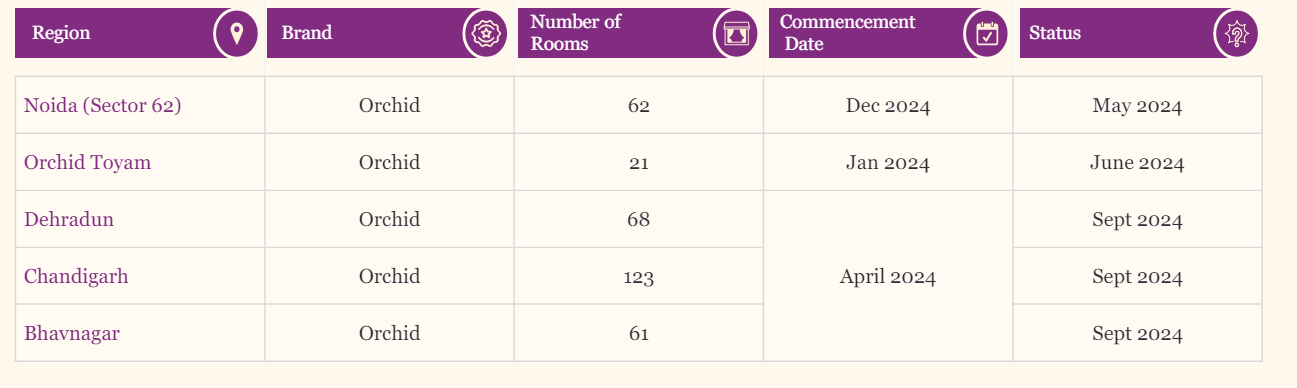

Orchid: 6 hotels (5 upcoming). Ecotel 5-star hotel chain

– FY24 Occupancy is 55% from 75% in FY19, occupancy of other hotels in the 5-star segment is much higher – 72% for Lemontree and 80% for Taj. As per Kamat’s management, this is because a lot of their properties are small which doesn’t allow them to host large events

– ARR in this segment is expected to increase by 5-12% as per industry estimates. Kamat management has guided for 15% increase which seems aggressive -

Ira (4-star): 5 hotels. New branding from July-23, earlier it was VITS

-

Lotus resorts (4-star): 3 hotels. Occupancy at 54% in FY24 from 50% in FY19

-

Fort Jadhavgarh (5-star)

– FY24 Occupancy is 40% from 55% in FY23: Larger hotels have an advantage of being flexible and being able to take more kind of functions so occupancy is a challenge here

– ARR is 8,364 increasing at 6% CAGR -

Mahodadhi Palace (5-star): JV with 51% stake. 33 rooms currently, which will be expanded to 120

-

- Why is Kamat Hotels a good investment?

- This is a classic turn-around story with PAT to increase due to decrease in debt along with potential PE re-rating when compared to its peers in the hospitality sector.

- Company took on huge debt for its Pune hotel and was unable to service it in 2014 due to slowdown in Indian economy, especially the hospitality sector

- Debt reduction from 664 Cr in FY16 to 265 Cr in FY24

- What will it turnaround or increase its earnings?

– Guidance of hotel sales and operating profit growth

1. Revenue: 315 Cr to 400 Cr in FY25 (27% increment)

2. EBITDA: Between 30-35% -> 130 Cr in FY25

- Savings from balance sheet and other items

- Levers for hotel sales growth

1. ARR and Occupancy increase

* ARR: FY25 company is guiding for 15% ARR increase (looks unlikely)

* Occupancy: Existing main hotels are already at their peak performance in terms of 85% for the year. Rest of the hotels are smaller and their occupancy seems unlikely to increase

2. New launches

* Planned: 335 keys (20% increase) in 5 locations till Dec 24

- Not yet announced: 300+ additional keys (addn. 20%+, so overall 40% increase) in 4 new locations (no launch date). 87 rooms to come from Mahodadhi Place in FY26

- Adding new keys is easy because company only needs to invest in lighter material (linen, crockery) which is 0.3 to 0.7 Cr per hotel and other additional costs are manpower related

– F&B: Contributes 37% to sales

- Financials

- Debt: Interest expenses expected to decline by 53%

| FY24 | FY25 | Interest rate | |

|---|---|---|---|

| NCD-1 borrowing | 297.5 | 43.65 | 21% |

| Interest on NCD-1 (till mid-Oct when VITS was sold) | 44.3 | 9.2 | |

| Remaining Interest on NCD-1 (mid-Oct to Mar) | 10.6 | 0 | |

| NCD-2 borrowing | 27.5 | 27.5 | 21% |

| Interest on NCD-2 | 5.8 | 5.8 | |

| Alternate financing | 0 | 128.85 | 11% |

| Interest on alternate financing | 0 | 13.9 | |

| Total debt | 325 | 200 | |

| Total interest | 60.6 | 28.8 | -53% |

- Company is paying lease of 20 Cr for VITS hotel

- Warrants are due in July 24. So EPS will come down and PE will go up

5. Valuation:

| FY24 | FY25 (E) | YoY | |

|---|---|---|---|

| Sales (as per guidance) | 304 | 400 | 32% |

| EBITDA | 91 | 120 | |

| EBITDA (%) – conservative est. considering lease and new keys | 30% | 30% | |

| Other Income | 12 | 16 | |

| Dep | 18 | 18 | |

| Interest | 60.6 | 28.8 | |

| PBT | 24.4 | 88.7 | 264% |

| Tax | 17% | 17% | |

| PAT (excl. exceptional items) | 20.3 | 73.6 | 264% |

| PAT (%) | 6.7% | 6.7% | |

| PAT + exceptional items + savings | 45 | 73.6 | 64% |

| No. of shares (post warrant dilution in July-24) | 2.95 | 2.95 | |

| EPS (excl exceptional items and incl. savings) | 6.9 | 25.0 | |

| CMP | 227 | 227 | |

| PE (current) | 33.1 | 9.1 | |

| Exit PE (assumed) | 30 | ||

| Price (est) | 749 | ||

| Upside | +230% |

- Competitive analysis and industry benchmarking

-

Lemon Tree:

- The number of people who use branded hotel rooms will grow 3-5x in the next five years. In China and Indonesia, around 2006-07, when they were at this point in their economy, hotel room demand grew over 22% every year

- 13% ARR increase in FY24

- Management: “My forward view is, now I think the whole industry will wait for the upcycle, which is imminent in my opinion. At which point, you will see further significant hikes. Otherwise, typically, the hikes you will see will be depending on the market and depending on the quality of hotel, it could be anywhere from 5% to 12%.”

- The first point is that the segment that took off first, because it had the lowest base, was luxury and 2 years lag, then mid-market took off. I think we are seeing the same thing in India. You will notice luxury operators are showing a much higher growth in ARR than the mid-market

- What I can say is for Lemon Tree certainly, we will see at least a 15% increase in revenue every year for the next 3 years. And this will partly be led by ARR increase, partly by occupancy and partly by management contract business increasing. The minimum we expect is 15% increase.”

- Company wants to be debt free in 4 years

- In 2006, 2007, 2008 and 2009 until the global financial crisis, the average rate of Lemon Tree which did not have a Lemon Tree Premier, it only had Lemon Trees and Red Foxes, the ARR was Rs. 9,000. Actually, we are below what was there 15-18 years ago. And that is true, by the way, for every hotel company that had hotels there. There is an ability to reprice.

- I do not see much competition very frankly because of a very basic reason, it is that demand is growing. When demand grows, then everybody runs like horses. It does not matter what you were in your previous avatar, but everybody becomes a racehorse. Obviously, there is competition in terms of similar hotels going after similar accounts and retail customers. I can sense the early tide of a rising wave of demand. And I think that’s going to quite distinctly get demonstrated in the next 15 months.

- Mumbai, Delhi are large markets where demand will always outpace supply

-

IHL:

- Experts like Horwath HTL have predicted that demand will grow at a rate of over 10-11% annually for the next 3 to 4 years. while the supply will continue to lack demand. Most of the future supply is expected to come outside of the key markets for non tier-1 cities

- The ARR is really all about the part of the business, 47% of our business is room revenue. There’s everything else in terms of F&B, in terms of the asset light businesses, the banqueting, the chambers and a whole bunch of other things actually

-

CareEdge ratings:

- It’s not just leisure hotels and resorts that are driving up and sustaining room rates—there is sustained demand for city hotels from the domestic business traveller, as well.

- Amid all this, supply is estimated to record a compound annual growth rate of 4% to 5% over the next four-five years, said the CareEdge Ratings report, adding just 50,000 rooms to the country’s current inventory of approximately 160,000 branded rooms

Discl: Invested

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (27-07-2024)

I was meaning to post a detailed analysis of this company for sometime now. Let me know in case of any feedback or something I can add to my analysis ![]()

- What does the company do?

-

Company has 5 decades of experience in hotels, first hotel started in Mumbai

-

Headed by Vishal Kamat (3rd generation) since 27th May ‘23

-

Hotels:

- 16 in 4 and 5-star categories

- 1637 keys

- 372 owned, 36 on mgmt. contract and 48 in Goa is free holding meaning the company owns the hotel, land (currently used as collateral for loan)

- Rest 72% are leased; model is asset light similar to LemonTree which has ~60% owned or leased hotels and similarly Indian Hotels also has 60% leased or managed

- ARR: 6,500

-

Owns 5 brands:

-

Orchid: 6 hotels (5 upcoming). Ecotel 5-star hotel chain

– FY24 Occupancy is 55% from 75% in FY19, occupancy of other hotels in the 5-star segment is much higher – 72% for Lemontree and 80% for Taj. As per Kamat’s management, this is because a lot of their properties are small which doesn’t allow them to host large events

– ARR in this segment is expected to increase by 5-12% as per industry estimates. Kamat management has guided for 15% increase which seems aggressive -

Ira (4-star): 5 hotels. New branding from July-23, earlier it was VITS

-

Lotus resorts (4-star): 3 hotels. Occupancy at 54% in FY24 from 50% in FY19

-

Fort Jadhavgarh (5-star)

– FY24 Occupancy is 40% from 55% in FY23: Larger hotels have an advantage of being flexible and being able to take more kind of functions so occupancy is a challenge here

– ARR is 8,364 increasing at 6% CAGR -

Mahodadhi Palace (5-star): JV with 51% stake. 33 rooms currently, which will be expanded to 120

-

- Why is Kamat Hotels a good investment?

- This is a classic turn-around story with PAT to increase due to decrease in debt along with potential PE re-rating when compared to its peers in the hospitality sector.

- Company took on huge debt for its Pune hotel and was unable to service it in 2014 due to slowdown in Indian economy, especially the hospitality sector

- Debt reduction from 664 Cr in FY16 to 265 Cr in FY24

- What will it turnaround or increase its earnings?

– Guidance of hotel sales and operating profit growth

1. Revenue: 315 Cr to 400 Cr in FY25 (27% increment)

2. EBITDA: Between 30-35% -> 130 Cr in FY25

- Savings from balance sheet and other items

- Levers for hotel sales growth

1. ARR and Occupancy increase

* ARR: FY25 company is guiding for 15% ARR increase (looks unlikely)

* Occupancy: Existing main hotels are already at their peak performance in terms of 85% for the year. Rest of the hotels are smaller and their occupancy seems unlikely to increase

2. New launches

* Planned: 335 keys (20% increase) in 5 locations till Dec 24

- Not yet announced: 300+ additional keys (addn. 20%+, so overall 40% increase) in 4 new locations (no launch date). 87 rooms to come from Mahodadhi Place in FY26

- Adding new keys is easy because company only needs to invest in lighter material (linen, crockery) which is 0.3 to 0.7 Cr per hotel and other additional costs are manpower related

– F&B: Contributes 37% to sales

- Financials

- Debt: Interest expenses expected to decline by 53%

| FY24 | FY25 | Interest rate | |

|---|---|---|---|

| NCD-1 borrowing | 297.5 | 43.65 | 21% |

| Interest on NCD-1 (till mid-Oct when VITS was sold) | 44.3 | 9.2 | |

| Remaining Interest on NCD-1 (mid-Oct to Mar) | 10.6 | 0 | |

| NCD-2 borrowing | 27.5 | 27.5 | 21% |

| Interest on NCD-2 | 5.8 | 5.8 | |

| Alternate financing | 0 | 128.85 | 11% |

| Interest on alternate financing | 0 | 13.9 | |

| Total debt | 325 | 200 | |

| Total interest | 60.6 | 28.8 | -53% |

- Company is paying lease of 20 Cr for VITS hotel

- Warrants are due in July 24. So EPS will come down and PE will go up

5. Valuation:

| FY24 | FY25 (E) | YoY | |

|---|---|---|---|

| Sales (as per guidance) | 304 | 400 | 32% |

| EBITDA | 91 | 120 | |

| EBITDA (%) – conservative est. considering lease and new keys | 30% | 30% | |

| Other Income | 12 | 16 | |

| Dep | 18 | 18 | |

| Interest | 60.6 | 28.8 | |

| PBT | 24.4 | 88.7 | 264% |

| Tax | 17% | 17% | |

| PAT (excl. exceptional items) | 20.3 | 73.6 | 264% |

| PAT (%) | 6.7% | 6.7% | |

| PAT + exceptional items + savings | 45 | 73.6 | 64% |

| No. of shares (post warrant dilution in July-24) | 2.95 | 2.95 | |

| EPS (excl exceptional items and incl. savings) | 6.9 | 25.0 | |

| CMP | 227 | 227 | |

| PE (current) | 33.1 | 9.1 | |

| Exit PE (assumed) | 30 | ||

| Price (est) | 749 | ||

| Upside | +230% |

- Competitive analysis and industry benchmarking

-

Lemon Tree:

- The number of people who use branded hotel rooms will grow 3-5x in the next five years. In China and Indonesia, around 2006-07, when they were at this point in their economy, hotel room demand grew over 22% every year

- 13% ARR increase in FY24

- Management: “My forward view is, now I think the whole industry will wait for the upcycle, which is imminent in my opinion. At which point, you will see further significant hikes. Otherwise, typically, the hikes you will see will be depending on the market and depending on the quality of hotel, it could be anywhere from 5% to 12%.”

- The first point is that the segment that took off first, because it had the lowest base, was luxury and 2 years lag, then mid-market took off. I think we are seeing the same thing in India. You will notice luxury operators are showing a much higher growth in ARR than the mid-market

- What I can say is for Lemon Tree certainly, we will see at least a 15% increase in revenue every year for the next 3 years. And this will partly be led by ARR increase, partly by occupancy and partly by management contract business increasing. The minimum we expect is 15% increase.”

- Company wants to be debt free in 4 years

- In 2006, 2007, 2008 and 2009 until the global financial crisis, the average rate of Lemon Tree which did not have a Lemon Tree Premier, it only had Lemon Trees and Red Foxes, the ARR was Rs. 9,000. Actually, we are below what was there 15-18 years ago. And that is true, by the way, for every hotel company that had hotels there. There is an ability to reprice.

- I do not see much competition very frankly because of a very basic reason, it is that demand is growing. When demand grows, then everybody runs like horses. It does not matter what you were in your previous avatar, but everybody becomes a racehorse. Obviously, there is competition in terms of similar hotels going after similar accounts and retail customers. I can sense the early tide of a rising wave of demand. And I think that’s going to quite distinctly get demonstrated in the next 15 months.

- Mumbai, Delhi are large markets where demand will always outpace supply

-

IHL:

- Experts like Horwath HTL have predicted that demand will grow at a rate of over 10-11% annually for the next 3 to 4 years. while the supply will continue to lack demand. Most of the future supply is expected to come outside of the key markets for non tier-1 cities

- The ARR is really all about the part of the business, 47% of our business is room revenue. There’s everything else in terms of F&B, in terms of the asset light businesses, the banqueting, the chambers and a whole bunch of other things actually

-

CareEdge ratings:

- It’s not just leisure hotels and resorts that are driving up and sustaining room rates—there is sustained demand for city hotels from the domestic business traveller, as well.

- Amid all this, supply is estimated to record a compound annual growth rate of 4% to 5% over the next four-five years, said the CareEdge Ratings report, adding just 50,000 rooms to the country’s current inventory of approximately 160,000 branded rooms

Discl: Invested

Fino payments Bank – Can the unique business model spring a surprise? (27-07-2024)

Does anybody know anything about the qualifications of the board members? especially the independent ones.

Microcap momentum portfolio (27-07-2024)

Hi @visuarchie Sir,

Can you confirm the back date for 6 months as the 26th of January was a holiday.

Are you considering Thursday or Monday?

Jupiter Wagons Ltd (previously CEBBCO) (27-07-2024)

- Overall Performance:

- Impressive revenue growth of 19% year-on-year (YoY) and robust EBIDTA growth of 32% YoY.

- Profit after tax (PAT) growth at 40%, with improved margins.

- Notable impact due to elections and peak summer conditions at multi-location facilities.

- Successful completion of a 6-month trial for the 11.2 kW system, securing an order from Siemens for the Vande Bharat train.

- EV Business:

- ARAI approval for commercial production of a 1.0-ton, four-wheel light electric vehicle with fast charging capabilities (full charge in 20 minutes). Certified range of 127 km.

- Production set for Q2 2025, with an initial batch of 500 vehicles (primarily B2B).

- High localization (80%) makes it eligible for subsidies.

- Promising demand potential in the 1 to 3-ton category.

- BIPL (Wheel Set Business):

- Remarkable 5X revenue growth reported.

- Plans to sell wheel sets to Indian Railways, Vande Bharat, and metros.

- Ambitious goal of establishing a 100,000-wheel set facility by 2027 for both exports and domestic consumption.

- QIP funds utilized for building a forged wheel and axle plant, enhancing backward integration.

- Jupiter (Brake Business):

- Leveraging partnerships, design capabilities, and backward integration.

- Sustainable margins attributed to wheels and braking systems.

- Strong order inflow expected, with ongoing work on Lithium-Ion batteries.

- Wheel Set Segment:

- Wheel sets need replacement every 7 years.

- Demand: 500,000 wheel sets per year (aftermarket) and 100,000 wheel sets per year from OEMs.

- Initial capacity of 100,000 sets per year by 2027, with potential for expansion.

- Forged wheels are the future due to high-speed requirements.

- Different pricing for freight vs. high-speed wheel sets.

- Anticipated revenue of 200 to 250 crore in FY 2024/2025 with Stone India.

- Forging facility expected to contribute significantly, achieving revenue of 4,000 to 5,000 crore with margins exceeding 15%.

- Container Business:

- Focusing on enhancing capacity for containers used in data centres and battery applications (not marine containers).

- Higher margins in data/battery containers.

- Collaborating with major players like TATA, Reliance, and Schneider.

- Global Total Addressable Market for container solutions estimated at 5.0 gigawatts, with potential growth to 10 gigawatts.

- Guidance:

- A strategic shift: By 2028, more than 50% of revenue will come from non-wagon businesses.

Conclusion:

1. There are multiple levers of growth.

2. Margins are increasing continuously with commentary of further increase.

3. Non Wagon revenue going to increase to 50% by 2028.

4. 7000 cr. of order book give visibility for approx 1.5 years.

5. Wheels business will give stability to revenue as it is replacement as well as OEM product.

6. Strong partnerships.

7. Valuation are high.

D: Invested