This might be due to inventory build up before festive season?

Posts tagged Value Pickr

Aaron Industries Ltd- The Elevator Play (09-11-2024)

Capacity expansion is still not live…

AARON_09112024120428_Update_09112024.pdf (601.0 KB)

CarTrade Tech – A Multi-Channel Auto Platform (09-11-2024)

Can someone explain what the total Addressable market size is for CarTrade and how much of that market share CarTrade currently holds?

Management think its 14 Bn $.

But it’s too much i need realistic number.

Patel Engineering – A bet on India’s Infra growth (09-11-2024)

Invested in this stock, my tracking.

Patel Engineering – https://pateleng.com/

Q3/23 Earning call highlights. (Feb 23)

- Mr Rupen Patel has not participated.

- Orderbook @ 16K

- Land parcels are being sold to reduce debt.

- Right issue, 1:2 at Rs 11 premium on 6/2/23, another at 7:5 at 8 Rs premium in 2019.

- JVs and others loss making assets are being trimmed to improve financial health.

- Too many questions on finance cost, Debt, right issue, Management commitments etc

Q4/24 Earning call highlights (May 24)

- QIP of 400 Cr raised at Rs 56.53.

- Order book 18,600 Cr as on march end 24.

- 130 Cr recd as arbitration with Govt. @ 300 Cr still pending, will be recd in next 3-4 years.

- FY 25 R guidance -10-15%/FY 26 R guidance 20-25%

- Next 3-4 years, debt to be reduced to @700-800 Cr, current debt 2600-2700 Cr. 5-6 year back it was 5500 Cr.

- 10% Equity participation in new Indian start up working in TBM servicing.

- Debt to EBITA ratio current 3-3.5, to be reduced to 2.25 by FY 26.

08/07/24 – Patel Engineering crashes 12% after CMD Rupen Patel death, pares YTD gains. Patel Engineering stock price hit a record high of Rs 740 on January 4, 2008, and an all-time low of Rs 0.69 on October 13, 1995. Patel Engineering stock hit a 52-week high of Rs 79 on February 6, 2024, and a 52-week low of Rs 34.95 on July 10, 2023.

Q1/25 Earning call audio recording

Patel Engineering Ltd Q1 FY2024-25 Earnings Conference Call

- Order book 17700 CR, @ 4 time annual revenue

- FY 24 revenue 4544 Cr, FY 25 10%, FY 26 20% increase, margin 14-15%

- Death of main promoter Mr Rupen Patel on 7/7/24.

- Concall assurance of the continuation of legacy in bid, competency and business.

- 50000 Cr tenders being quoted, success ratio @20-22%, Available opportunity 1.5L Cr.

- Hydro, irrigation and tunneling main focus area.

- Lesser orders received in Q1 due to election.

- Reduced interest burden due reduced debt on account of money received from arbitration and QIP. QIP issued at 56.53, 10.03% discount of last closing price (400 Cr.)

- Future growth expected from pumped hydro storage

- Expected order inflow of 10-12K Cr in FY 25.

- Average broker price target 75 by FY 25 end.

30 Aug 2024, 11:12AM

Patel Engineering Shares Gain @ 6.5% to 57.30 After Tie-Up With RVNL For Hydro, Infra Projects.

Sep 20 2024 | 1:33 PM IST

Patel Engineering stock gains: Shares of Patel Engineering rose sharply on September 20, 2024. The share surged up to 4.89 per cent to hit an intraday high of 60.39 per share.

The rise in Patel Engineering share price came after the company said that it has bagged an order worth Rs 240.02 crore from NHPC.

17/10/24 – Ircon International signs a memorandum of understanding (MoU) with Patel Engineering (+@4%. To 56.50) to collaborate on identifying, pursuing, and executing infrastructure projects in India and overseas.

30/10/24

Patel Engineering Limited has announced its decision to divest its remaining 9.99 per cent stake in Welspun Michigan Engineers Limited. This strategic move aligns with the company’s objective to optimize its investment portfolio and focus on core business activities. The sale is expected to be completed on November 7, 2024, and is anticipated to fetch a consideration of Rs 100 crore. Price reacted to +4% to 51.50

Q2/25 Result 13/11/24 and earning call highlights

Wednesday, 13th November 2024, at 05:00 PM IST

Share holding pattern and changes in last 4 quarters.

Summary Jun 2024 Apr 25, 2024 Mar 2024 Dec 2023

Promoter 36.1% 36.1% 39.4% 39.4%

Pledged 88.67% 88.67% 88.67% 88.67%

Locked 0.0% 0.0% 0.0% 0.0%

FII 3.7% 8.5% 3.4% 2.8%

DII 6.2% 7.1% 4.5% 5.6%

Public 49.6% 43.9% 47.9% 47.4%

Others 4.4% 4.4% 4.8% 4.8%

Big investor – Vijay Kedia – 1.42%, Anil vishanji dedhia 1.48%

Major event specific to Patel Engineering to be tracked.

- L1 to order conversion

- Tracking by – ICICI direct, Hem Securities, Anand Rathi.

FII/DII activity – and what we can make out of that! (09-11-2024)

“October Sell-Off: Why FIIs Are Pulling Out of Indian Markets”

Unpacking the Factors Driving FIIs Away from Indian Markets.

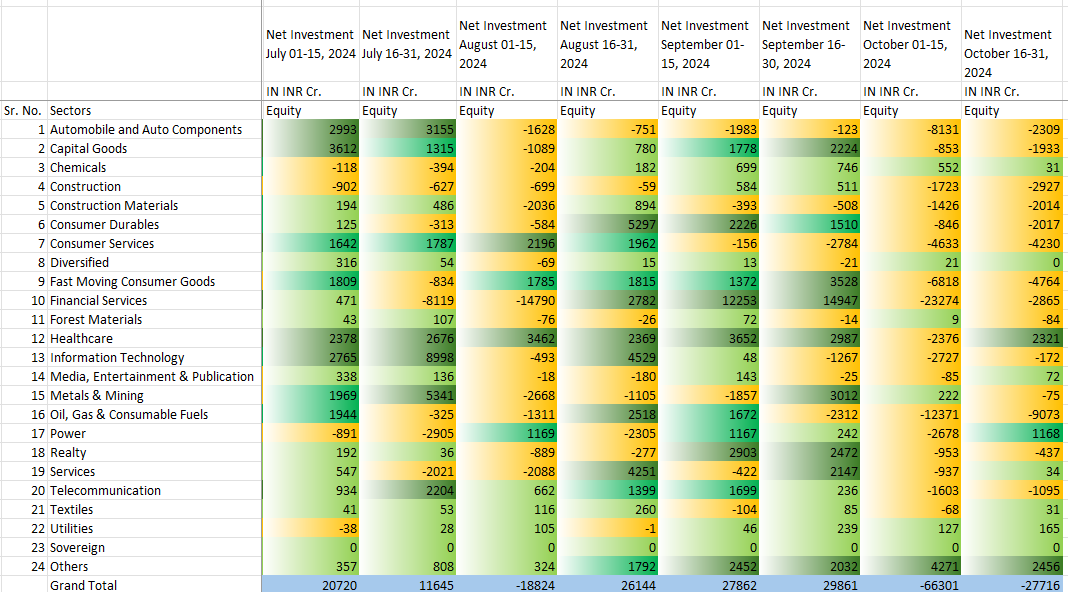

October month was a turbulent month for Indian equities, experiencing significant volatility and rampant outflows across several key sectors. The above data shows pronounced decline in foreign investor sentiments as nearly all sectors experienced heavy investment withdrawals, reflecting heightened market uncertainty.

The above data shows sector wise net investments of FII’s from the month of July to October. Out of 24 sectors, ~60% of the sectors experienced outflows. In the second quarter of FY25 ie. from July to September, Indian equities saw a total inflows of 97,408 cr. Rupees , while in the alone month of October we experienced a massive outflow of 94,017 cr. Rupees.

This outflows show a period of market anxiety and if this sharp downturn trend continuous it could point to challenging economic environment ahead.

The most hit sectors in this period are:

- Automobile and Auto Components :In the July month it gained a net investment of 6,148 Cr. and by the end of October it suffered a net outflow of 10,440 Cr. From a positive inflow to a major outflow indicating a significant investor retreat.

- Capital Goods :In July it secured investments worth 4,927 Cr. and by October it suffered outflows worth 2,786 Cr. The investment swing is a -153% change , showing increasing volatility.

- Chemicals :This sector was a good bet for the FPI’s as in the month of October it saw net inflows of 583 cr. as compared to net outflow of 512 cr. in the month of July.

- Financial Services :This the most uncertain sector amongst all as it is the backbone of any economy and is very difficult to analyse. in the four month period the FII’s have withdrawn a staggering amount of 18,515cr. Alone in the month of October, the financial service sector have contributed 27.8% or one fourth of the total outflows of the net investments for the particular month, suffering the net decrease of 26,139 cr.

- Healthcare :In the second half of October month only the healthcare sector experienced net inflow of >2000 cr. Overall this sector has gained a total of 17,469 cr. This shows that the FII’s are still bullish on this sector.

- Oil, Gas & Consumable Fuels :This sector saw a stark contrast between early inflows and severe outflows in October. From 1,944 cr. in early July to -12,371 cr. in early October has affected all the companies in this sector severely. The main reason behind this can be contributed to the ongoing war between Israel and Iran which directly impacts the prices of the crude oil.

The reasons for the selloff in the month are given below

- US Presidential Elections Stirring Uncertainty.

Global investors are keeping a close watch on the outcome, which could shake up economic policies worldwide. As the outcome was in favour of India not many economist believe it. - China’s Stimulus TemptationOne of the big reasons for the FII exit is China stepping up with some pretty tempting stimulus measures. China wants to get global investors back, and with these new incentives, FIIs see potential for higher returns there.

- Premium Valuation of Indian MarketsHere’s where valuations come into play. The Indian market isn’t exactly cheap. The long-term median price-to-earnings (PE) ratio of the Indian market, since 2007, has been around 21.9. But before this recent market correction, the Nifty50 PE was over 24. In simple terms, the market was slightly overvalued compared to other emerging economies. FIIs are like seasoned bargain hunters, and when they spot better value elsewhere, they don’t hesitate to shift. With more attractive valuations popping up in global markets, India lost some of its appeal.

- Disappointing Q2 FY25 Earningsthe September quarter earnings were a real letdown. Indian companies posted net profit growth of only 3.6% in Q2 FY25, the slowest in 17 quarters. This sluggish growth came from weak revenue numbers and rising interest and depreciation costs. Even though expenses and other income crept up only a little, the market didn’t take this news lightly. There was panic amongst the retails investors.

Conclusion

The overall idea from analyzing the data is that market investments between July and October 2024 experienced significant fluctuations across different sectors, reflecting broader market volatility and changing investor sentiments due to various macro economic factors.

While things might be a bit shaky in the short run, India’s economy is actually pretty solid underneath all the drama. Don’t panic out and sell everything just because things get a little wild Just do your homework, spread your money around different investments and focus on sectors that seem to provide opportunity in the long run. Stay cool, stay smart, and keep your eyes on the bigger picture!

HCC – Infra giant with massive turnaround story! (09-11-2024)

I have invested in HCC. My noting on company is here under.

HCC – https://www.hccindia.com/

Founded by industrialist Seth Walchand Hirachand in 1926.

Q1/24 earning call recording

Q4/24 earning call recording

- Order book 10475 Cr at the end of current quarter. Last year no order receipt.

- Right issue completed, 350 Cr raised.

- Debt reduced by money recd with client settlement, right issue and earning.

- Tehri – PSP for 2X250 MW completed, 2 remains. This year completion.

- Steiner AG – Switzerland – construction business sold to French company. Real estate remains with Steiner. Plan to make separate company and sell it.

- L1 – 4625 Cr, mainly from transport and hydro.

- Many arbitrages underway, some awards recd, few will be recd.

- Debt – FY 25 will by paying 425 Cr. Principle 200-220 Cr.

- Bidding can be done as net worth last year 600 Cr, current year 800 Cr.

- L1 to LOA @ 2 Months / 15-20% conversion. Normally L1 getting converted to LOA.

- Current year higher tax provision due to higher profit, brought forward losses will compensate.

- Next year FY 25 interest cost will be same that of FY 24.

- 3-4 years for order completion.

- Presently transport is higher contributor, future hydro and nuclear can be higher. Future order book will be much higher.

- 40K tenders open, @ 10K order can be expected in current year.

Q1/25 EARNING CALL AUDIO RECORDING

- Current order backlog is 9,534 crores – Q1/25

- L1 in 4,600 crores worth of orders.

- Tenders for 40,000 crores worth of strong project pipeline, conversion ration 15-20%. Almost 6-7K worth of projects being quoted on monthly basis.

- One of subsidiaries, Steiner AG – Switzerland being sold off, finding buyers. (loss contribution – 17 Cr). HCC may continue to be associated if new buyer wishes so.

- No guidance on revenue and margin in generally but will improve upon Quartey. FY revenue expected to be subdued, FY 26 revenue will be much more.

- Reduced interest cost due to debt repayment done in last two years. Debt: HCC has made significant strides in debt reduction, with consolidated debt, including accrued interest, declining sharply from ₹12,200 crore in FY15 to ₹3,500 crore by FY24 — a reduction of 71 percent. Standalone debt also decreased by 45 percent, from ₹6,200 crore in FY22 to ₹3,400 crore in FY24

- Normally Q2 revenue will remains subdued in relation to other Q due to monsoon.

- 65% order executed till date are from nuclear power plant.

- Green field hydro power takes 6-10 years, PSP 4 Years. Thus, existing dam with hydro plant will see more action.

- QIP planned for MF and large fund houses.

Earlier actions

- Right issues, 15/3/24 at Rs 20 premium in the ratio of 13 share for 118 holding.

- Right issues on 20/11/18 at Rs 9 premium in the ratio of 49 share for 100 holding.

05/09/24

Care rating upgrade from BB to BB+

04/10/24

Local swiss court extended Steiner AG’s provisional debt moratorium, by four months until February 07, 2025. The Court has authorized Steiner AG to conclude the asset transfer agreement for all real estate development projects including the transfer of assets from Steiner AG to Steiner Development AG, a wholly owned subsidiary of Steiner AG.

Price continue to be under pressure as compared to market, down to 40.33.

14/10/24

Price up by @10% to 44 in last two days.

HCC receives fresh order for construction of Cable Stayed Bridge across Agardanda Creek for Rs. 1031.6 Crore (excluding provisional sum & applicable GST) (HC original bid – 1187.76 Cr, Afcons Quote – 1249.42 Cr, MSRDC estimate – 809.89 Cr, Just east of Adani Ports & SEZ’s Dighi Port project)

Q2/25 Result – Earning call points – https://hccindia.com/uploads/reports/Analyst_meet_recording_Q2_FY25.mp3

- Operating Profit Margin %

Sep ’24 Jun ’24 Mar ’24 Dec ’23

17.78% 12.59% 15.02% 12.35% - 30 Projects spread well across India

- Order book @ 9800 Cr excluding 1032 Cr order received in October (standalone excluding subsidiaries)

- Consolidated revenue is Rs. 1,400 crores against Rs. 1,800 crores, low mainly due to sell of Steiner construction business.

- EBITA 18% v/s 14% (YoY)

- L1 in 3860 Cr, bids submitted 46000 Cr.

- QIP procedure started, will likely to be closed by December.

- HCC corporate debt guarantee to Prolific Resolution debt (3700 Cr) from Rs. 100% to 20%. Thus HCC’s corporate guarantee will be reduced to 740 Cr only now. This helps in fund raising efforts for new projects (QIP). Helps in accelerated order acquisition and future growth.

- HCC owns 49% of Prolific which holds Rs. 6,000 crore worth of claims and awards. These are interest bearing claims and awards.

- 307 Cr OCD settled at 234 Cr, will help in interest payment by 35 Cr annually. One of the means for accelerated debt reduction by utilizing money deposited in court against our arbitration. Current interest out go 350-370 Cr. Annually. 35 Cr reduction means @ 10% less interest payment.

- Steiner received orders Rs. 128 crore equivalent. Turnover Rs. 200 crore, PBT was Rs. 14.5 crore.

- Financial restructuring underway by various means, equity fund will support new order win and working capital will be by bank by better credit rating. After present QIP plan, if more order win come, further equity fund can be raised.

- Q3/Q4 revenue will be almost flat as order presently can generate Q1/Q2 revenue. Rising order win is target, order win transform in to revenue and P&L after @ 6 months time.

- Steiner AG Real Estate business divestment underway, will share as and when it conclude.

- PSP: Discussions with private power sector players. Formed with others strategic joint ventures. Looking at the sector engagement to bid @ Rs.12,000 -15,000 crores, coming 6 to 8 months.

- Year end debt 3600 Cr to 3000Cr.

- Subsidiary HCC Infrastructure – not interested in BOT, E&C is priority. Finance is critical while deciding road projects.

Changes in share holding pattern in last 4Q

Summary Jun 2024 Apr 13, 2024 Mar 2024 Dec 2023

Promoter 18.6% 18.6% 18.6% 18.6%

Pledged 76.85% 76.85% 85.32% 85.32%

Locked 0.0% 0.0% 0.0% 0.0%

FII 9.6% 9.3% 9.2% 7.8%

DII 6.6% 7.8% 8.2% 9.4%

Public 65.2% 64.4% 64.0% 64.1%

Chetan Jayantilal Shah – 1.28%

Important event specific to HCC to be tracked

- Steiner AG asset sell / transfer

- QIP

- L1 conversion to order.

- Tracking by any fund house – Ellara securities started tracking.

- Business concentration / political tilt: Maharashtra

The Anti-Portfolio (09-11-2024)

Bought websol from leftover cash of diwali trades, which would have otherwise been withdrawn to a bank FD, feeling bullish on waaree energies like bet.

Disc: unqualified to advise, hence please do your own research.

Vishnu prakash R Punglia LTD(VPRPL)-“Steering India’s Water Management Future” (09-11-2024)

VPRPL – Q2 FY25 result

YoY revenue – 334 cr Vs 296 cr ![]()

YoY PBT – 31 cr Vs 28 cr ![]()

YoY PAT – 23 cr Vs 21 cr ![]()

YoY EPS – 1.90 vs 2.05 ![]()

QoQ revenue – 334 cr Vs 256 cr ![]()

QoQ PBT – 31 cr Vs 19 cr ![]()

QoQ PAT – 23 cr Vs 14 cr ![]()

QoQ EPS – 1.90 vs 1.18 ![]()

Decent results ![]()

Disc: invested

Max Healthcare: A Growing Force in India’s Healthcare Sector (09-11-2024)

- Max Healthcare has a market capitalization of ₹3.5 trillion, a ninefold increase since Fiscal Year (FY) 2020. This increase is due to improved pricing, higher insurance penetration, and the focus on complicated treatments such as transplants.

- The Indian hospital industry was valued at $98.38 billion in 2023 and is expected to grow at a Compound Annual Growth Rate (CAGR) of 8% from 2024 to 2032. Public expenditure on healthcare in India was 1.9% of GDP in FY 2024.

- In the first quarter of fiscal year 2025 (Q1 FY25), Max Healthcare’s consolidated revenue increased by 20% year-over-year due to improved inpatient volume, bed expansion, improved Average Revenue Per Occupied Bed (ARPOB), and stable occupancy levels.

- Max Healthcare’s consolidated occupancy rate in FY 2024 averaged 74%, a decrease from 76% in FY 2023. This decline is due to the increased number of operational beds. In absolute terms, occupied bed days increased in FY 2024 by 7% compared to FY 2023.

- Max Healthcare’s ARPOB in FY 2024 was ₹75,800, an increase from ₹67,400 in FY 2023. This is due to price revisions, increased traction from international medical tourism, and a greater share of oncology, high-end, and robotic surgeries.

- Max Healthcare’s Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) per bed in Q2 FY 2025 was ₹74.5 lakhs, a decrease from ₹75.0 lakhs in Q2 FY 2024 and an increase from ₹70.9 lakhs in Q1 FY 2025.

- Max Healthcare’s network revenue grew by 16% in FY 2024 and by approximately 19% in Q1 FY 2025. This growth was driven by higher inpatient volumes and a shift in specialty mix towards higher-value specialties. Max Healthcare’s consolidated revenue in FY 2024 was ₹5,437 crore, a 19.17% increase compared to ₹4,562.60 crore in FY 2023.

- The operating margin for Max Healthcare’s network was 26.87% in FY 2024, while the consolidated operating margin was 28.23%.

Please note that this information may not reflect Max Healthcare’s complete financial picture. I recommend conducting thorough research and consulting financial experts for a more comprehensive valuation assessment.

Signature Global – Biggest Real Estate Company in NCR for Mid income and Afforable housing (09-11-2024)

Thanks for posting and I feel they are executing very well . Here is my q1 25 notes – generated with the help of AI.

Signature Global (India) Limited Q1 FY25 Earnings Call Briefing Doc

Date: 08 August 2024

Attendees:

• Management: Mr. Pradeep Kumar Aggarwal (Chairman and Whole-Time Director), Mr. Lalit Kumar Aggarwal (Vice Chairman and Whole-Time Director), Mr. Ravi Aggarwal (Managing Director), Mr. Devender Aggarwal (Joint Managing Director and Whole-Time Director), Mr. Rajat Kathuria (Chief Executive Officer), Mr. Manish Garg (Deputy Chief Financial Officer), Mr. Gaurav Malik (Chief Financial Officer), Ms. Preetika Singh (Head of Investor Relations)

• Moderator: Mr. Adhidev Chattopadhyay – ICICI Securities

• Analysts: Ayushi (Individual Analyst), Pritesh Sheth (Motilal Oswal), Deepak Poddar (Sapphire Capital), Prem Khurana (Anand Rathi Shares and Stock Brokers)

Main Themes and Highlights:

• Strong Q1 FY25 Performance: Signature Global reported robust operational and financial performance in Q1 FY25, driven by strong sales momentum and positive market trends in the Delhi NCR region, particularly Gurugram.

• Sales and Growth: Pre-sales reached INR 31.2 billion in Q1 FY25, a 255% year-on-year increase, exceeding 31% of the FY25 pre-sale target of INR 100 billion. The company is confident in achieving this ambitious target, supported by a strong distribution network, strategic launches, and favourable market conditions.

• Realization and Collections: Average sales realization increased significantly to INR 15,369 per square foot in Q1 FY25. Collections stood at INR 12.1 billion, surpassing expectations.

• Financial Health: Net debt reduced by 16% to INR 9.8 billion at the end of Q1 FY25. The company maintains a healthy financial position and is focused on generating operating surplus for debt reduction and strategic land acquisition.

• Project Development and Execution: The company has a robust project pipeline with 51 million square feet of portfolio, including 16 million square feet at advanced stages of completion. Signature Global is committed to timely project execution and plans to complete projects worth INR 38 billion in FY25.

• Focus on Key Micro Markets: Signature Global is strategically focused on key micro-markets within Gurugram, including Sector 71, Sector 37D, and Sohna. The company plans to launch a large project in Sohna, targeting the mid-income segment, and will continue its strategy of sustained supply in these areas.

• Strategic Partnerships: Signature Global is partnering with Grade-A general contractors for its premium segment projects, leveraging their expertise for high-quality construction while maintaining in-house capabilities for other segments.

• EBITDA Margin: The company anticipates an embedded EBITDA margin of 35% on current sales, reflecting a higher average realization compared to previous projects. For projects at advanced stages of completion, the EBITDA margin is expected to be between 20% and 25%.

Key Quotes:

• On Market Dynamics: “The residential real estate market in Delhi NCR, particularly in Gurugram, continued to display impressive growth in the first quarter of the current financial year.” – Mr. Pradeep Kumar Agarwal

• On Sales Performance: “We have achieved pre-sale amounting to INR31.2 billion in Q1 FY ’25, reflecting a year-on-year increase of 255%.” – Mr. Pradeep Kumar Agarwal

• On Growth Strategy: “Our strategy focuses on offering the right price, right size and right location real estate products in each segment.” – Mr. Pradeep Kumar Agarwal

• On Strong Operating Cashflow: “Our operating cash flows were good. We collected about INR1200 crores during this quarter. More interestingly, we created a surplus of about INR530 crores.” – Mr. Rajat Kathuria

• On Business Development: “Since the company has good levels of yet to be launched projects, which is almost like 30-odd million square foot of land inventory still exists with us, we only intend to do land acquisition going forward on a replenishment basis.” – Mr. Rajat Kathuria

• On Project Execution: “These are projects which are under affordable housing or under the mid-income housing scheme or the few projects which are plotting developments which are being done by the company. There’s a lot of focus going on in completing these projects. Our more than 500 member construction team is fully focused to deliver these projects within the committed timelines.” – Mr. Rajat Kathuria

• On Micro-Market Strategy: “As far as the Gurgaon strategy is concerned, we will stay put on these three locations. We may do something opportunistically but we don’t need to add something very significant, we don’t need, we are not missing out on any very specific significant location per se.” – Mr. Rajat Kathuria

• On Partnership with General Contractors: “We do intend to bring in good quality grade-A general contractors. These are not makeshift guys. These would be the best-in-class sort of general contractors, with whom one can work in the country right now.” – Mr. Rajat Kathuria

Overall, Signature Global delivered a strong Q1 FY25 performance and remains optimistic about its future prospects. The company’s strategic focus on key markets, strong execution capabilities, and healthy financial position are expected to drive continued growth in the coming quarters.