More competition

More competition

SRF posted results yesterday and hosted a conf call today. It seems worst is over for the firm with packaging and textiles showing good growth over CQPY1. Chemicals is beginning to show turnaround and will catch more in Q2 and a lot more in H2 2025 per mgmt…

Overall, mgmt. seems reasonably confident of achieving 20% growth in FY25 over FY24.

Please share your thoughts on this. is it a hold, buy more or exit per your views?

The OPM is going through the roof since they have not been able to acquire content, due to intense competition. We need to evaluate what kind of margins they will have going forward. Once the content acquisition resumes, the yoy results might start moderaing as margins will go down as per my understanding.

Thank you!

Your thought process in valuing stocks is impressive. While comparing, I didn’t acknowlegde that Hatsun could have been overvalued.

Please do share your Twitter ID if you’re present on the platform.

generally this is done to replace debt with higher interest rate with new one with lower interest rate.

They maybe able to raise debt now at lower interest rate than what they raised before.

Dodla Dairy –

Q1 results and concall highlights –

Revenues – 911 vs 823 cr, up 10 pc ( revenues are at all time high ). Revenues from international business grew by a massive 38 pc to 83 cr

EBITDA – 105 vs 60 cr, up 60 pc ( margins @ 11.5 vs 7 pc )

PAT – 65 vs 35 cr, up 86 pc

Value Added products contribution to sales @ 35 vs 32 pc – a big jump

Avg milk procurement per day @ 17.6 lakh litres, up 11 pc YoY

Avg milk sales per day @ 11.3 lakh litres, up 2.5 pc YoY

Avg daily sale of curd @ 467 MT, up 6.3 pc

Sale of Value added products in Q1 @ 313 vs 258 cr, up 22 pc

Total Dodla parlours @ 598

Total chilling centers @ 152

Total milk processing capacity per day @ 20 lakh litres @ 14 processing plants

Total milk processing plants in Africa @ 02. Margins in Africa are higher due to limited competition

Sales from Animal feed @ 31 vs 18 cr YoY. EBITDA @ 4 vs 1.6 cr YoY

Company has taken minor price cuts in Q1 ( due falling milk procurement prices ) and may take some more price cuts in future too. However, they intend to maintain their Gross margins at Q1 levels

Gross margin expansion in Q1 led by – higher value added sales, higher export sales, soft procurement prices

Seeing similar procurement prices in Q2 as in Q1 ( basically seeing no inflation in procurement )

Africa sales LY were around 220 cr. Expecting to do around 350 cr this yr !!!

Animal feed business sales LY were 80 cr. Expecting to do around 160 cr this yr !!!

Confident of maintaining 10-12 pc kind of topline growth with 11-12 pc kind of EBITDA margins for whole of FY 25. That would mean a full yr EBITDA of around 380 cr vs 290 cr YOY !!!

Most of company’s products do sell at a premium price vs competitors. That’s because of better quality and better positioning

Current avg procurement price is Rs 36 / lit and avg selling price is Rs 56 / lit – for India business

No major capex is lined up for current FY

International business margins are almost double that of India business margins

Margins in plain milk business are around 7-8 pc. Margins in VAP ( including curd ) are around 13-14 pc (EBITDA margins – ie)

Company expects the total share of value added products for FY 25 @ 33-34 pc of total sales

Disc: holding from lower levels, not SEBI registered, not a buy/sell recommendation

Dodla Dairy –

Q1 results and concall highlights –

Revenues – 911 vs 823 cr, up 10 pc ( revenues are at all time high ). Revenues from international business grew by a massive 38 pc to 83 cr

EBITDA – 105 vs 60 cr, up 60 pc ( margins @ 11.5 vs 7 pc )

PAT – 65 vs 35 cr, up 86 pc

Value Added products contribution to sales @ 35 vs 32 pc – a big jump

Avg milk procurement per day @ 17.6 lakh litres, up 11 pc YoY

Avg milk sales per day @ 11.3 lakh litres, up 2.5 pc YoY

Avg daily sale of curd @ 467 MT, up 6.3 pc

Sale of Value added products in Q1 @ 313 vs 258 cr, up 22 pc

Total Dodla parlours @ 598

Total chilling centers @ 152

Total milk processing capacity per day @ 20 lakh litres @ 14 processing plants

Total milk processing plants in Africa @ 02. Margins in Africa are higher due to limited competition

Sales from Animal feed @ 31 vs 18 cr YoY. EBITDA @ 4 vs 1.6 cr YoY

Company has taken minor price cuts in Q1 ( due falling milk procurement prices ) and may take some more price cuts in future too. However, they intend to maintain their Gross margins at Q1 levels

Gross margin expansion in Q1 led by – higher value added sales, higher export sales, soft procurement prices

Seeing similar procurement prices in Q2 as in Q1 ( basically seeing no inflation in procurement )

Africa sales LY were around 220 cr. Expecting to do around 350 cr this yr !!!

Animal feed business sales LY were 80 cr. Expecting to do around 160 cr this yr !!!

Confident of maintaining 10-12 pc kind of topline growth with 11-12 pc kind of EBITDA margins for whole of FY 25. That would mean a full yr EBITDA of around 380 cr vs 290 cr YOY !!!

Most of company’s products do sell at a premium price vs competitors. That’s because of better quality and better positioning

Current avg procurement price is Rs 36 / lit and avg selling price is Rs 56 / lit – for India business

No major capex is lined up for current FY

International business margins are almost double that of India business margins

Margins in plain milk business are around 7-8 pc. Margins in VAP ( including curd ) are around 13-14 pc (EBITDA margins – ie)

Company expects the total share of value added products for FY 25 @ 33-34 pc of total sales

Disc: holding from lower levels, not SEBI registered, not a buy/sell recommendation

@Anant buys 130000 shares of RS today. Would be interesting to hear his views on this business.

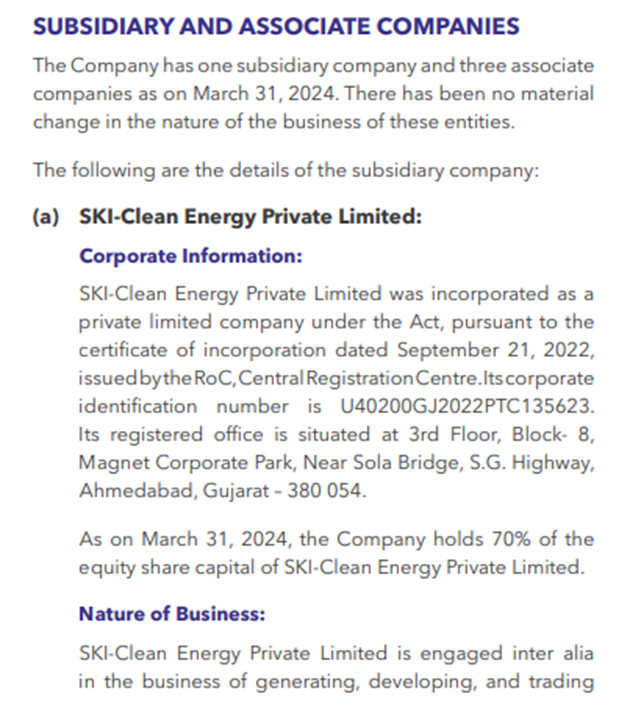

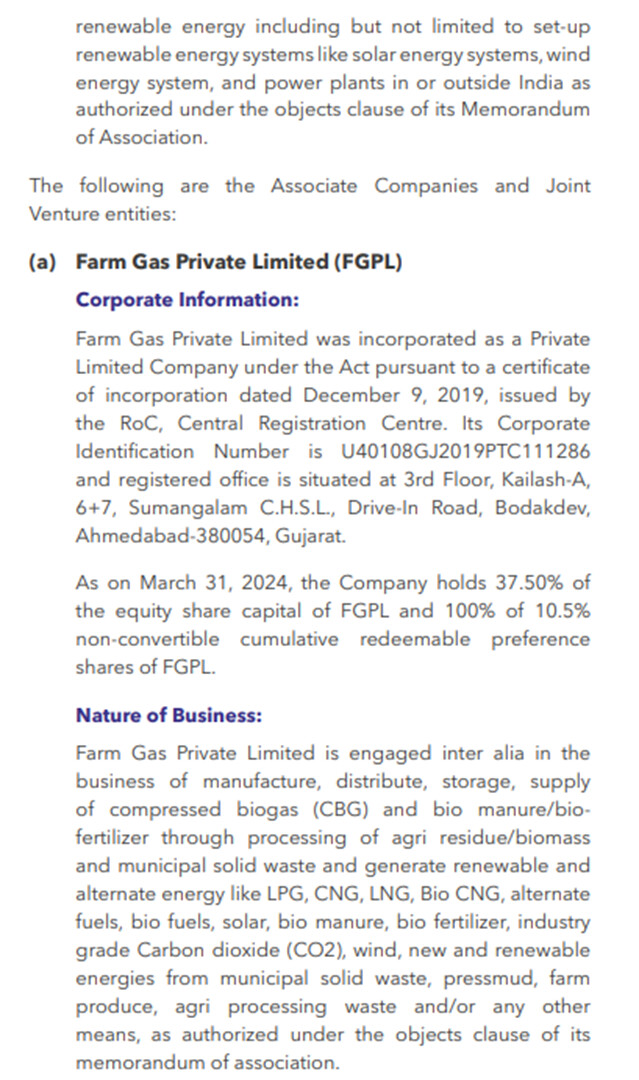

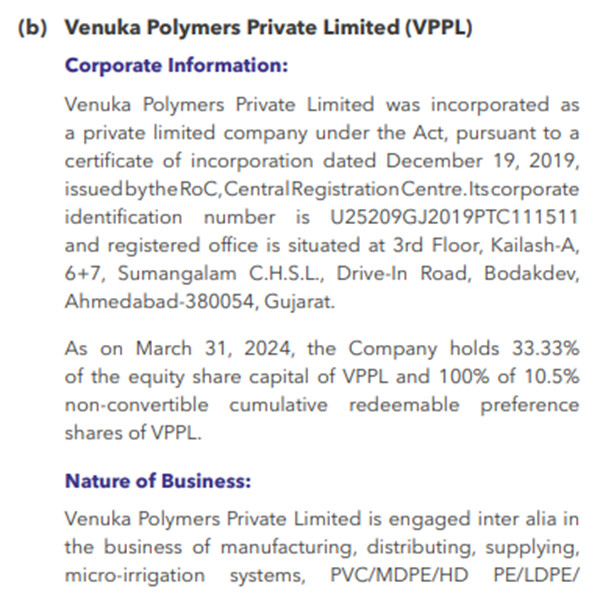

Is there any way to ascribe a value to the subsidiary and the JVs.

Subsidiary’s AR is present on IRM’s website but it wasn’t generating any revenue from operations till end of FY23:

Hi Prabhat, iam holding marksans since few years, and I can surely say company will cross 3500CR revenue by FY26 and even more because management has always been conservative in giving targets.