Thank you sir, for the detailed answer. I’m planning to have 20 stocks PF from NSE 500 universe and WRH to be 1.5X (Wait until rank 30) and to start the rebalancing once in a week and change it to fortnight if churn rate is very less. thanks again for taking time to explain in detail. much appreciated.

Posts tagged Value Pickr

Margin Of Safety (Stocks & Index) stocktrend.net (22-07-2024)

I have been studying about Intrinsic value and margin of safety from intelligent Investor and I have been building stocktrend margin of safety calculator some kind of screening formula to calculate margin of safety. I have been using Benjamin Graham Intrinsic value formula to calculate Margin of safety. so basically I am tech guy and learning stock market since 2019 and also its my first active thread, so bear with me if any miscalculation or incorrect thesis.

Intrinsic value = [EPS × (8.5 + 2g) × 4.4]/Y

From:https://www.valueresearchonline.com/stories/27759/the-ben-graham-way/

I had changed some of the parameter to include future earning and for Indian market.

Intrinsic Value = (EPS * (AverageNiftyPE + 2 * growthRate)* Gsec)/Bond Yield

So, For 8.5 base PE, I had taken Average PE for Indian market and For 4.4, I had taken gsec rate as risk free rate and bond yield as same above AAA corporate yield.

For simple screening, we can formulate a formula to know MOS over future earning potential whether its worth to know more or study about the company. So by applying the above for Nifty.

As on (21/07/2024) For Base PE, I had taken Average Nifty median PE which is 20.74 (20 year average) and if we consider 0% earning growth and EPS as 1,052.4 Rs. Bond Rate(Risk Free Rate) as 7.01(Government Sec) and Bond Yield as 8.32% (AAA Corporate Yield)

This gives Intrinsic value of Nifty as 18390.11 and margin of safety as -33.39% which is overvalued by 32.09% at 0% growth rate but if we assume 10% eps growth for the next 5-7 years its undervalued by 32%

If My understanding is correct, so assuming 10% eps for the next 5 years, nifty is undervalued by 32%. Which gives better view of valuation over future earnings or am I missing something ?

By applying Same principle in Each sector by giving expected earning growth Rate for each industry and average median PE as industry PE. we can formulate at screening margin of safety for each sector.

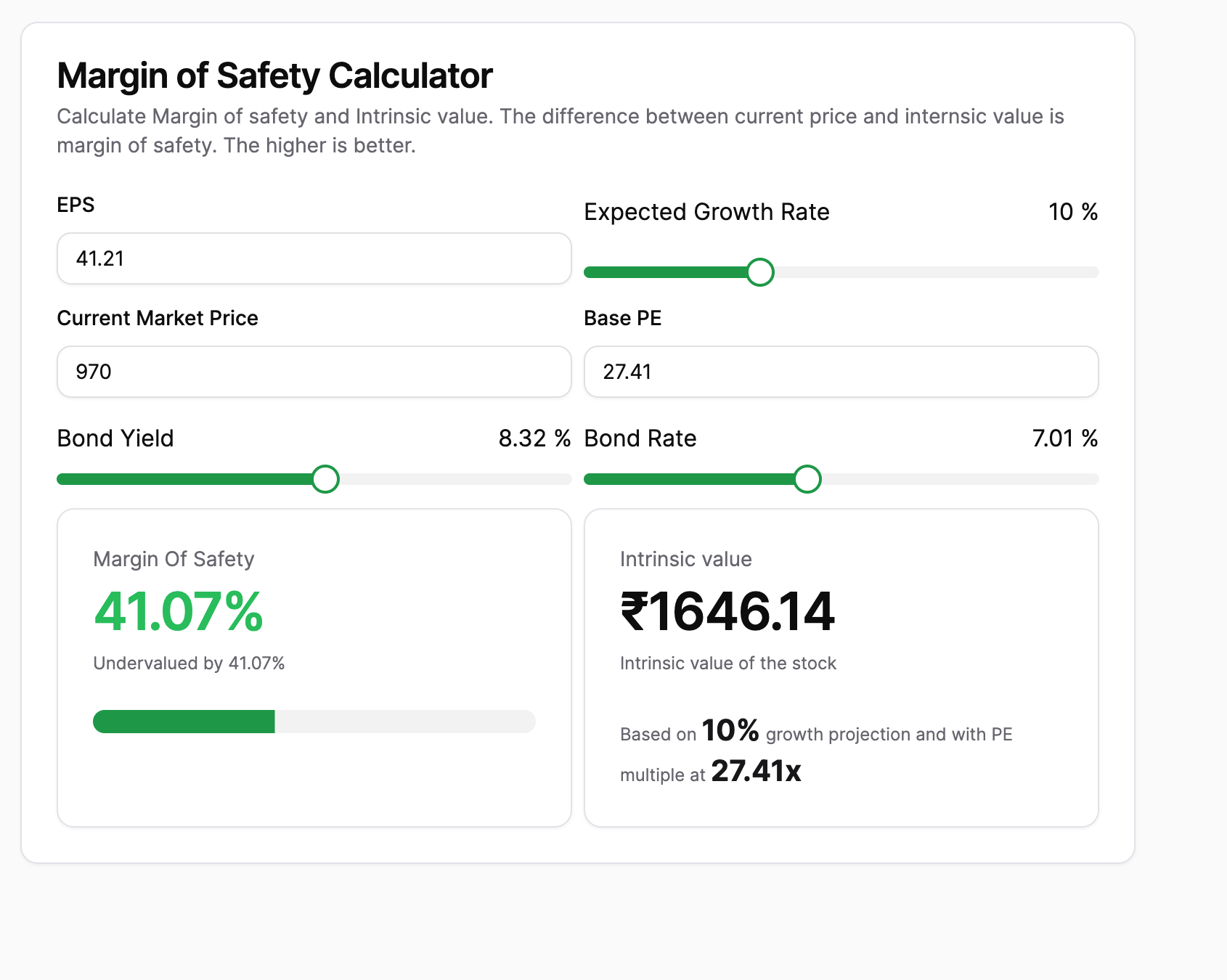

Eg: Tanla Platforms Limited

As on (21/07/2024) I had taken Average Nifty IT Index median PE which is 27.46 (5Y avg) because of IT company and if we consider 10% earning growth and EPS as 10.50 Rs. which gives 41.07% margin of safety.

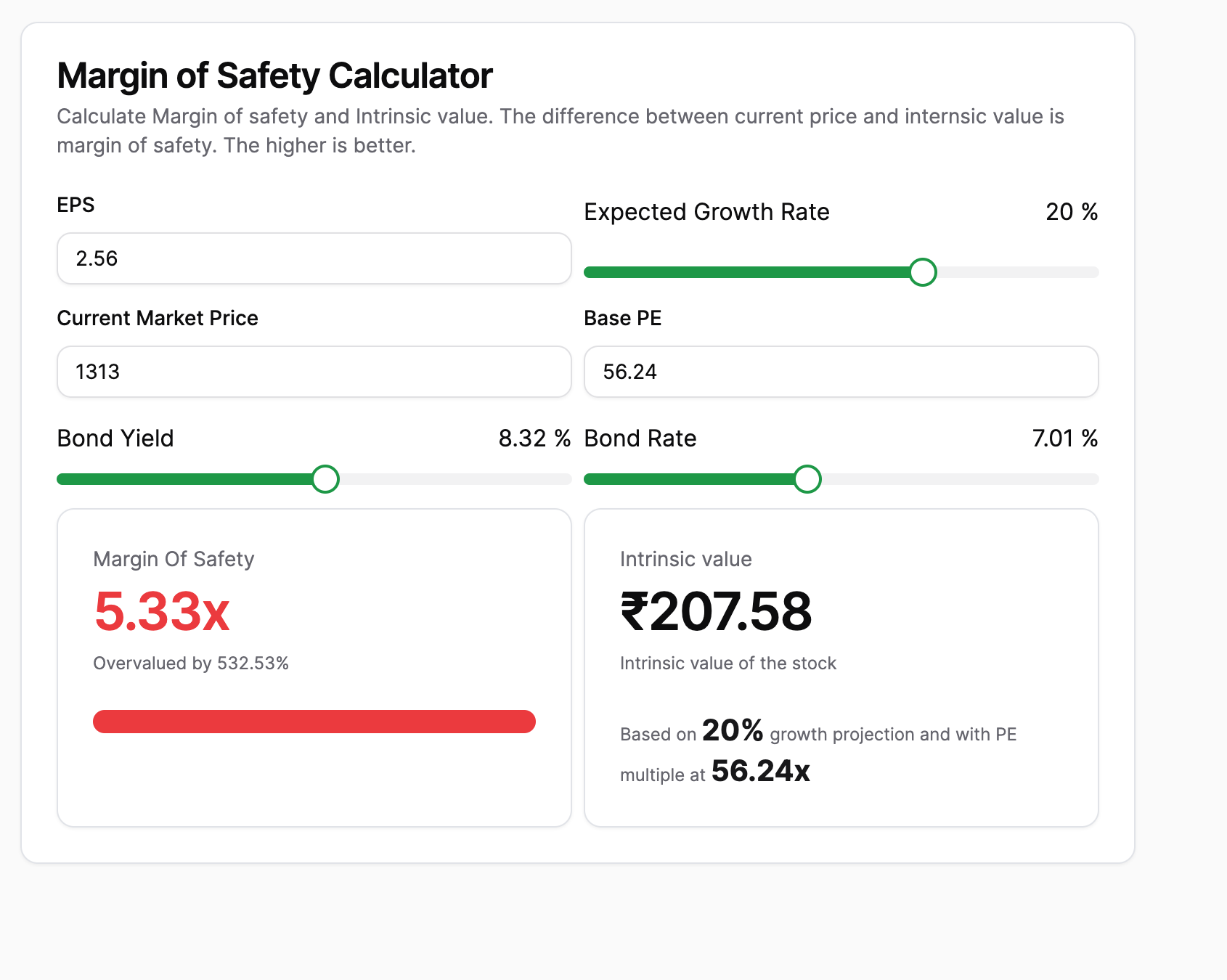

Like wise, Lets take hot sector, defence

Paras Defence

Here we don’t have longterm index data, I would have taken nifty PE but lets us use defense index PE as 56.24 and if we consider 25% earning growth and EPS as 2.56 Rs. which gives -532% margin of safety. which is overvalued by 532% or 5x its future earnings. If we consider Nifty PE as base PE it would be 8 times.

And Also, I had taken the same in google sheet and computed MOS % for each stock.

Stocktrend(Margin of Safety Calculator):StockTrend – Trusted Source for Market Trends and Insights

Twitter Thread (Stock Watchlist):x.com

Note:The above mentioned stocks are for examples only and Not a Buy/Sell recommendation. I may be wrong as well. Feel free to share your views and analysis of any stocks. Very much interested to discuss further.

E2E Networks Ltd – Listed small Cloud computing player (22-07-2024)

True. I’ve complained on this forum of vague number provided in concalls before. I hope Dua learns that number uttered, even in the most hypothetical scenarios, will be quoted back.

800cr. did seem like surreal and actually got my heart racing due to the below calculation:

If we look at it from an annual asset turn perspective where capex this year, gives revenue next year, these are the numbers we get:

Assets: 800 (this year) + ~200 (existing 210 - 12 intangible assets ) = ~1000 cr. This will be in FY24-25

Revenue in 25-26 from above at 1.5x asset turn = 1000 X 1.5 = 1500 cr.

Assume, PAT margin is 15% (24% now - 9% debt interest assumed) = 1500 * 0.15 = 225 cr.

EPS = 225 /1.45 = 155 Rs/ share

PE (in todays price) = 1818 (CMP) / 155 = ~11.7

Now these are quite conservative assumptions. It does not assume capex will give returns within the same year. PAT is assumed low. No new CAPEX and returns in FY25-26.

I have not accounted for mounting depreciation but the point is that the dream of these numbers go my heart rate up and that does not happen often.

With the 800cr. assumption gone, let’s see where this goes. Will have better idea in H2.

E2E Networks Ltd – Listed small Cloud computing player (22-07-2024)

(post deleted by author)

E2E Networks Ltd – Listed small Cloud computing player (22-07-2024)

Agree. However, now that they have said that the Rs 800 cr capex guidance was a misunderstanding, we have to go back and rework the FY 25E numbers.

Motherson Sumi Wiring India Ltd (MSWIL) – Wired for growth (22-07-2024)

As mentioned, none of the peers are listed so does this company have some sort of moat? Would be interested to know if you are still tracking this company.

Samhi Hotels – Turnaround with Tailwinds (22-07-2024)

Last lot bought at 171 today, fully loaded up with 20% allocation, as Warren bufffet said, stock will find its own value and this investment is a no brainer for me. Heads i win and tail i dont loose much. Fingers crossed.

They own all real state, only value of real state will go up by at least 50% in 3-4 years seeing the markets land is situated.

Not writing any number based calculations as it doesn’t work in current market conditions where penny stocks trade at P/S of 10 and PE 100,![]()

![]()

![]()

Angel One: Metamorphosis into a Fintech? (Previously Angel Broking) (22-07-2024)

Definitely an attractive opportunity. However, keeping an eye on the chart pattern.

The last 7-8 months, the stock has been making lower tops and bottoms. Unless it goes to 13-14 PE, I personally will not buy it. However, I will be ready with the cash. Very high-quality company, transitioning to a stable AMC business.

However, you can buy if a further 10-15% drop does not bother you. Because I feel long-term (>3-5 years) will be good.

Stance: Quite biased. This is the highest allocation in my portfolio. Looking to invest more, if the trend reverses or stock becomes extremely cheap. Currently, 10% lower compared by average buying price