As mentioned in concall, company is looking for acquisition in RoW as India is expensive. IF it does not materialize for long time, buy back may be considered.

D: Invested

As mentioned in concall, company is looking for acquisition in RoW as India is expensive. IF it does not materialize for long time, buy back may be considered.

D: Invested

Three points is important and track properly as per my understanding

Three points –

ola maps is using open streetmaps vs developing their own maps solution. I dont think it will be scalable or will have adoption

Google maps pricing might have a v minor affect as google maps cant be used for commercial purpose

Selling stake of around 1% doesnt meaning anything is fishy. Promoters stake is > 51%. And 1% was sold for philanthropy.

Hey Kalyan, just check the bulk deal data. Once you know their names, you’ll know where they turn up.

Indeed, these are high quality subsidaries that should grow at a PAT >15%. Currently, these contribute to about 5000Cr of the 68000 Cr PAT of HDFC (about 8%).

For sure, you cant buy earnings of this quality at a PE of 20 in the open market which is what HDFC sells for now.

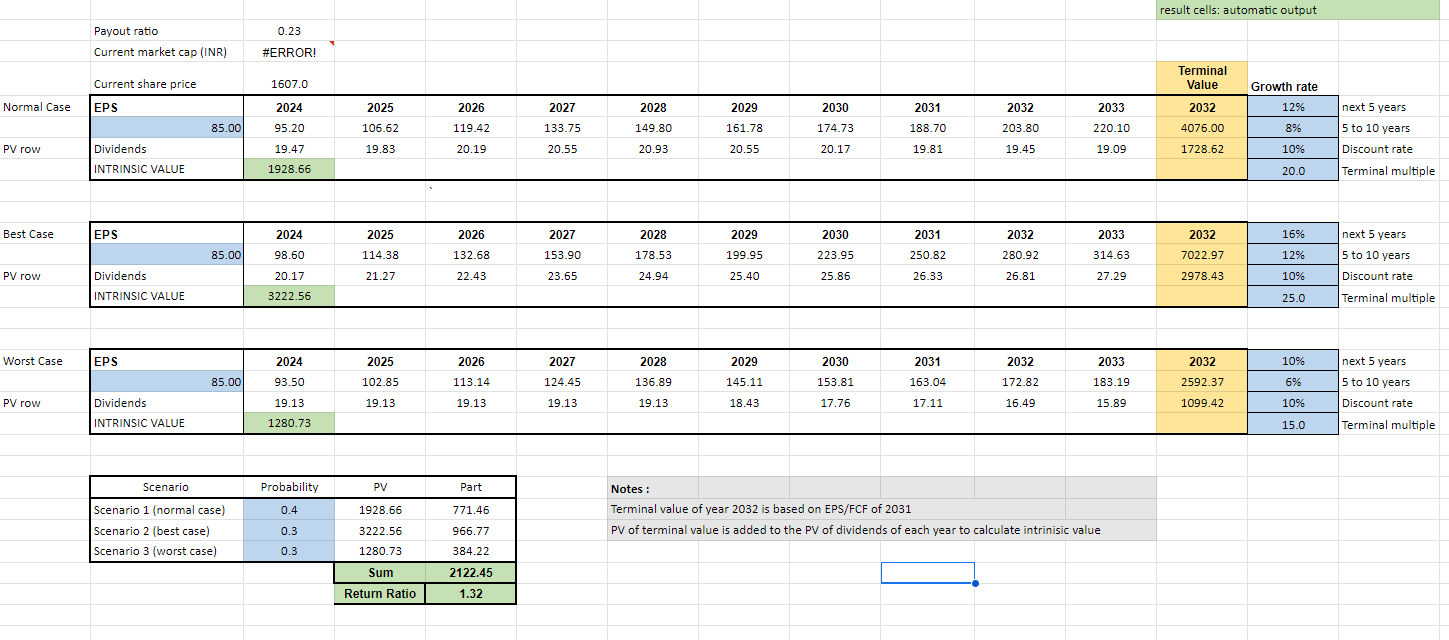

A light weight valuation of HDFC below. One should certainly make more than 10% going forward. Can be closer to 15% I think.

The decrease of 9.42% in promoter holding during the Q4 FY 2023-24 was mainly due to QIP of Rs.500 crore for the stated reasons and seems it was well accepted by the stakeholders. The reasons for reduction of promoter’s holding in Q1 of FY 2024-25 are yet not disclosed/know, let hope some concrete reasons come out.

The reasons for decrease in shareholding by FII and DII are best known to themselves as they keep coming and going. However, the number of retail shareholders are increasing, can be an indicator.

My Apologies, it looks a diversified small case,![]()

![]() . What matters when you pick a stock is capital allocation thats what i have learnt in markets. Your 50% allocation should be in top three bets if you want to create a meaningful PF size. I hold 12 stocks with top 3 are close to 50%.

. What matters when you pick a stock is capital allocation thats what i have learnt in markets. Your 50% allocation should be in top three bets if you want to create a meaningful PF size. I hold 12 stocks with top 3 are close to 50%.

Example, Kalyan Jewel turn 5X in last year, weightage has increased to 25% from 10% just by holding.

Just be careful of that analogy. 7 years is long time. Even with high caliber promoters company can under perform. Shilpa med is a prime example. It got it’s act right just now

Again good set of numbers by RPG

I hope you find it useful

Nice thread since 2015

I took a fresh entry last week before the run up.

While going through the past discussions in this forum, I have noticed the frequent management changes, and quality problems with certain products.

Anyone else knows if the issue stills persists with the company, as whoever the management, no business is investable if the products are not reliables

Strong cash basis, no debt, and strongest reserves, and ideal Accounting profit to OCF are my conviction points.