Good compilation of 100+ ideas

https://x.com/EquityInsightss/status/1812341460773355980?t=QX65K7j6C4wA2Luys56FCQ&s=08

Good compilation of 100+ ideas

https://x.com/EquityInsightss/status/1812341460773355980?t=QX65K7j6C4wA2Luys56FCQ&s=08

Company has reduced it’s guidance for FY25 to 26-35% from 40-45% due to headwinds in the sector.I expect H1 to be flat and growth can only come in H2.

Some of the good setups , we are looking at wrt technical prespective:

No buy/sell recommendation.

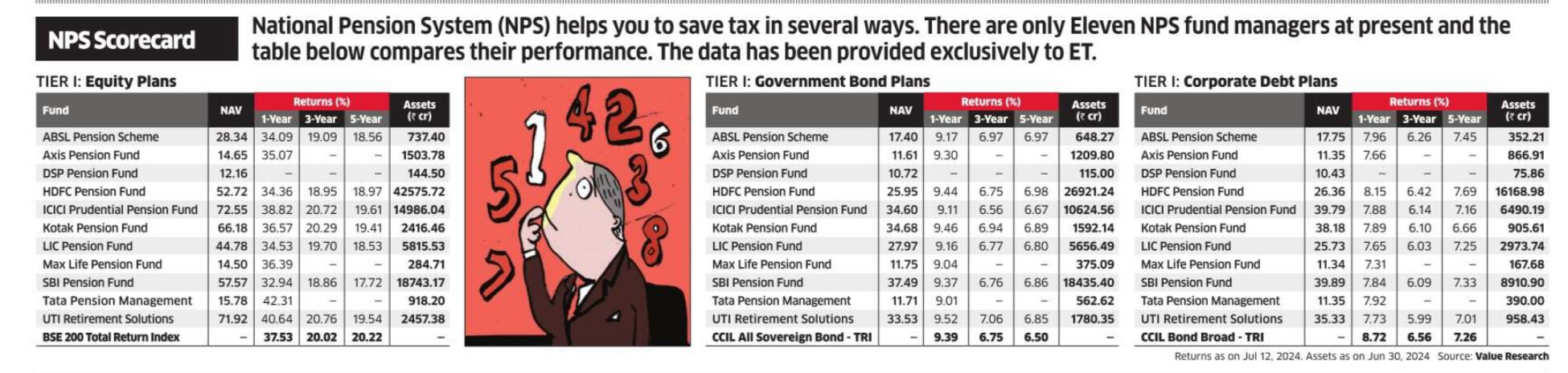

While the National Pension System(NPS) has gained a lot of traction over the past few years, it is important to track the asset managers and switch funds to the best performing ones.

Here’s a comparison of fund performance across Equity, Govt. and Corporate Debt:

Moreover, with 7-8 parks in India – won’t the competition increase thus the growth would be a lot tougher, therefore, my suggestion is to reduce it further by Park 8

Hi @GautamBafna

It looks like this quarter was affected by a lot of one-time cost i.e. Retrenchment, Consultancy project and inventory issue. Do you see a turnaround in the coming quarter just on the basis of these issues being getting resolved in the future?

What are your thoughts?

Is margin really a confidential info?!! What they have achieved by hiding it? Has market share improved? Has margin improved?

In last 10 years market cap of ambika is hardly doubled, in other hand nitin spinners is more than 10X in same time period even after disclosing that “confidential info”, that fabric margin is 1-2% more than yarn margin.

With rave reviews on “Kalki”, it is surprising not to find any reflection on Phantom, or we will see late reaction on Monday?

These are Semiconductor products. Sansera doesn’t have any offering in terms of expertise (tbh there would be handful companies who can offer any kind of expertise in our country). As long as management of Sansera understands that they don’t have the knowledge to take technical decisions and leave the running to the professionals, it is best thing.

Setup of manufacturing of semiconductor chips is close to impossible for Sansera. It can setup specialized manufacturing of COTS solutions for RF & mmWave products which would be at a much higher level of expertise compared to what let’s say Dixon is manufacturing. Even if it outsources the manufacturing, the majority of the value add would remain with MMRFIC as the IP carries value here. MMRFIC’s products are of MIL standards and not commodity products.

Semiconductor and PCB based, COTS solutions.

Can you please implement number of outstanding shares in income statement please.