I am searching the answer for this question. But unfortunately till now not able to find a satisfactory answer. Can the experts answer this doubt please.

Thanks in advance

!

I am searching the answer for this question. But unfortunately till now not able to find a satisfactory answer. Can the experts answer this doubt please.

Thanks in advance

!

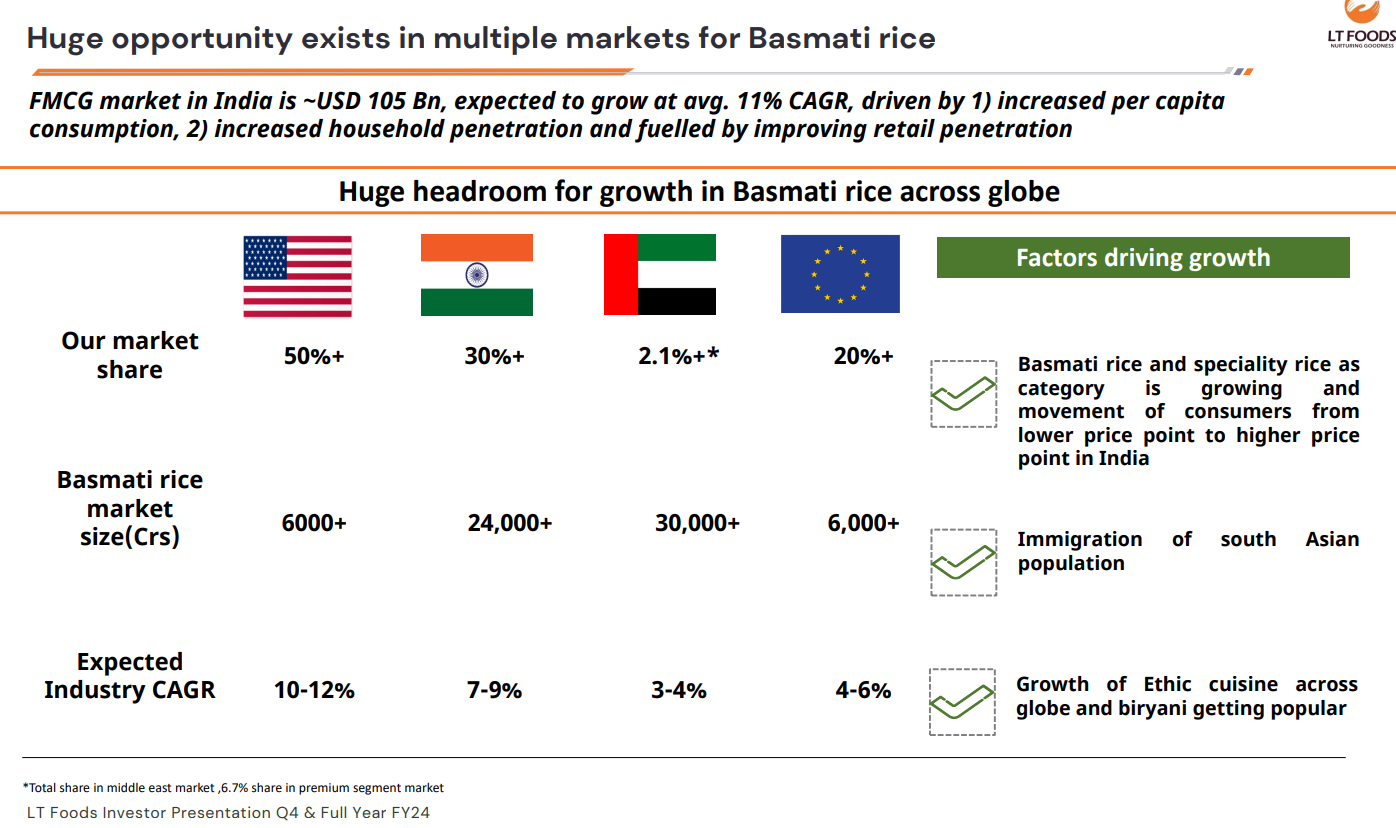

Saudi Market alone is 10K cr market

Lt foods have negligible present in middle east which is biggest market ,

Just see opportunity and look at domestic there is massive shift from unorganized to organized

Lots of hypermarkets are expanding , Quick commerce also , matter of time these chains will penetrate in rural and tier 2 tier 3 cities, growth coming from these will be massive

How it’s different from Shankara. It also has some stake of apl Apollo

Hi,

I had a few questions wrt related party transactions for a company’s RHP I was going through.

I exited my position some time back. Tracked it till 2022 end. I don’t think demerging would ever be good or is an option. Outlined it in my original thesis. Part of my thesis continues to hold. I exited because I just didn’t understand some of the developments. Haven’t tracked the company since. No views on the company as of now.

SGMART is a B2B one-stop shop that provides a wide range of construction-related solutions from top brands under one roof. The company aims to establish itself as the trusted and preferred platform for all infrastructural and building material needs in India.

History:

The company used to be Kintech Renewables. The company was earlier engaged in activities relating to the renewable energy sector. The promoters then were Aditya Singhal, Saurav Singhal, Ambala Patel and Jigar Shah.

In April-23, New promoters Meenakshi Gupta and Dhruv Gupta bought out the company for INR 22 crs. The promoters belong to the APL Apollo group family.

Products:

TMT Bar, MESH NET, Binding Wire, Welding Rod, Steel Tube, Sanitaryware, Bath fittings, Laminates, Galvanised Sheet, HR Coil & Sheet, All Ceramic Range of Tiles, Premium Tiles Adhesive & Grouts, Double Charge Tiles division, Home appliances, Lighting for Domestic, Commercial & Industrial applications, LED Lighting, Fans, Modular Switches & Wiring Accessories, Water Heaters, Industrial & Domestic Circuit Protection Switchgear, and Industrial & Domestic Cables and Wires. Looking ahead, the company plans to expand its product line, adding Barbed Wire, MS Bar, Angle, ISMC Channel, ISMB Beam, and Patti Flat.

Brands being sold:

4 large brands- APL Apollo TMT bars, Kajaria Tiles, Havells electricals, SG premium

Other Brand partners- NMDC, JSW Steel, Jindal Steel and Power, Hindustan Zinc, Godawari Power and ISPAT, Triveni Enterprises, etc.

Industry dynamics:

Industry issues:

Industry size:

| Segment Product | Market Size, FY24 | FY2027E | |

|---|---|---|---|

| Downstream Steel | 4.1 Trillion | 5.6 Trillion | |

| Fixtures & Fittings (Bath fittings, Electrical fittings) | 1.3 Trillion | 1.8 Trillion | |

| Tiles industry | 0.4 Trillion | 0.6 Trillion | |

| Total | 5.8 | 8 |

Other Investors and fund raising:

In Nov-23, The company raised equity shares worth 878 crs, at Rs 5000 per share, Rs. 10 face value. The top allotees from this were:

| Allottees | No of equity shares | Value (in crs) |

|---|---|---|

| Kitara PIIN 1103 | 202,000 | 101 |

| Plutus Wealth Management LLP | 200,000 | 100 |

| QRG investments and Holdings Ltd | 100,000 | 50 |

| Blue Foundry Advisors LLP | 100,000 | 50 |

| Vallabh Bhanshali | 50,000 | 25 |

| SageOne-Multiple | 50,000 | 25 |

| Turnaround opportunities fund | 40,000 | 20 |

| Abbakus | 80,000 | 40 |

| Rikeen P Dalal | 30,000 | 15 |

| 360 One special Opp Fund | 30,000 | 15 |

| Mukul Mahavir Agarwal | 30,000 | 15 |

| Ashok Goel Trust | 24,000 | 12 |

| High Conviction Fund | 20,000 | 10 |

| Madhuri Madhusudhan kela | 20,000 | 10 |

| Top allottes | 976000 | 488 |

The company also issued warrants at the time, at Rs 5000 per share to non-promoter category:

| Particulars | No of shares | Value (in crs) |

|---|---|---|

| Rohan Gupta | 382,000 | 191 |

| Marigold Partners | 90,000 | 45 |

| Shivkumar Bansal | 75,000 | 37.5 |

| Rohit Gupta | 50,000 | 25 |

| Deepak Kumar | 25,000 | 12.5 |

| Anubhav Gupta | 25,000 | 12.5 |

| Kanhaiya Sharma | 10,000 | 5 |

| Anjana Bansal | 10,000 | 5 |

| Arun Agarwal | 10,000 | 5 |

| Payal Jain | 10,000 | 5 |

| Ravindra Kumar | 10,000 | 5 |

| Chakram Singh | 5,000 | 2.5 |

| Amit Kapoor | 5,000 | 2.5 |

| Bhanu Singh | 5,000 | 2.5 |

| Utkarsh Dwivedi | 5,000 | 2.5 |

| Ankit Jain | 3,000 | 1.5 |

| Atul Jain | 3,000 | 1.5 |

| Total | 723,000 | 361.5 |

In February 2024, the company split the stock 10:1, and issued bonus shares on the same.

Financials:

The new company started operations in June 2023, and since has had 4 quarters of operation.

| Particulars | Q1FY24 | Q2FY24 | Q3FY24 | Q4FY24 | FY24 |

|---|---|---|---|---|---|

| No. of customers | 170 | 315 | 426 | 444 | |

| Net Revenue | 150 | 506 | 748 | 1277 | 2681 |

| Raw Material cost | 147 | 493 | 728 | 1238 | 2606 |

| % of rev | 98.00% | 97.43% | 97.33% | 96.95% | 97.20% |

| Gross profit | 3 | 13 | 20 | 39 | 75 |

| GP Margin | 2.00% | 2.57% | 2.67% | 3.05% | 2.80% |

| Employee cost | 0.5 | 0.9 | 0.15 | 0.21 | 1.76 |

| Other expenses | 0.7 | 0.2 | 0.1 | 0.52 | 1.52 |

| EBITDA | 1.8 | 11.9 | 19.75 | 38.27 | 71.72 |

| EBITDA Margin | 1.20% | 2.35% | 2.64% | 3.00% | 2.68% |

| Other income | 0 | 1.1 | 9.6 | 20.9 | 31.6 |

| Interest Cost | 0.1 | 0.3 | 3.4 | 7.9 | 11.7 |

| Depreciation | 0 | 0.1 | 0.1 | 0.3 | 0.5 |

| PBT | 1.7 | 12.6 | 25.85 | 50.97 | 91.12 |

| Tax | 0.4 | 3 | 6 | 10.9 | 20.3 |

| Tax rate | 23.53% | 23.81% | 23.21% | 21.39% | 22.28% |

| Net Profit | 1.3 | 9.6 | 19.85 | 40.07 | 70.82 |

The company has given a guidance of reaching INR 18,000 crs of revenue in FY27.

In typical APL Apollo group company fashion, it works on negative working capital (-5 days)

Thesis:

Risks:

Disclosure- Invested

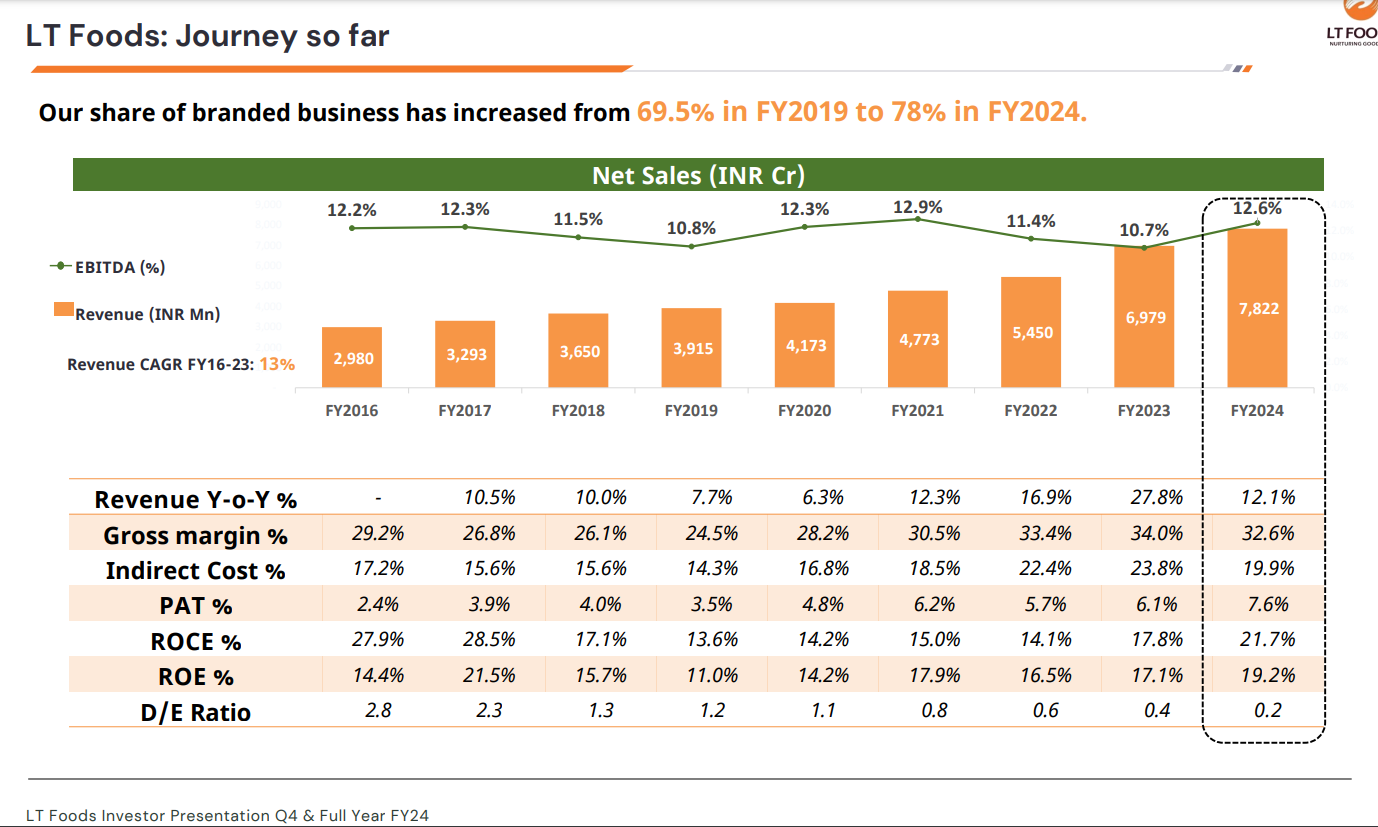

LT foods has doubled revenues in the last 5 years. They have a double engine for domestic growth: (1) increasing GDP per capita will increase overall rice consumption per capita, plus (2) as disposable income increases, more people will buy basmati rice, which is seen as a premium rice product in most of the country. Richer consumers will also chose premium / trusted brands like Daawat / Royal. Hence, if LT Foods retains its market share and “premium” branding, they should grow faster than Indian GDP growth. Exports will be the cherry on top, with increasing Indian diaspora abroad and also Indian food gaining popularity with foreigners.

So, I see a good runway ahead of growth between 8%~12%. But f you’re expecting 20%+ growth, this is probably the wrong company to invest in.

Thanks,

Sharad

OpenSourceInvestor @ Substack

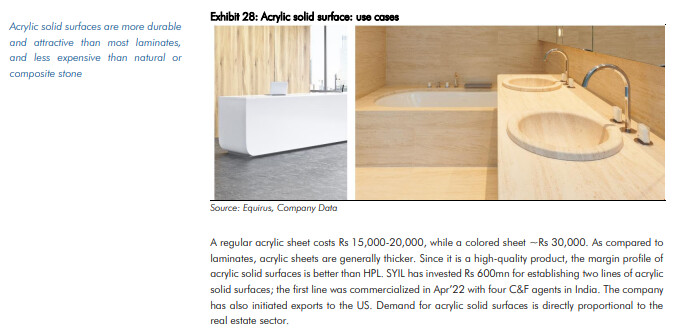

@rupaniamit since you track US real estate market closely (my assumption based on your work on Pokarna)

How do you see below product will impact Pokarna / Acrysil ?

Note : This is a slide from Equirus – Stylam latest report.

Many Thanks