Execution is impacted in Monsoons typically. H1 has had a double whammy for a lot of EPCs – elections, then Monsoons.

Posts tagged Value Pickr

Microcap momentum portfolio (07-11-2024)

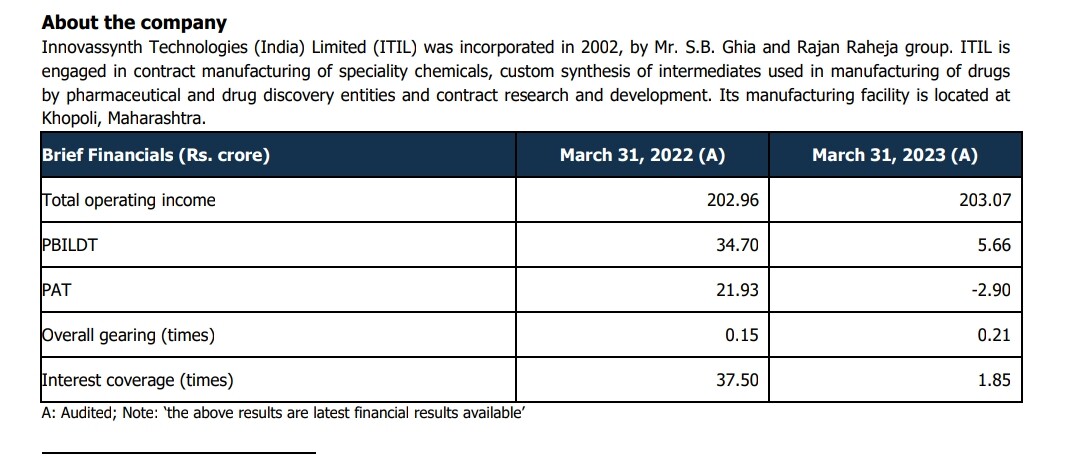

I checked in Care Reports where FY24 revenue is 200 odd Crore while PAT has dropped to negative which was approx 22cr in FY23. Is it correct?

Where can I find the latest numbers?

Also please share your rationale behind 450cr number. Will be helpful. Thanks in advance.

Steel Strip Infrastructures – Hidden Gem (07-11-2024)

Are you tracking after latest result ?

Microcap momentum portfolio (07-11-2024)

The Innovasynth investment and ITIL is going into reverse merger . Where in Utpal Seth of rare enterprise will be holding 15% stake based on pref allotment – LIC has 3% Raheja already own 72% – rest with public . CDMO is a big story and current mcap is highly discounted should be Atleast 450 crore based on their last 4 years performance and promoter good will .

Skipper Ltd., (Power and Water) a moat in making? (07-11-2024)

So many reports on the past couple of days, covering power T&D. Some calling it a Multi decade opportunity, all kinds of numbers being thrown around from 4lac CR to USD110bn opportunities.

If Skipper is able to win orders and manage timely execution – then we’re looking at a multibagger in making.

Huge runway and massive growth ahead.

Microcap momentum portfolio (07-11-2024)

Hi @Ankittivrekar ,

Could you share some more light on Innovasynth reverse merger story.

Piccadily Agro Industries Ltd (07-11-2024)

And here is Siddharth Sharma’s interview to Whisky Expert from Germany.

Firstsource Solutions Ltd (07-11-2024)

stock at ATH 381

HDFC Life Insurance Company (07-11-2024)

Q2 FY25 Update:

No. of shares = 215 crores (As of 31-12-2023 as per published data)

Embedded value (As of Q2 FY25) = 52,110 Crores

VNB (As of Q2 FY25) = 1,660 Crores

IEV + VNB (As of Q2 FY25) / share = (52,110 + 1,660) / 215 = 250.09

Valuation(As of 07 Nov 2024) = 711 / 250.09 = 2.84x

It has moved up from 2.47x to 2.84x during Q4 FY24 and Q2FY25.

If my calculations are correct, then the share price looks close to Fair Value to me or marginally undervalued.

Share Price has moved up from 475 to 711 during Mid 2022 to November 2025 i.e. about 50% which looks reasonable for a large cap stock.

Currently with No negative taxation imposed during current FY, slow growth from here looks possible but Insurance being highly regulated sector, predicting future growth is difficult based on my experience.

Disclosure: Invested from lower levels during corrections in 2022 and Holding from 5+ years perspective. No addition during 2024 to the position.