My observation for Tiger Logi are:

- Decreasing RoE, RocE

- Falling Sales

So may be avoided as of now.

My observation for Tiger Logi are:

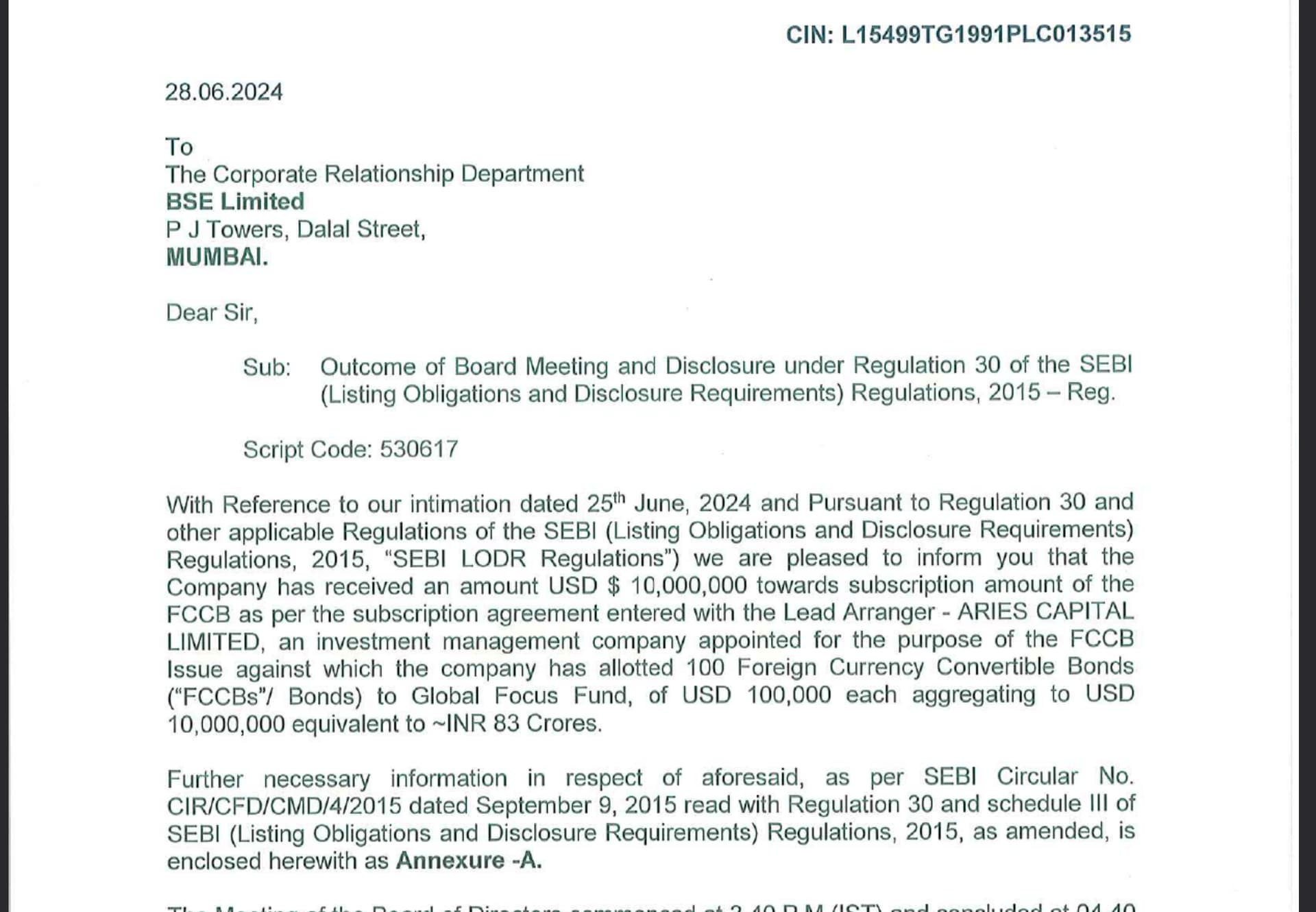

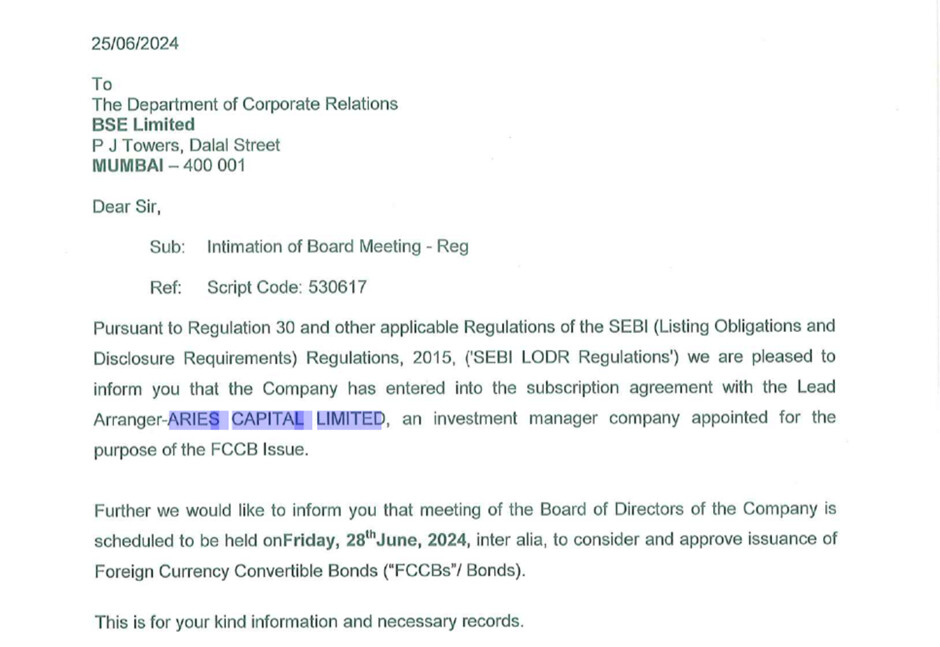

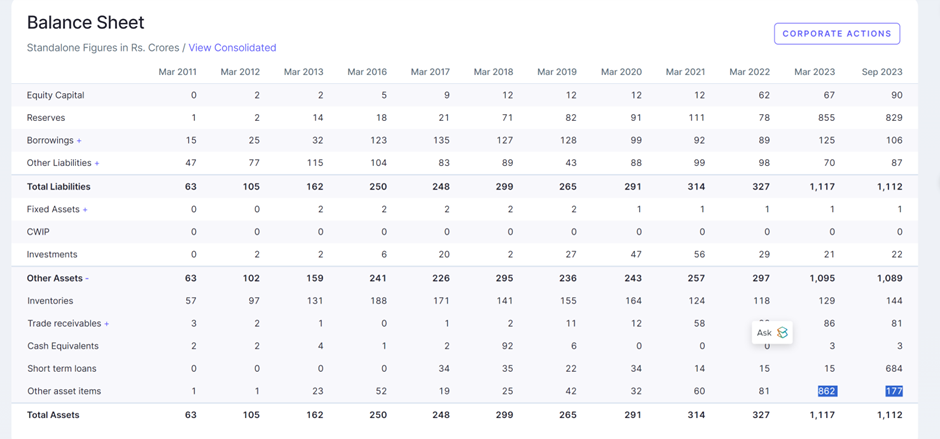

Sampre Nutritions is again doing a fund raising worth 83 Cr which is more than their market cap through FCCB after already done fund raising so many times.

The company had many red flags earlier regarding high volatility in margins and sales too but I choose to ignore it as it was exclusive manufacturer for Mondelez which gave the company some credibility and also through scuttlebutt I found that their plant at Hyderabad, Telangana was very good and since they were approached by Mondelez to set up a new plant for lollypops so fund raising made sense and since the promoter himself was not selling due to raising funds through preferential allotment he got diluted.

So I had mailed their investor relations for questions I had but I have received no reply.

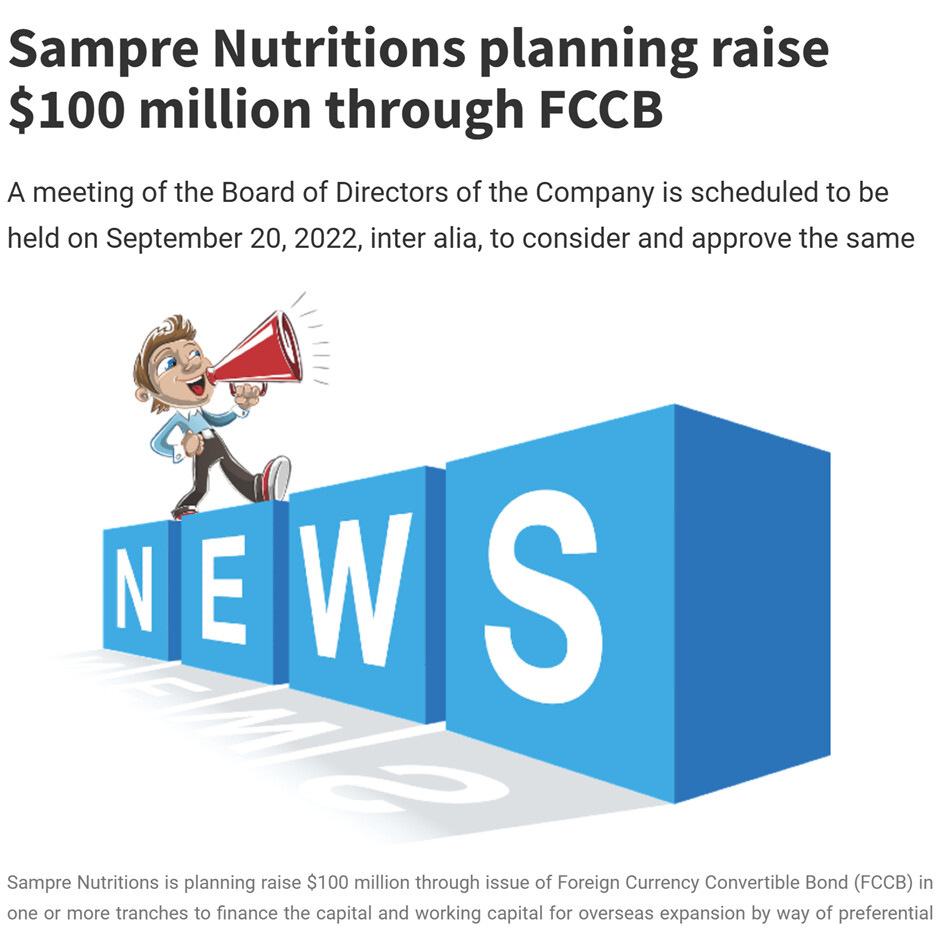

Now in the past they had also come with a similar circular that they would be raising $100mn

It was just a plot to pump and dump shares as can be seen in this chart.

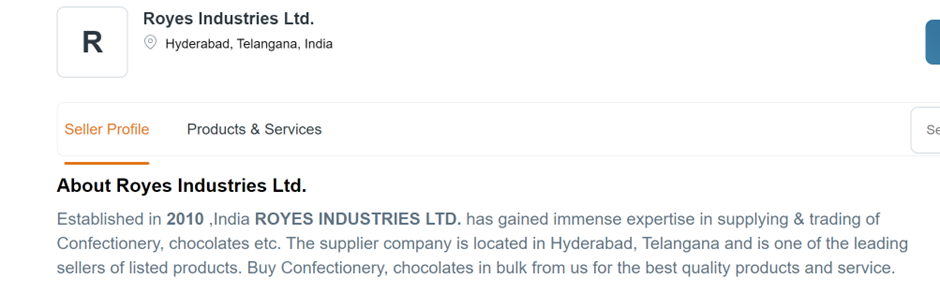

Their Related Party Company is in the same business

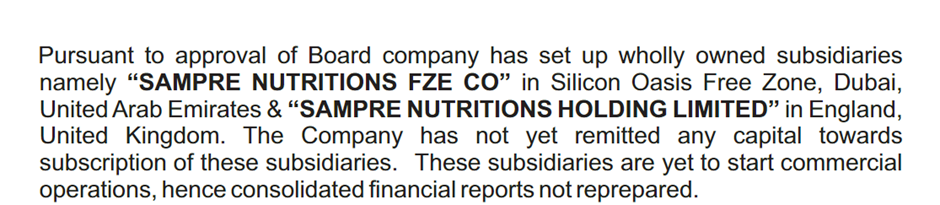

They have earlier made announcements of opening new subsidiaries in Dubai and England similar to their announcement now of signing an MOU with African.

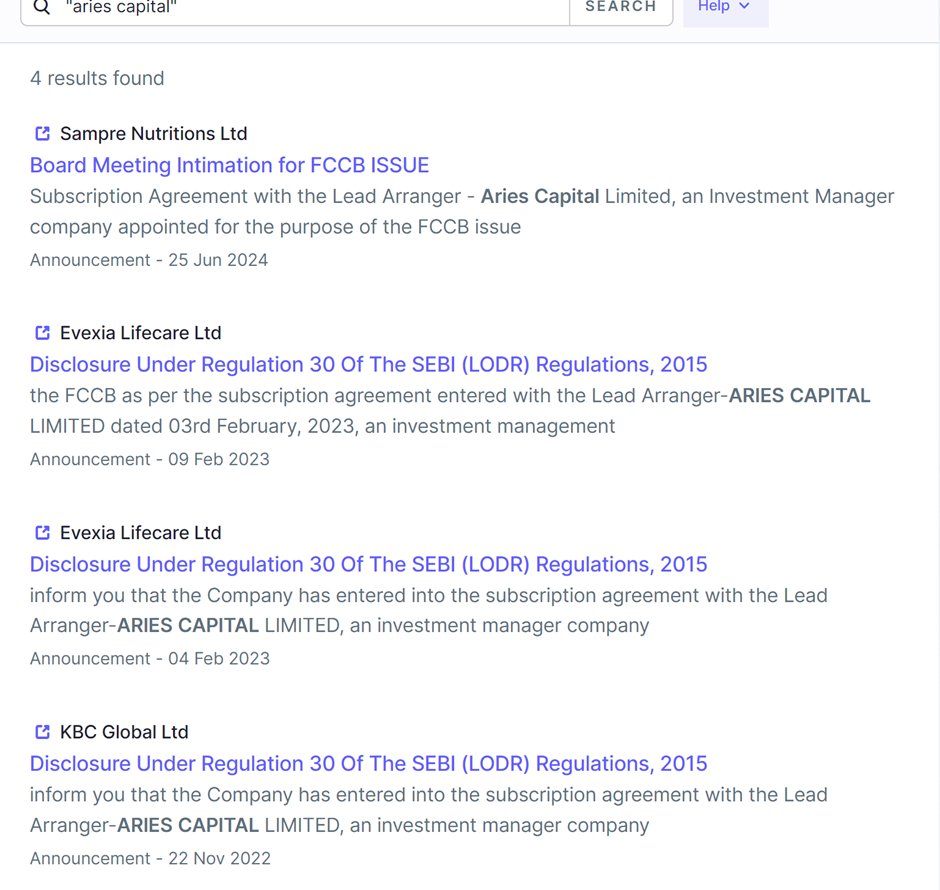

Now they are raising capital through Aries Capital Ltd as their lead manager, this company was also the lead manager for fund raising through FCCB route for Evexia Lifecare and KBC Global.

Now if we look at both these companies now:

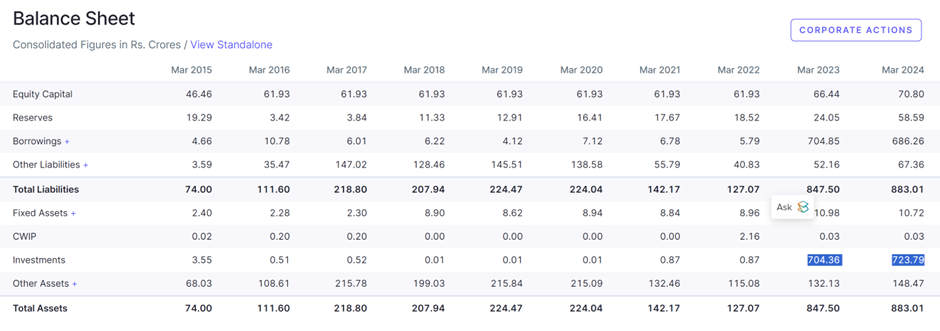

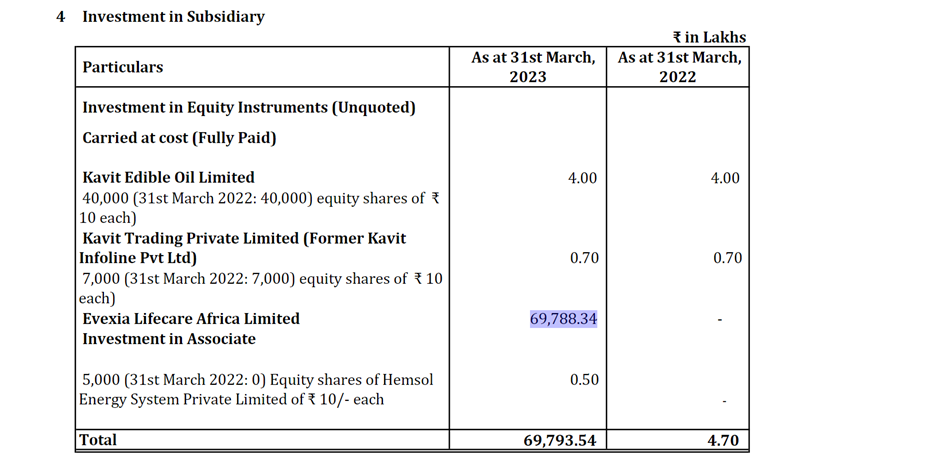

Evexia Lifecare’s borrowed 700 CR and then siphoned off this money in Africa

Similar pattern was observed in KBC Global:

Although after the announcement of fund raising the stock is locked in Upper Circuits I have decided to sell all my holdings as this company is most probably fraudulent and I choose to ignore all the red flags as it reminded me of Warren Buffet See’s Candy business and since they were exclusive manufacturer for Mondelez for eclairs, I was expecting an update regarding the money they had spent on importing machinery for manufacturing of lollypops for Mondelez and was expecting some increase in sales and margin once it goes live.

There is bad news… More shares pledged…

Slightly yes. Tempting to book profits.

A good price action with few corrections and bases is always good and gives more confidence in holding.

Does the rise too fast and too frequent make you nervous?

Got it, Sir.

Never thought it the way you mentioned. Thanks

I shall also be deleting my irrelevant post as they are not contributing towards R.S. Software discussion.

Very well written precise and relevant information. Thanks

Have started preliminary research on Five Star Business Finance.

A question I had is that how are they able to capture such high NIM’S at roughly 17%, which are almost twice of what peers like Fedfina and SBFC are able to get and in fact higher than most microfinance companies.

Any major differentiator in the business model per se?

Thanks.

The company’s receivables as a proportion of sales is around 20-25%. So I feel there should not be an issue of receivables rising at faster rate than sales. However, there is one concern of related party loans which have been highlighted here a couple of times.