I do not track this company.

Posts tagged Value Pickr

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (07-11-2024)

pl go through Investor call recoding of Dhampur Bio. Salient points:

Cane crush quantity for this season – no guidance as not sure.

Recovery – cant say right now

Distillery – when remain underutlised inspite of capex of 50cr for grain based modification. they could not bid for maize based ethanol as plant was not ready!! Management view – Maize prices are anyway going to be very high… but if it comes down due to some reason like imports… then also they will not be able to make ethanol !!

Company has plant for pharma grade sugar exports – but exports are banned ! so realisation is not as expected.

Focusing on country liquor – realisation is falling…

What is to be done with profits/cash as there is no capex – this is most convoluted reply i have ever heard.

Lots of promises but poor delivery… company has potential but something or the other happens… is it bad luck or bad management?

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (07-11-2024)

(post deleted by author)

KPI Green- Turning Sunshine Into Cashflows (07-11-2024)

pl compare with trailing quarter… then you will know why KPI is falling.

Raymond – The Complete Man (07-11-2024)

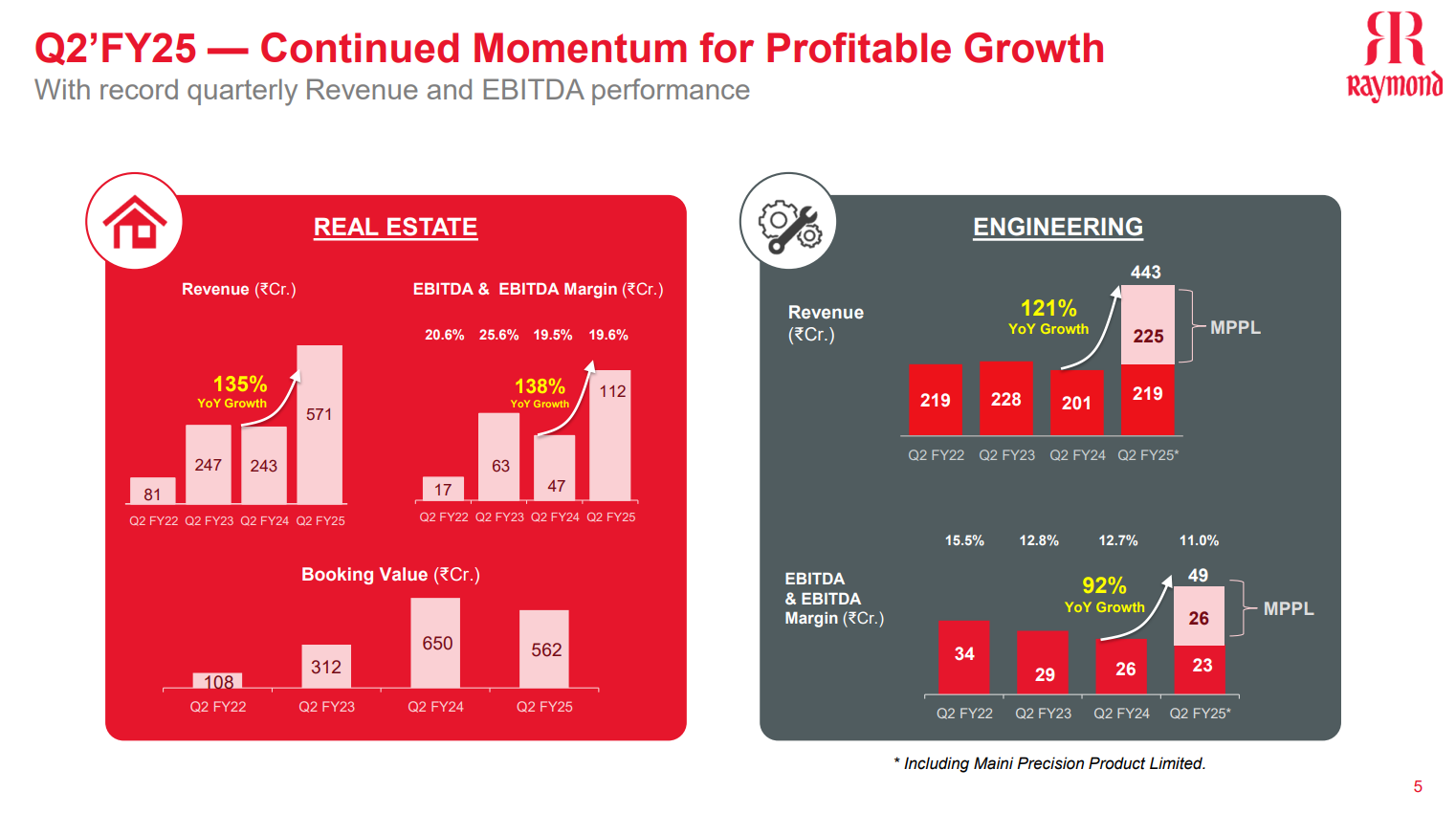

This shows the comparable base, also separates the MPPL revenue.

Engineering (excluding MPPL) has remained flat over last 4 years in Q2.

Manappuram Finance (07-11-2024)

I don’t think quantum of risk is changing much in MFI, and as far as rates go they don’t have a choice but to lower under RBI enforcement.

Nitiraj’s Portfolio (07-11-2024)

Let me give you some broad advice. Even if you want to invest for reasons other than profit, you can do it in a methodical; structural way or build a broad understanding in any other way which suits you.

Start with the highest allocation stocks in your PF, whose threads exist in the forum, there will be many from your PF. Go through them and let an understanding develop, even if it takes some time. As you already know, market isn’t going anywhere. If you are interested, make this forum your first place of knowing something, unless what you seek does not exist, which isn’t usually the case.

Not just the number of companies whose threads exist, we have members who come from different schools of thought; who have diversified investing philosophies, who participate differently. I am sure one or more such styles resonate with you.

Renewable Energy Listed Companies who could give good returns in future (07-11-2024)

Which are some Good Energy Based companies (any sector) from Mid-cap category to invest in and to hold for 8-10 yrs for good potential returns .

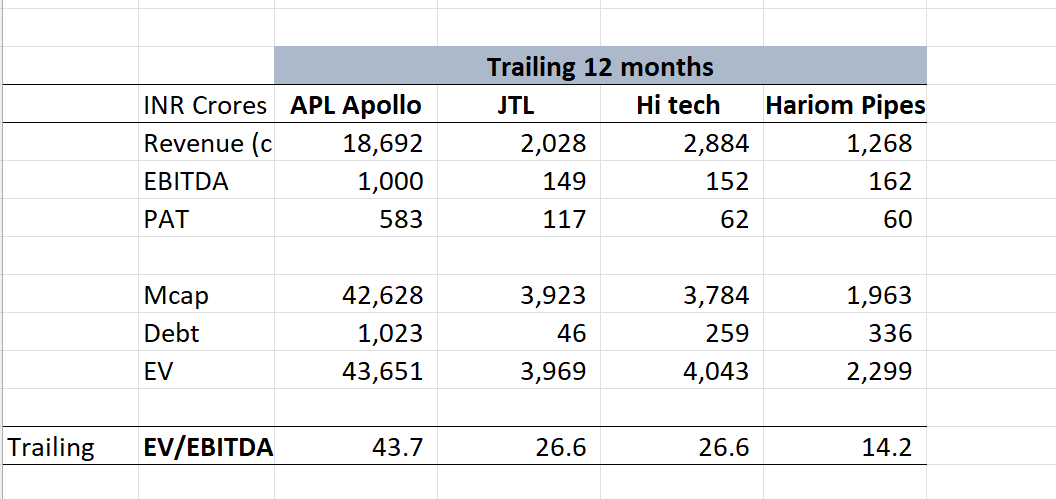

Hariom Pipes Ltd: A Capex Play! (07-11-2024)

Now that all pipe companies have reported Q2 numbers, here is compilation of valuation comparison based on EV/EBITDA.

Note: This is based on trailing reported numbers and doesn’t take into account future growth.

Source:Screener

If we consider CFO’s guidance of 330+ crore EBITDA in FY26, then EV/EBITDA would look like 6.9x for Hariom

Sandur Manganese (07-11-2024)

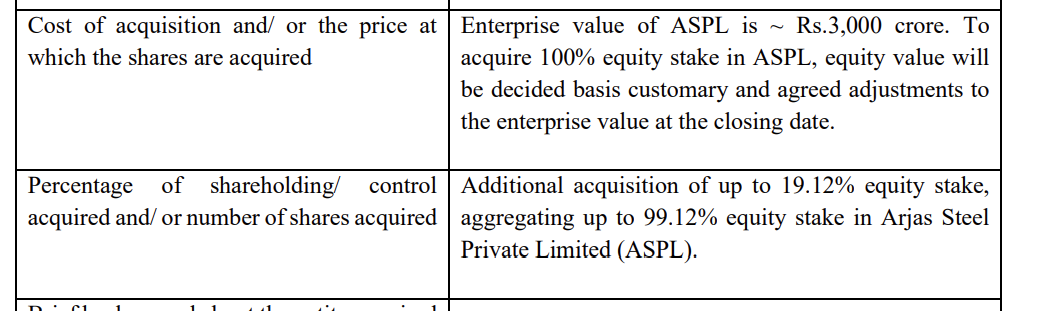

Did they randomly change to buying 100% of Arjas; instead of the 80-20 split between company and promoter?