Amara Raja to start operations at battery recycling plant | Autocar Professional

Posts tagged Value Pickr

Voltamp Transformers (07-11-2024)

Completely agree with you. When a structural tail wind starts, it takes at least 12-18 months for new capacities to emerge to fulfill the rising demand. During that period, companies having good quality and spare capacities make outsize gains. It does not makes sense to compare their performance with their past, as demand environment has changed completely. With yesterday’s Trump victory, AI, data centers and Cryptos (and crypto mining) will be given big push, which has potential to drive power demand further.

Coming back to company specific issues, it is hard to note why Voltamp did not perform in such a benign environment. Company not doing any investor communications like investor presentations and quarterly conference calls is a big negative for any investor like me.

Disclosure – invested in TRIL and Shilchar. Interested in Voltamp but can not invest due to lack of information

Microcap momentum portfolio (07-11-2024)

How much amount and how many stocks you have scanned before investing to this rule based system.

Tips Industries Limited – Ready to RACE ahead! (07-11-2024)

Seeing people discussing valuation of Tips Music on PE matrix. In my opinion Tips Music is a pure play music label which cannot be valued by just calculating PE by seeing profit alone. Tips is charging content cost in expenses of P&L account and not capitalising it and the content cost is kind of not a raw material for top line of the same period, it is more like a capital expenditure for future growth. Suppose, if Tips gets an opportunity of buy very good music at good deal and they spent almost all the revenue for the particular year in buying that content then the PE will be very high or in negative but the company will save good amount in taxes apart from ensuring solid growth. Content cost can be a problem if the company is not spending prudently, however, having observed the strategy of Tips for last 4-5 years, I thing they are quite conservative and prudent in buying new music.

If I have to value the Tips of PE matrix alone, I would calculate based on top line and not on profit. For instance, TTM Sales are Rs. 283 crores which results in operating profit of Rs. 268 crores (assuming 95% OPM, ex of content cost). Now, lets assume there is tax rate of 25%, the PAT works out to be Rs. 200 crores. Now calculate the PE, it is less than 60 and not 80-90.

Having said that, I understand if they don’t do content acquisition, the growth will slow down but I feel most of the growth is coming from their legacy content coupled with structural shift of paid customers and ads revenue of music platforms.

Disclaimer: Not invested

Voltamp Transformers (07-11-2024)

When the industry is in strong tailwind and became sellers market, unable to understand the margin erosion. Waiting period for delivery in USA has become 2 to 3 yrs. Shilchar is in Distribution transformers in renewable energy sector while TARIL is in high capacity Power Transformers. All the three are not strictly comparable. INDOTECH also reported good numbers. It is my perception if they are not able to command margin in a Too good to be true market, there may be some strong reasons for the Not so good results. Respectfully I disagree with you on honesty front of fudging possibility of results by the other two. I have exposure in all the three from lower levels .

Neuland Laboratories Limited – Transformation towards niche APIs? (07-11-2024)

Long term prospects are intact and Company as earlier advised is expecting strong growth momentum from FY 26 onwards.

Piccadily Agro Industries Ltd (07-11-2024)

OK. Just for the record; this is Siddharth Sharma, the driving force behind Piccadily and biggest individual shareholder (22.73%)

Infollion Research Services Ltd – Moated Microcap with Differentiated business? (07-11-2024)

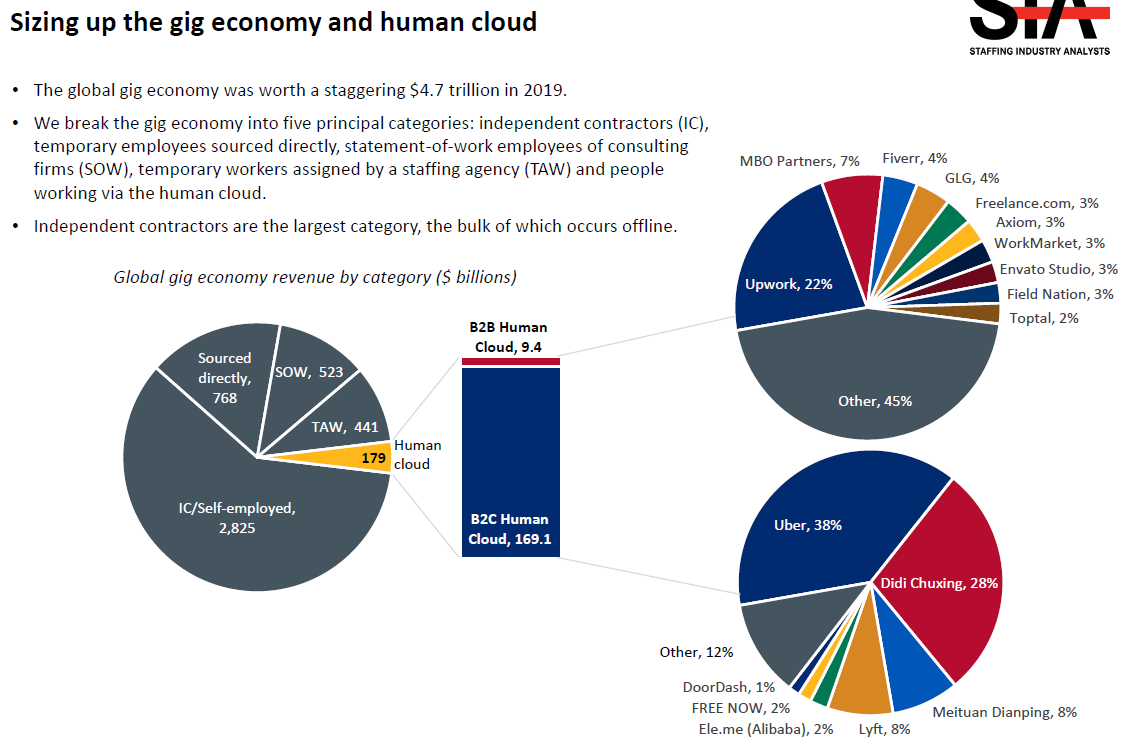

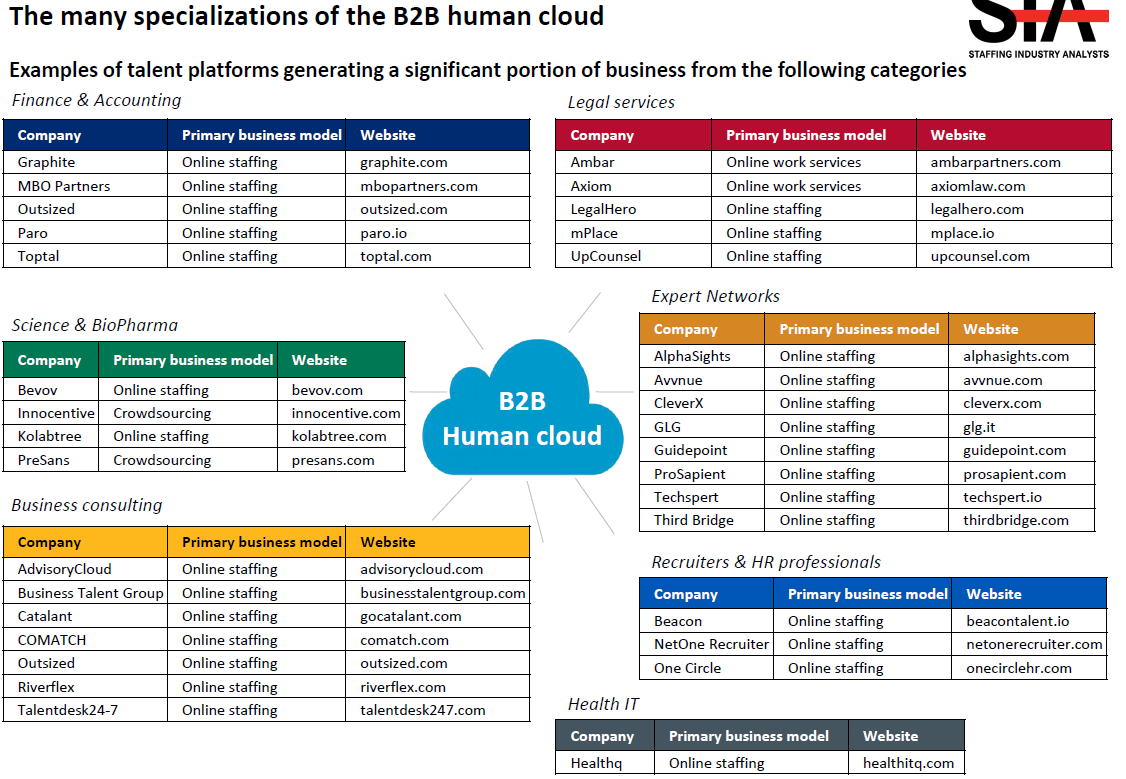

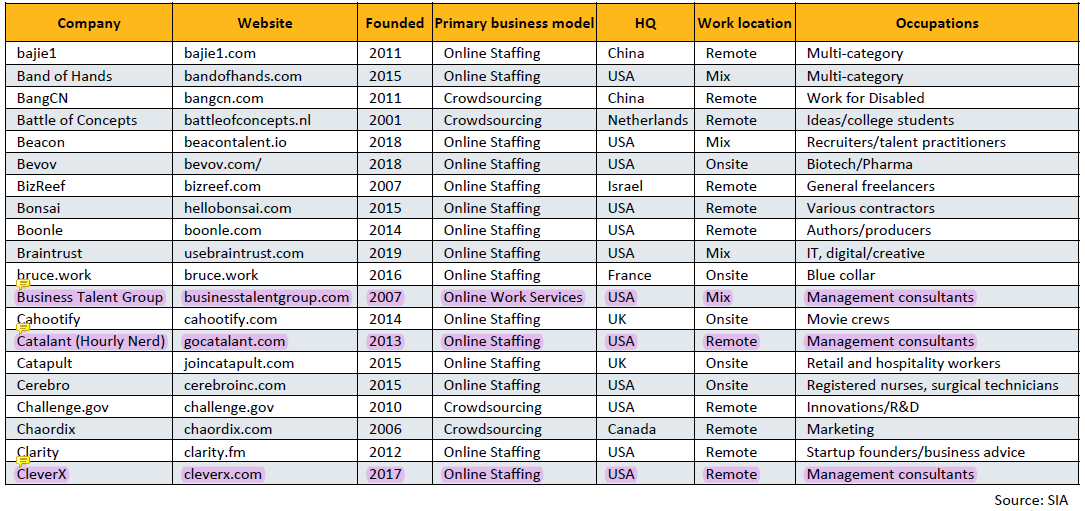

Sorry think writing this at Midnight may caused to miss some points. Just to Add some More in Market size.

These are kind of subsector or part of GIG economy and staffing Industry.

Check this : https://apexassembly.com/wp-content/uploads/2021/02/The_Gig_Economy_and_Talent_Platform_Landscape_1.pdf

In Overall Human cloud Market

It’s not an apple to apple comparison but we can get some idea.

See how the part are been divided into

Some of the Financials i have provided at the Top.

Check out the List from Page 66: Occupations to be checked are Network expert, Consultants etc…,

BSE (Bombay Stock Exchange)- Bet on Financialization? (07-11-2024)

BSE LTD is now added to MSCI INDEX

Manappuram Finance (07-11-2024)

I think what Manappuram will do is stop giving out risky, high-interest loans. If they stop these high-interest loans, it won’t have a huge impact because most of their loans are at average risk with average interest rates, and only a few will be high risk. Earlier, they could charge very high interest on these few risky loans, but now they’ll cut back on those and focus on little safer, average-interest loans. I feel the high-risk loans aren’t a large part of their business, stopping them shouldn’t affect much. Offering the lowest interest rates in the industry could actually drive growth and help balance any impact. It’s complicated in theory, but practically, it won’t make a huge difference on paper. I think within 6 to 12 months, they’ll be back to near similar levels in profitability and NIM , if not exactly the same. Let’s see how things go as the numbers start coming in if and when ban is lifted

At least ban lifting seems pretty easy of they are planning to offer lowest interest rates in industry

Management mostly do what they speak

Last time during ED fiasco management guided well and same thing happened