@Adhiraj ji any plans for a meetup in the near future?

Posts tagged Value Pickr

Action construction equipment ltd (30-06-2024)

I can see the ACE cranes all over here in Hyderabad. This really gives me conviction of staying invested in ACE. I’ve been here since quite a while now and I can only see the construction activities growing like anything. Not just new buildings are erected but the old ones are moving into redevelopment as well. So the future seems bright for ACE.

Action construction equipment ltd (30-06-2024)

I can see the ACE cranes all over here in Hyderabad. This really gives me conviction of staying invested in ACE. I’ve been here since quite a while now and I can only see the construction activities growing like anything. Not just new buildings are erected but the old ones are moving into redevelopment as well. So the future seems bright for ACE.

Screener.in: The destination for Intelligent Screening & Reporting in India (30-06-2024)

How to download it. Please elaborate.

Action construction equipment ltd (30-06-2024)

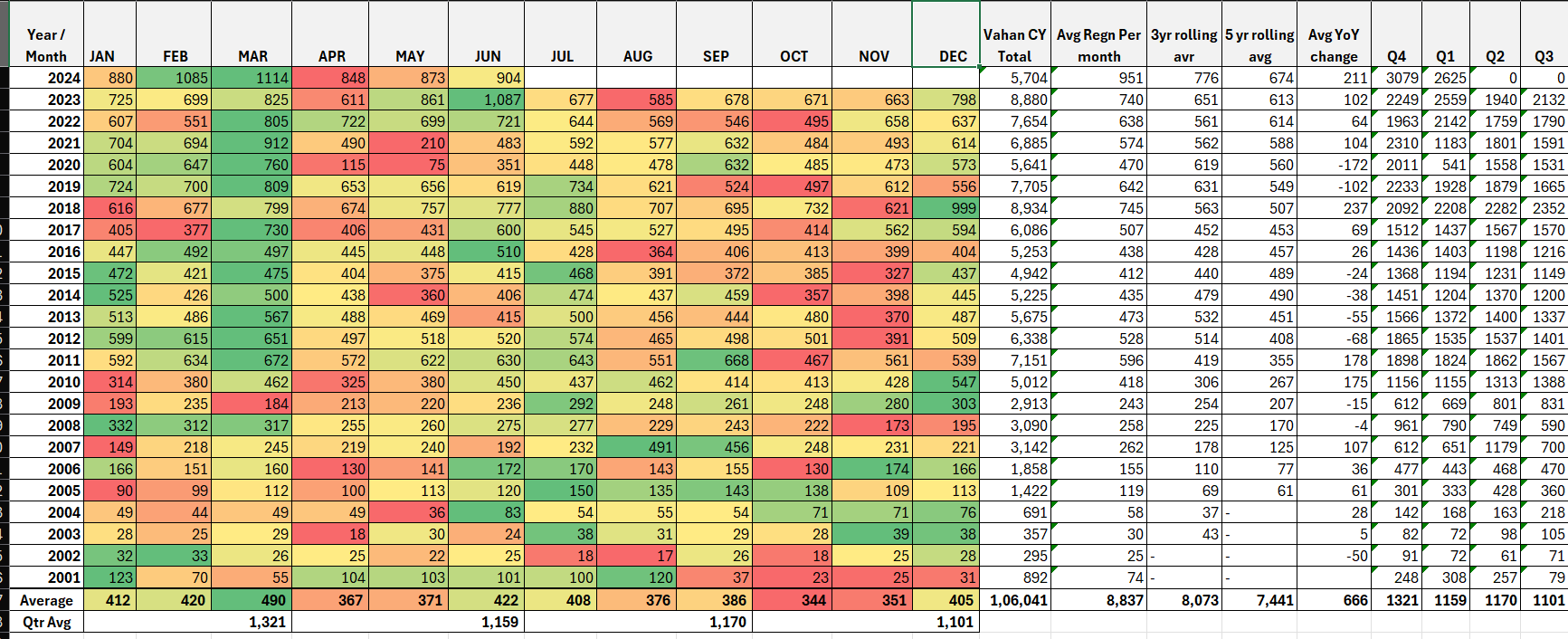

June End VAHAN Regn Numbers for ACE –

- 904 Regn in June till now, higher than May, Apr.

- 2625 Q1 FY25 versus 2559 in Q1 FY24 YoY, 3079 Q4 FY 24 for QoQ

- If similar number continues, we will see 10K for the year,

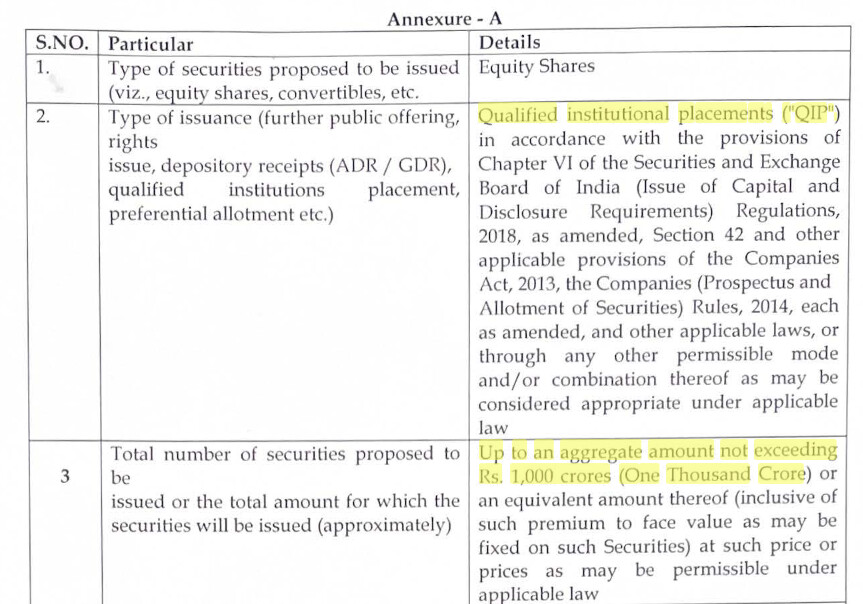

Poly Medicure – at an inflection point! (30-06-2024)

Recent exchange initimation –

Fund Raise was indicated in Q4 Call

Caplin Point Laboratories (30-06-2024)

Caplin had another great year, with 16% sales and 21% EPS growth. Concall notes below

FY24Q4

-

INVIMA successfully audited CP-1 facility at Pondicherry for soft gel capsules. This will cater to Mexico, Chile, and other major geographies of Latin America

-

Caplin Sterile

-

Does very little CMO and efforts into building own ANDA pipeline is finally paying off (313 cr. sales; 61.2 EBITDA, PAT 18.7 cr.)

-

Increased volumes from 16 mn vials in FY23 to 27 mn vials in FY24

-

Started discussions with other CMOs for outsourcing manufacturing of high volume products while keeping high-value low-volume products in-house

-

Out of 3 ophthalmic approvals, launched 1 and will launch 2 more soon

-

Launching their first ready-to-use bag injectable product in the U.S.

-

-

Capex

-

Line 6 for prefilled syringe and cartridge is being qualified and will be used to manufacture new peptide injectable products for global markets

-

50-55% of capex is completed, CWIP is 116.6 crores. Pending investments are in the new OSD facility, API, and major equipment for injectables**. 250-300 cr. remaining** and will be finished in next couple of years

-

-

LATAM contribution: Guatemala > Nicaragua > El Salvador > Honduras > Dominican Republic > Ecuador

-

Completed registration of 85 products in Chile, opening a new warehouse in Chile

-

Received 6 marketing authorizations in Mexico, filed 23 products, 12 products are from Chinese companies. Once they register 25-30 products, they will start own warehouse and get into the private market in 2-years

-

Looking to get into insulin, biosimilars and peptides by sourcing it from Chinese vendors and doing fill-and-finish in India. Targeting regulated markets of Mexico, Brazil, South Africa which require Phase III studies. Do not plan to go into USA for selling biologicals

-

Automated QC and microbiology side, have taken a software partner for automating all their manual logbooks to electronic logbooks in next few months

-

Increase in working capital: always believe in keeping inventory closer to the end market

Disclosure: Invested (position size here, no transactions in last-30 days)

Rudra’s PF and Information attic (30-06-2024)

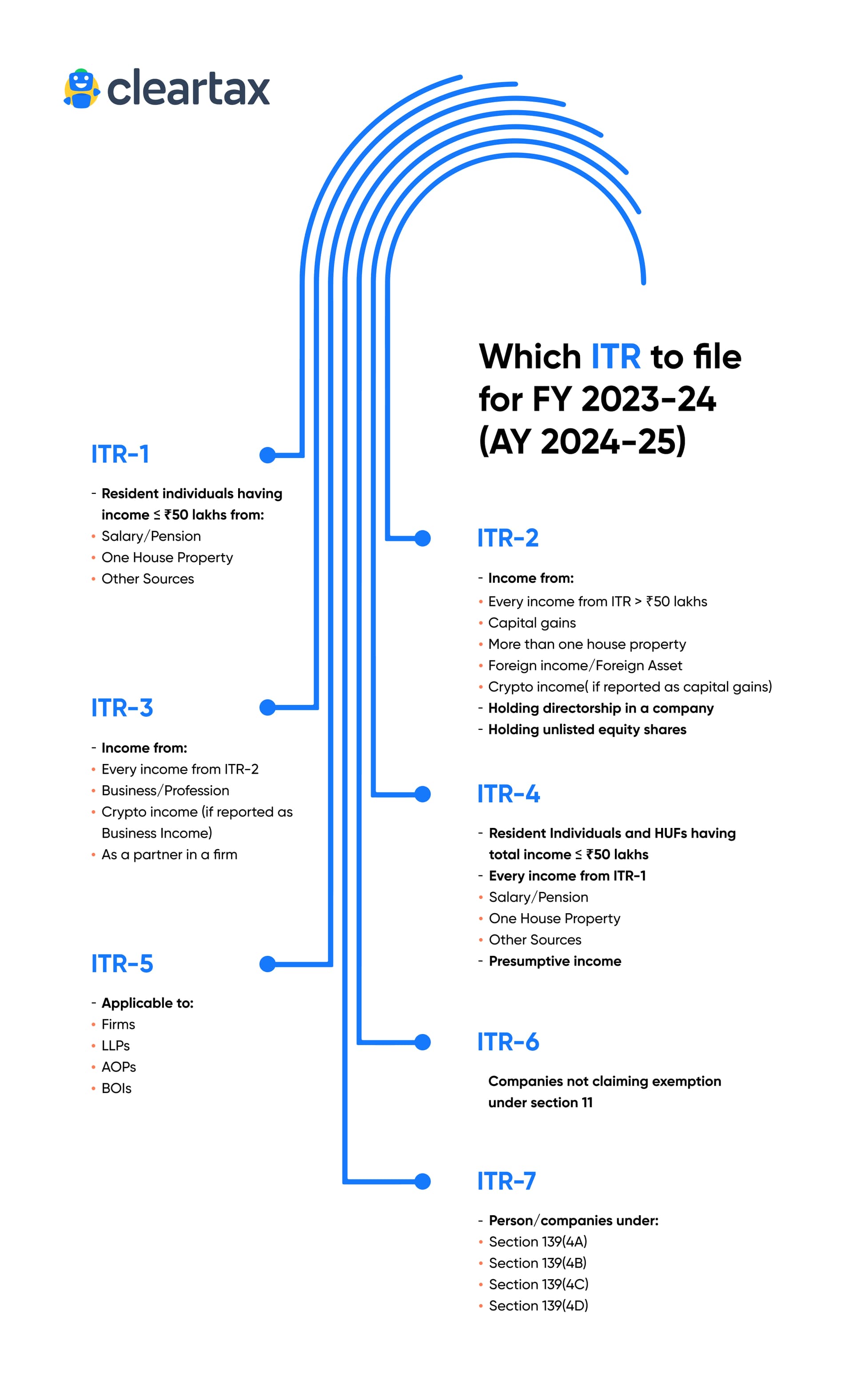

Tax filing season is on and this infographic beautifully captures all the different ITRs.

Source

Tembo Global – Infrastructure proxy? (30-06-2024)

Thankyou for the pointers. I went through the details. I could not find why the promoters did not subscribe fully to the rights issue, but the pointers were really helpful to understand the business better. May be not a good business, but to develop and understanding, below are my assessments.

- Their cash is mostly tied up in inventory and loans & advances so it is not a real cash item thus the actual cash profit is affected.

- Cash flow from operations is -ve for FY23-24 which is not a good sign. I understand that atleast the cash flow form operations should be +ve indicating that at least some of their notional profit is getting converted to cash. In this case, they will need to borrow money for day to day operations also.

- Their fixed asset growth is less so they are not expanding physically. Means they are not seeing growth in their engineering products business. So one question here is why is their inventory increasing? Could it be due to their trading activity?

- They have more capital employed in the engineering products, but they had a -ve profit margin there in FY24. If their assets are not growing much, then where does the capital employed go? Also they are having more sales in trading business so why is the capital employed in engineering business more?

I no more hold this company but I am curious about understanding a business, their balance sheet, cash flow etc and this is now just one company that I am trying to understand as a part of my learning.

Bull therapy 101-thread for technical analysis with the fundamentals (30-06-2024)

Krishca Strapping- a breakout after a long time, with strong volumes confirming the shift in the trend.

The new unit which is to sell higher margins straps is commercialized. They have doubled the capacity with this unit, taking the revenue potential to 300cr at peak utilisation. This yr they plan to do 40-50% utilisation, and will fully utilise it over 4yrs (although i expect it to be a lot earlier)

The peak revenue of 300cr, is excluding the packaging segment which can do a lot more then strapping segment once they get more approvals

They have also introduced another segment of products, primary packaging, which again is expected to be higher margin.

Have opened up their khaata with SAIL with 2 orders. Its very difficult to get into PSUs, SAIL has given them their smallest plant for now, SAIL has a lot many more plants, huge opportunity opens now.

Only 3 companies compete here, the new fourth one is krishca.

Mid East plan is still on, to setup a unit there, this can be very huge, as they will be the only one with a unit here and will be able to source rm from cheap asian countries, hence can compete even with china

Export sales is growing very rapidly, to do 30cr+ this yr and 100cr in the next 5yrs, i feel it can be done sooner.

Focusing on several new countries and already getting repeat orders, although smaller orders

The biggest risk here was a small TAM, but now they are getting into other prods (ofc a natural diversification and nothing else), these are higher margin then straps.

- one expansion is done

- new expansion is being planned

- packaging segment is moving very well, considering its the first yr of operations

- new geographies will now open up

- new prods are being introduced

Also recently the company has given an intimation of a potential fund raise, which i assume will be used for this new expansion and the Mid East expansion.

there is detailed thread on this company, if needed

invested and biased