Zee Music Company on YT has around 111M Subs. Company hasn’t disclosed revenue from music division till date. VIDIQ YT stats indicates $1MM-3MM in monthly earnings. Conservatively that’s ~100crs of annual revenue just from YT, and I haven’t taken into account licensing revenue(tie up with Insta) or revenue from streaming services. What am I missing? Just carving out Zee Music should contribute as much to Mcap as much as Zee Enterprises.

Posts tagged Value Pickr

Manappuram Finance (06-11-2024)

I don’t think sir , it is a masterstroke. It will lead to compression in NIM and ultimately will reflect in ROA.

It is RBI action which leads to such action by management. The same concern is raised in QnA in recent concall and management very beautifully diverted to “strategy which is expected to drive growth”. I began to smile after listening management answer and also admire the quality of how to show positiveness in negative things.

Disclosure: Invested from 89 levels. Will love to hear your counter views.

Piccadily Agro Industries Ltd (06-11-2024)

My intention was not to point in that direction but to highlight the fact that they are not just part of Promoters group but rather owners of the company themselves, which is good. And as investor and fellow citizen, i think they have made their investors richer and brought pride through their products from all around the world.

[Disc: Invested with sizeable allocation in my pf]

Screener.in: The destination for Intelligent Screening & Reporting in India (06-11-2024)

Fantastic to see Screener.in adding index information—it’s such a valuable addition for quick insights into a stock’s broader market context! This was also on my list for Screener Specter and I’m thrilled to see Screener bringing this feature to the community.

Demerger of Adani Enterprises (06-11-2024)

Super insightful, and I wish I had come across this back when the saga took place.

Stop the Count – US Policy impact on Indian Equities (06-11-2024)

True. Many things have been said to win the elections, but it’s not necessary it will be done.

Stop the Count – US Policy impact on Indian Equities (06-11-2024)

He did say he wants to devalue the dollar. But looking at bond yield and Dollar Index spike, I guess we can safely say that the world’s confidence in USD has increased.

This has more to do with both the President and Senate being Republican. Control over the House of Representatives is still up for grabs, with Republicans leading.

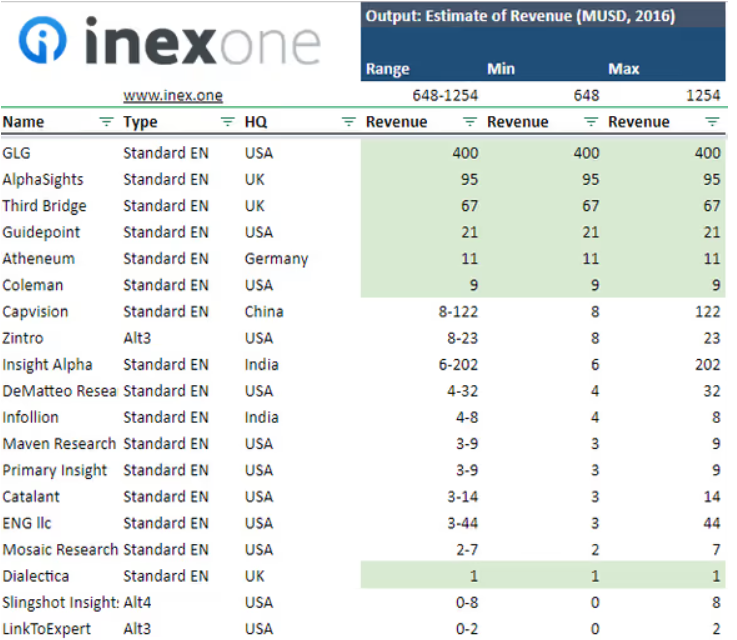

Infollion Research Services Ltd – Moated Microcap with Differentiated business? (06-11-2024)

Some Notes – Peer Comparsion

-

well-known global expert networks so the fees were like in the neighbourhood of i think 800 to 1100 dollar for a one-hour call.

-

Infollion – Starting from 400 dollars.

-

The expert network industry had over 100 active players in the global landscape in 2020

-

GLG has grown fast and forecasts that its revenues will rise by 15 per cent this year to $400m.

-

Experts within GLG’s network can earn up to $1,000 an hour for a phone call.

-

It costs about $100,000 for a group of four people to access the network for a year, while the heaviest users pay millions of dollars

Market

-

The industry held up as revenues surpassed $2.28 Bn in 2023, generated by about 120 experts.

-

Within 2 years recently industry grown 20%

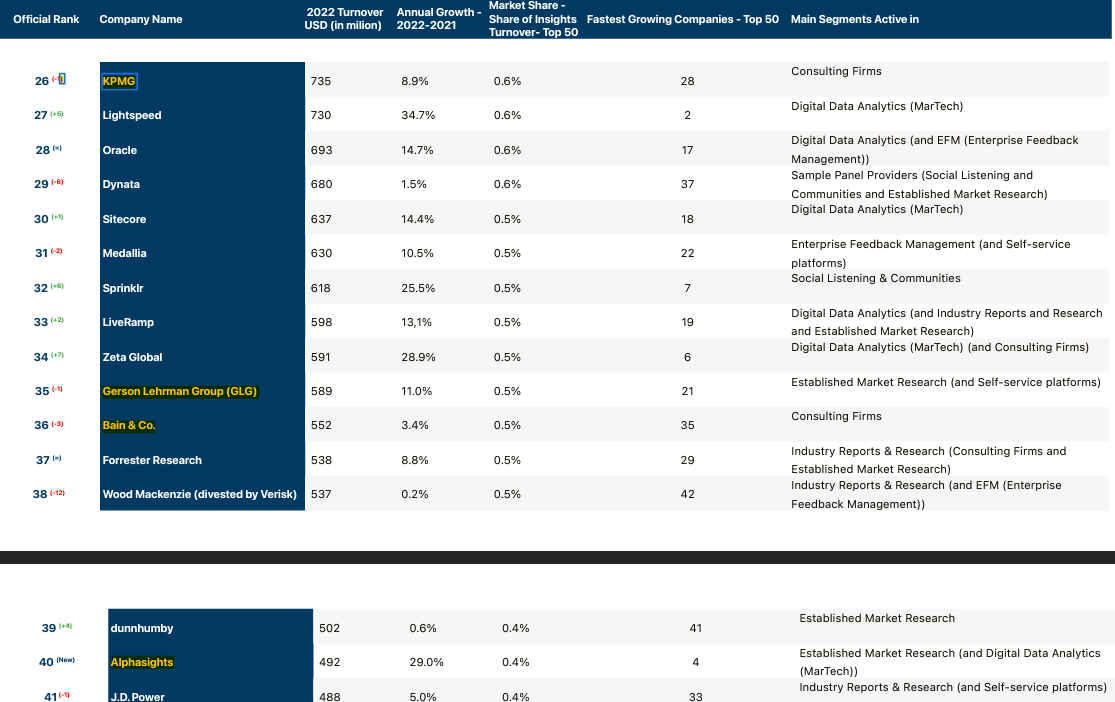

Peer List with Revenue

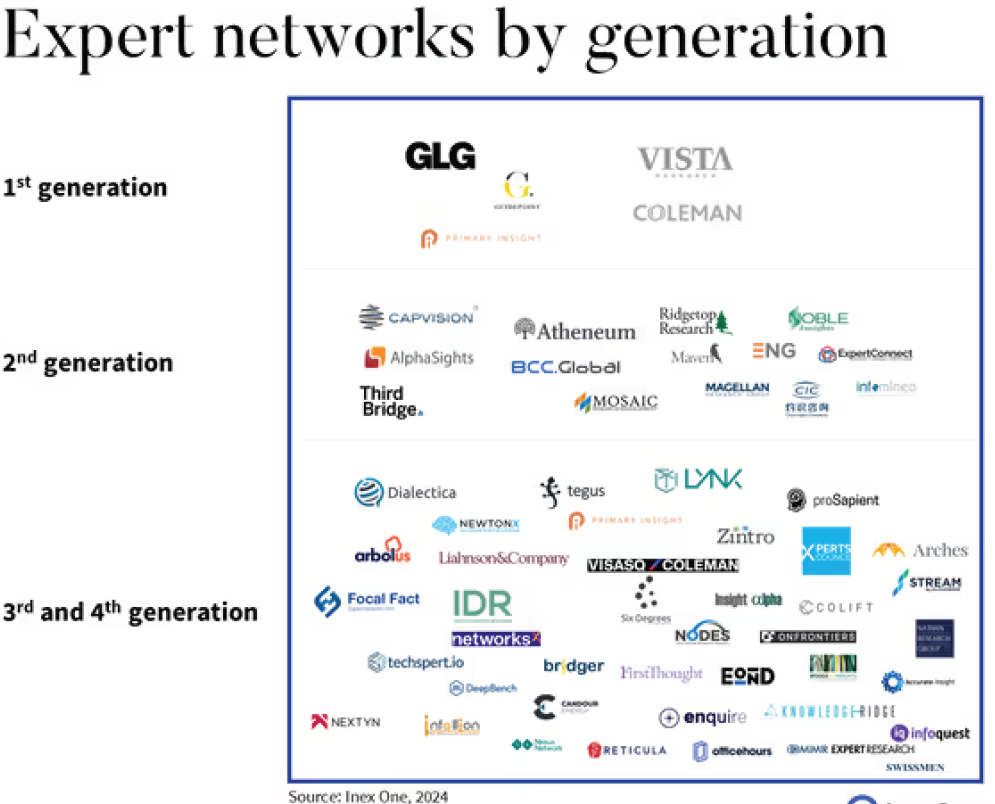

By generations

1st – Before 2006

2nd – after 2006

3rd – Mid of 2010

4th – Recently found.

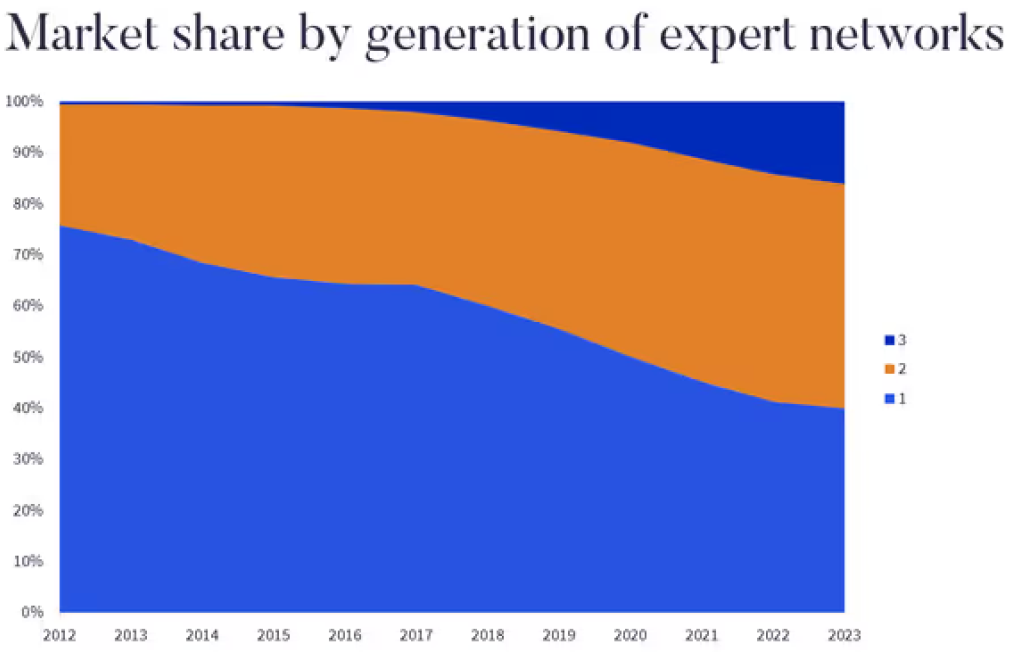

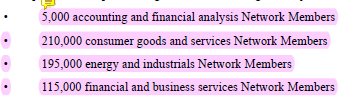

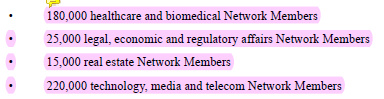

Market Share Split

Regional Leaders

Regulatory Evolution in 2000’s

Gross Margin – Comparison

For Thirdbridge

For DIALECTICA LTD – UK

For Prosapient Limited – UK

For GLG – DRHP

Revenue Contribution of GLG

Expert Counts GLG

One more interesting data – experts in Specific Industry

All data is collected from AR and DRHP’s. Some might be specific for one region alone.

Market started getting consolidated

VQ decided to acquire Coleman

Check this PPT : https://corp.visasq.co.jp/release/20210818en.pdf

Leader in Network Expert as per Forbes in 2021

Kind of Regional Players

- Bryan Pena (MBO Partners, US)

- Max Friberg (Inex One, Sweden)

- Martin Tronquit (Infomineo, Dubai UAE)

- Nitin Kunimmal (Avvnue, US)

- Sharekh Shaik (CleverX, India)

- Mac Mabidilala (Pengo Insight, South Africa)

- Luis Mata (Consultok, Chile)

For More: ESOMAR – List of Top 50 players including Consulting players.

https://esomar.org/uploads/attachments/cllyzri8j06pkif3v31ipx081-top-50-insights-companies-2023-6.pdf

Some Questions

As they are n number of players in US. How Infollion will do its best?

- Acquisition might help to grow fast

- Operating front end from India – sightly helps

What else? Cost of US expert to US clients maybe same for all the players in US right?

Is there something I am missing on the above question?

Growth – Alphainsights

we are almost 15-year-old Company – from Concall, why infollion didn’t? After IPO promotors is getting excited ?

Possibility as a 2st gen player – alpha might have got some upper hand. But is it?

Some helpful Links

Insider’s Guide to Expert Network Consulting with Zintro’s Michael Collins

Inside View of Expert Network Industry: Feat. Akshat Naithani (DGM, Insight Alpha)

EFC – Entrepreneurial Facilitation Centre (06-11-2024)

- Did anyone notice that their cash flow from operations is wrongly calculated in financials statements (consol.), it should be 28 Cr instead of 150 Cr. Interestingly, it appears to be wrongly calculated for FY-24 on screener as well, it should be 16 Cr instead of 29 Cr

FY-24

- Anyways, receivables have turned positive I believe for the first time, which is a sign of good ROCE generating business and ideally, since they take rent upfront it should remain positive as they expand

Some concerns:

- They had given a target of 65-70k seats for FY25. Since they add under development seats too in their seating capacity numbers, let’s assume we would have 61k operational seats by end of FY25. This means that they need to add 2x the number of seats in H2

- They had given guidance of 2x revenue in FY25 which seems unlikely to happen. We should ask them if they would like to revisit their guidance. I estimate around 60-65% sales growth over FY24 which is still decent

- As per their ppt, their rentals paid to received has increased from 40% to 45% but EBITDA has remained same at 25%. Interestingly, in rental division EBIT margins have increased from 22% in Q2FY24 and 24% in Q1FY25 to 39% in Q2. I am not sure what is the reason for this sudden jump in margins as rental prices have remained same at 6250, rentals paid has increased by 500 bps, employee costs have remained same YoY and improved by just 53 bps QoQ – @manhar if you can shine some light on this

- Rental revenue based on 90% occupancy on 46.8k seats should be 79 Cr but they have reported it at 89 Cr, either they had high occupancy earlier (seems unlikely as this number was 91% in Q1). Again, I might be missing something here

- Avg rent per seat seems to be constant for last 1.5 years. Why have they not even increased the prices by 7-10% to account for inflation? Do they lack pricing power this much?

- Interior EBIT margin has also increased by 800 bps QoQ, what could be the potential reason for this?

Discl: Invested.

Voltamp Transformers (06-11-2024)

This may have some info that you are looking at ( though bit dated now. TRIL, CG, Voltamp each has significant capacity addition from that time, can be tracked easily in recent communications by each ):