If Donald Trump Wins: The Good, Bad & The Ugly For India & Stock Markets | Talking Point With Niraj

FII outflows will continue he says (among other things).

If Donald Trump Wins: The Good, Bad & The Ugly For India & Stock Markets | Talking Point With Niraj

FII outflows will continue he says (among other things).

Invested

EPS down 3%, OPM seems the same. Not very inspiring.

Also anyone can tell us why promoter seems low given that we thought it was handed over from one family unit to another? Must have missed something, but what?

please do your due diligence and verify above

Is this release discussing the same Vidyalaxmi programme that Protean runs? Even Protean has a portal called Vidyalakshmi to facilitate education loans right?

Questions Worth Asking in the Upcoming Q2 FY25 Concall

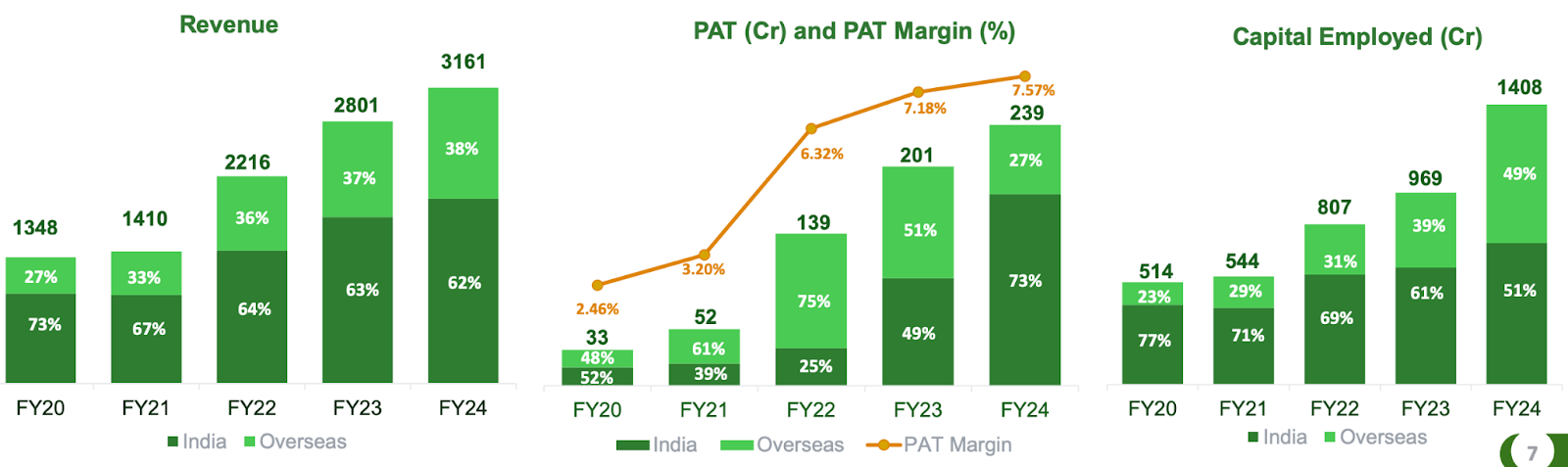

From the above graph, we can notice that while the revenue contribution from the overseas business increased from 36% in FY22 to 38% in FY24, the profit share dropped significantly from 75% to 27%, and the capital employed in overseas operations rose from 31% to 49% over the same period.

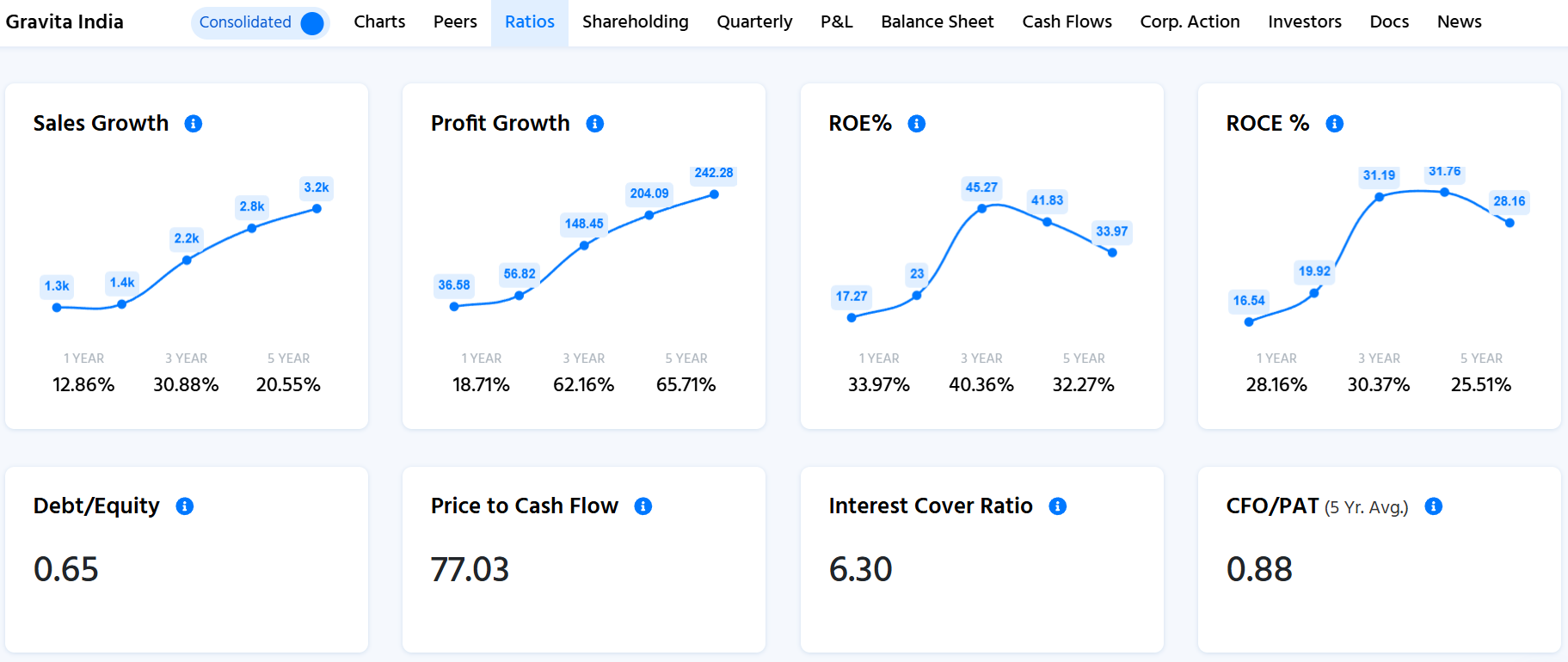

(Image Source: Finology Ticker)

From the above image of Finology Ticker, we can see that the CFO By PAT ratio is less than 1. It means the company is unable to convert its profit to cash.

Update on the New Overseas Acquisition

Gravita’s subsidiary has signed an MOU to acquire an 80% stake in a waste tyre recycling facility in Romania, which can process around 17,000 MTPA (Metric Tons Per Annum), for ₹32 crore. The remaining 20% will be owned by local partners in Romania.

This move marks Gravita’s entry into the European recycling market, significantly increasing its potential market reach, with Europe’s waste recycling industry valued at USD 155 billion in 2022.

This expansion into new regions and products is expected to be a key driver of the company’s future growth.

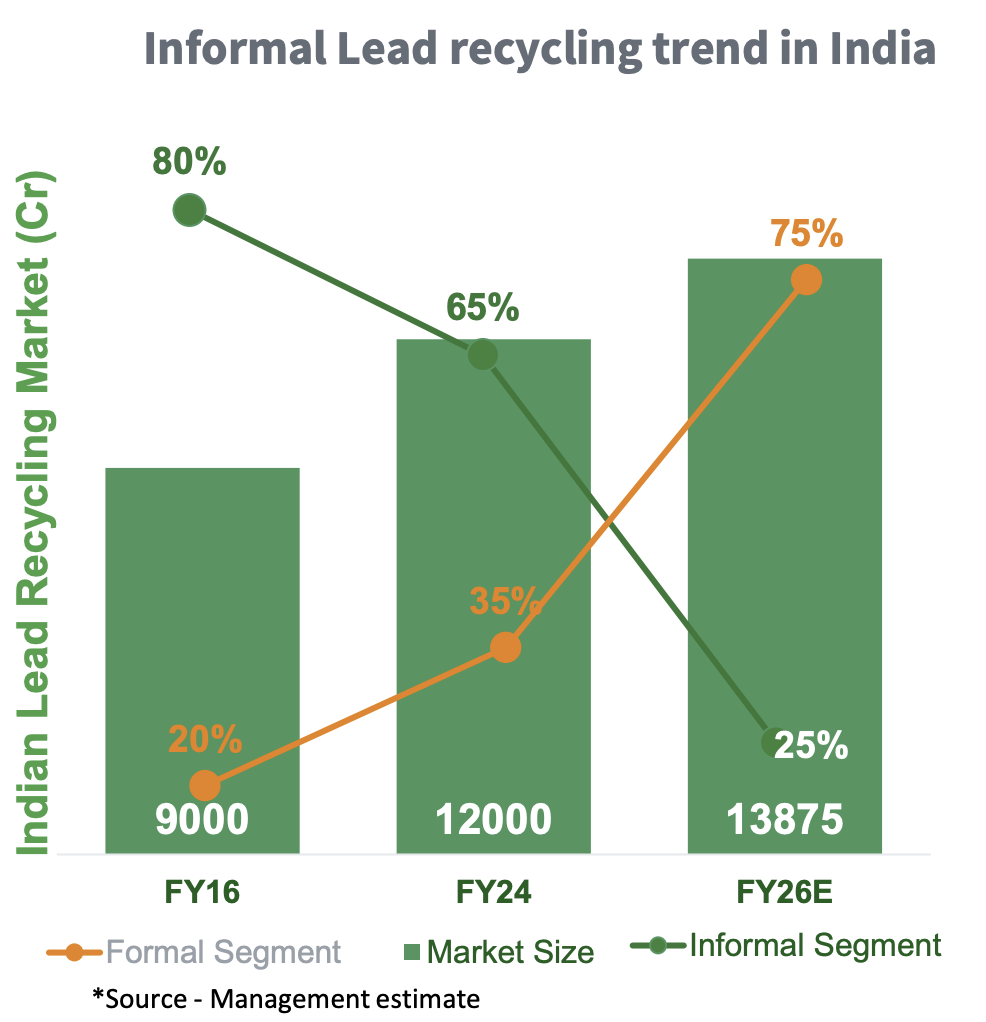

Multidecadal Tailwind in the Recycling Business

India’s battery recycling rate is just ~20%, far below the 60-80% as seen in Western countries.

Currently, 65-85% of recycling is handled by the informal sector.

However, recent regulatory changes are rapidly shifting this trend toward formal, organised players, creating a long-term earnings opportunity.

1️. Battery Waste Management Rules (BWMR): The 2022 BWMR has set the stage for formalising the industry by encouraging investments in collection networks and allowing legitimate recyclers to trade Extended Producer Responsibility (EPR) credits. This is pushing more business towards organised players.

2️. Extended Producer Responsibility (EPR): Manufacturers are now required to take responsibility for the entire lifecycle of their products, including post-consumer waste. They must collect at least 70% of their sold batteries once they reach end-of-life. This means more scrap batteries flowing into the formal channels, boosting business for organised recyclers. The mandate is expected to increase the volume for organised recyclers by 3x to 5x going forward.

The EPR rule mandates that recyclers can only recycle up to their capacity limit. The entity cannot outsource the recycling work. This mandate provides the clear reason for capacity expansion and utilisation within the industry.

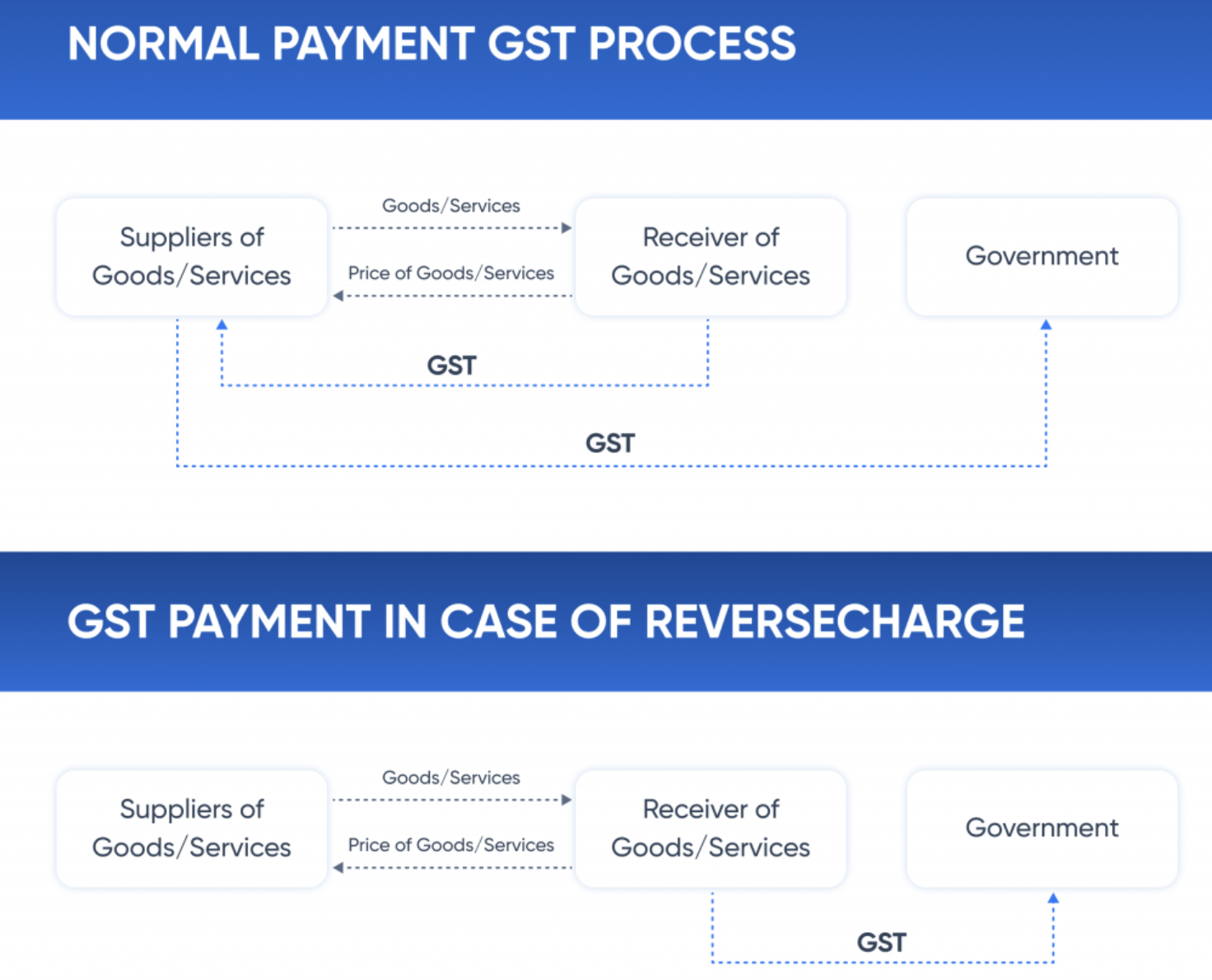

3️. Reverse Charge Mechanism (RCM): Registered recyclers are now required to pay tax on scrap, even if they buy it from unregistered suppliers. This creates a formal tracking system and is expected to reduce the dominance of unorganised players, who currently handle 65% of the market.

The introduction of the RCM is a game-changer in levelling the playing field in the lead recycling market. Shifting the responsibility for GST deduction and deposit to the scrap buyer will effectively reduce the cost advantage that unorganised players gained through GST evasion (18% GST on scrap materials). As a result, it will benefit the organised sector. In our opinion, this could be an even bigger tailwind than the BWMR rule.

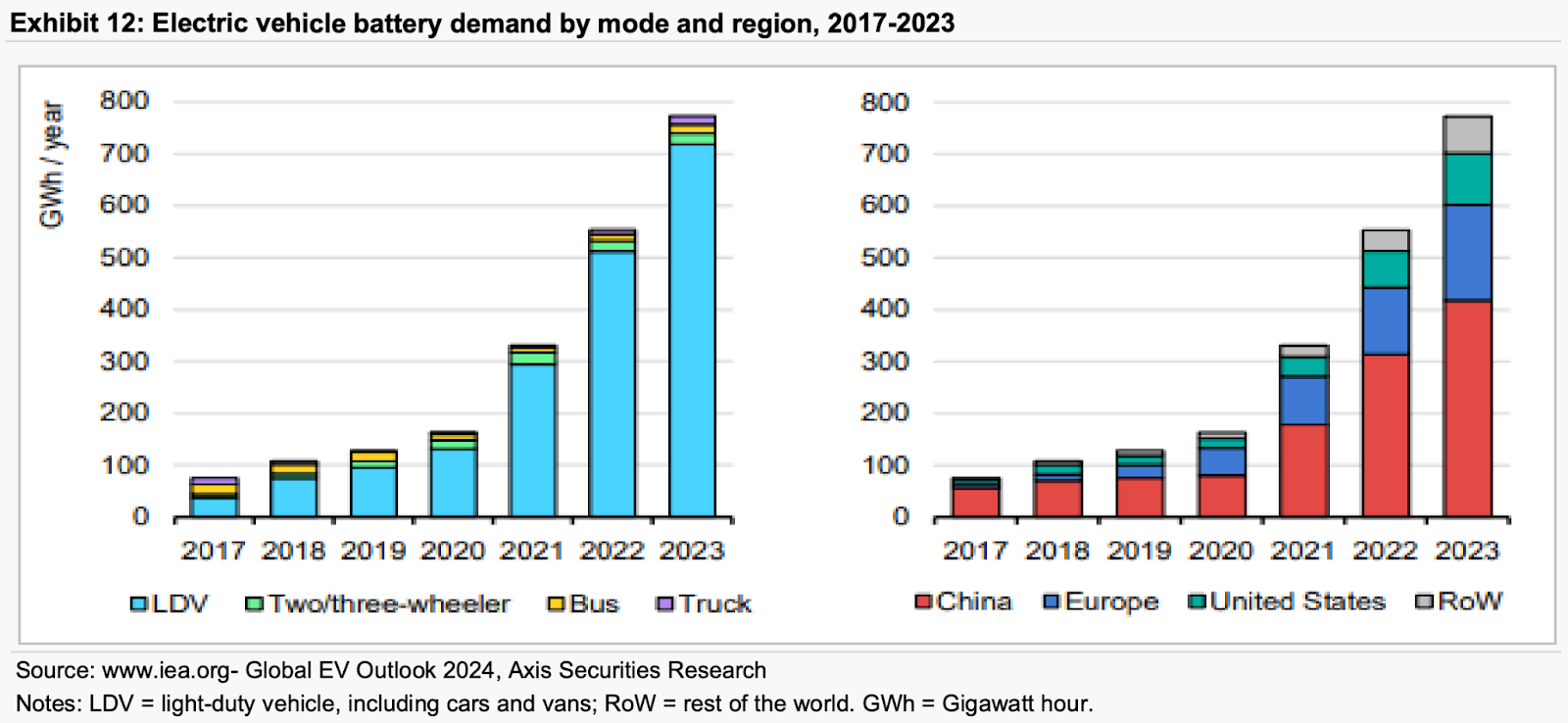

4️. EV Battery Recycling: The global EV battery recycling market is still in its early stages. However, as the first generation of EVs nears the end of its lifecycle (in about 5-8 years), India’s demand for recycling infrastructure is expected to skyrocket. While India’s lithium-ion recycling facilities are still developing, the first major wave of recycled EV batteries is projected globally by 2028-2030, and India will need to step up quickly.

5️. Vehicle Scrappage Policy: India’s Vehicle Scrappage Policy is designed to retire old, polluting vehicles, significantly boosting the battery recycling industry. As more end-of-life vehicles are scrapped, especially older models with lead-acid batteries, the recycling volume is expected to rise.

Northern Arc has bad underwriting standards, they have partnered with Uni which basically provides credit for 10-15 days interest free but later charges high interest with many hidden charges, literally every friend of mine has got credit from them with no income proof, also they have grown coz of high incentives for referrals.

No they wont, the SM REIT will raise funds separately.

The benefit to EFC will be that the properties purchased by SM REIT will be managed by EFC at similar margins, but no risk of landlords/property availability as the SM REIT becomes the landlord.

For companies in capital goods space there is always lumpiness in order flow and execution which impacts the quarterly numbers, more so of small companies who have high portfolio concentration in a single product. So we won’t see a smooth linear increase in yoy numbers. From that perspective inter-quarter variations in PAT and margins shouldn’t be worrying unless there is dramatic drop or some negative commentary from the management.

Overall outlook for the transformer sector in India is still positive and Voltamp management (a very conservative one) has maintained that. They have announced CAPEX for capacity expansion and knowing their disciplined execution they wont do that just to please the market.

I believe stock has run a lot, currently quoting 2x its historical valuations so these minor disappointments in numbers are always expected to cause a decent 20-30% corrections in stock prices.

Disc- Invested and adding at corrections

MFI AUM is 20% of the entire book, out of this 11% is through direct lending.

This stress in MFI & Vehicle finance is going to be there for 3-4 quarters

Indusind is also going to face tough quarters due to vehicle finance NPAs

As per my understanding, this is price adjustment …which is good some time

Wait for Q2 result…

As per 27.11.2023 Concall :

Revenue growth for FY24, 90Cr+ (Actual reported revenue 90.43Cr) …Matched with statement

FY25: Rs 135-150 Cr with EBITDA margin 36% + …Watch this Number

The actual problem of the company ” Receivables / Collection “

Welcome to valuepickr. Liked your first post very much.

Well, I think one might need to rethink this at some point of time or other (I am thinking loud here and also myself learning as I think and type. Also, I am speaking in general below so pls forgive or ignore the extreme events mentioned as we have to consider those when we think of insurance).

Life insurance is ideally not to cover immediate expenses of dependent family once they are gone but rather to ensure that the lifestyle of the dependents are not negatively impacted over the long term once the gone member’s income is taken away from the picture. Considering above, I think only a person/family who has enough other assets to ensure that the lifestyle, including inflation over long term, is not impacted may not need an insurance. Wife working & non-dependent parents are great to have and would ensure that financial survival is not impacted at all but would mean extra burden on the surviving members.

Another aspect to consider is, what if both earning members are gone is any unforeseen event. Then the non-earning or minor surviving members would definitely face huge financial stress.

Coming to health insurance, that again in worst case scenario, the earning members income will be in huge stress under unforeseen events. However, I feel taking a small health insurance policy is not of much use. The insured sum should be as big and comprehensive that if someone would have to shell that out of pocket, it would mean a massive future lifestyle impacting change. Problem with health insurance policies is that such big sum policies are extremely expensive upfront costs. In case of Life, the term insurance of big sum insured, I think is still at a reasonable/manageable cost. (I may be wrong here).

So, I think majority of people would need insurance. Its only that either they are fortunate enough to not have adverse events or they do not know it still that they need insurance. Problem is the upfront costs.

Can you pls mention more details/benefits about NPS tier 2 that you prefer it as part of your debt/hybrid portfolio?

Do keep writing such holistic/strategic posts like your first one. Good to see such structure, thoughts and vision.