Appreciate it, but I did read the concall.

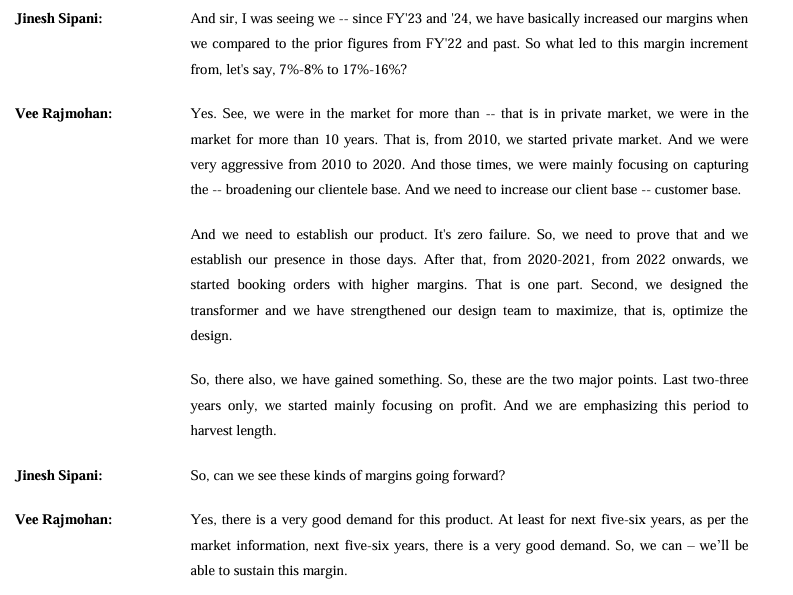

Just wanted to have a bit more clarity , on what exactly lead to the increase in the margin was it shift in product, if yes which type of transformer.

Posts tagged Value Pickr

Supreme Power Equipment Limited (16-06-2024)

Corporate Fraud/Misdemeanor – Public Domain – Global lessons (16-06-2024)

Promoter holding is 48% and in the history of the co. promoter only sold on 21st and 22nd march 2024 you show me any other day of selling I will gift you 1 crore !

But people like you aren’t smart enough to be in markets find some other job.

Atirek portfolio (16-06-2024)

Sold NH( Narayana Hrudayalaya Ltd)

I sold it after going through the Q4FY24 concall at around 1200.

Reasons – operating deleverage might play in coming 2-3 quarters.

- They will use only money earned in India for Indian capex(as they can not bring money earned in the Cayman to India due to tax issues). They might take loans up to 300-400 cr(1000 capex- 300 cr cash in India – 400 cr estimated profit this year in India), decreasing the net profit by 30 – 40 cr.

- Employee cost can become high going forward due to backlog as told in the Q4Fy24 concall.

- New facility of cayman will come in operation in Q2FY25 and depreciation and fixed cost will hit the balance sheet. My estimation is near to 40 cr in depreciation will get deducted from the PnL. As the capex is of category greenfield in the same city and it is in the city centre, it might take least 1 year to breakeven, till then it will decrease the profit in PnL(operating deleverage). The operating deleverage might be too high, it seems in the initial few quarters.

- The growth in revenue YoY is not coming even if the Northern Hospitals issue that they faced last quarter is gone(concall – Q4FY24). Considering they increase their prices by at least 5 percent on 1st of January every year, the YoY revenue increase of 5 percent has not been satisfactory.

I will judge the company again after the Q2FY25 results or if growth comes again in Q1FY24.

The reason why I looked at this company concall in detail was that, I studied it after I saw it being added in axis small cap fund as their top holdings and due to SOIC. But Axis small cap fund started selling the NH since few months, and I was looking for reasons.

Mutual fund updates

I could not find many stocks and hence have deployed the money that I got by selling stocks in the last few months in the Parag Parikh tax saver mutual fund. I have kept some cash(4.5% of net worth), to take a position in one stock if anything good arises.

Stock buying update

Added some units of Neuland.

Mutual funds have been adding SRF recently, the Mirae mutual funds which sold the SRF in April, added it back in May. Need to understand the reasons.

Supreme Power Equipment Limited (16-06-2024)

PLease find the answer to your question in the transcript.

Som Distilleries and Breweries (16-06-2024)

Saw this few days back…Is Company responsible in such or some cases like these? Power cool beer is owned by SOM distilleries which is shown in this reel.

Maharashtra seamless-a value plus cyclical play (16-06-2024)

Here is an improved version of your post with better structuring, formatting, and language:

Title: In-Depth Analysis of the Steel Pipe Industry

This weekend, I spent time researching the concall transcripts of major players in the steel pipe manufacturing sector, including Man Industries, Ratnamani Industries, Venus Pipes, Jindal Saw, and Maharashtra Seamless. After going through the transcripts, here are my key observations and analysis:

Observations:

- The industry is experiencing a strong tailwind, with most companies announcing significantCapEx plans and providing revenue growth guidance of over 20%.

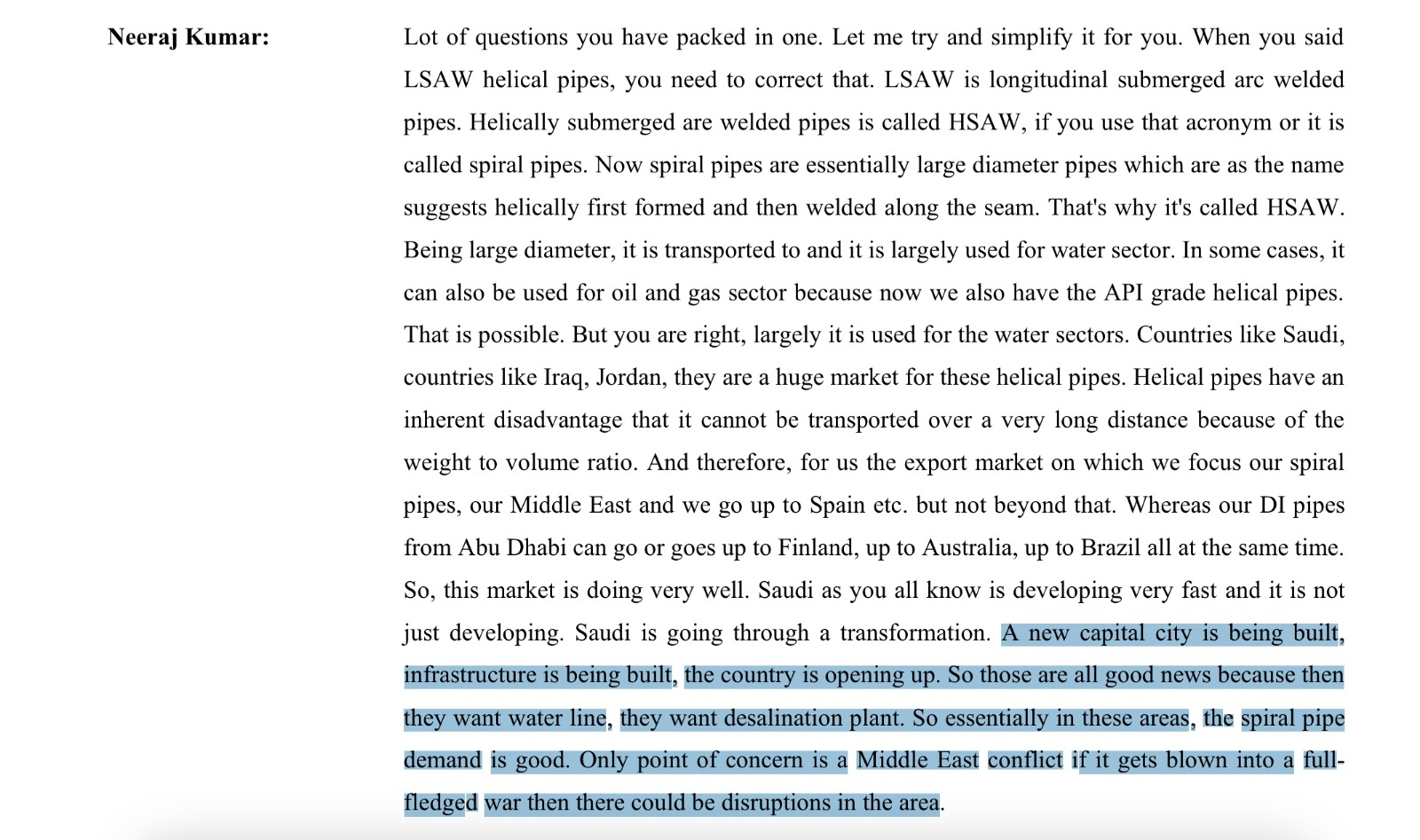

- The major products manufactured in this sector include ERW (Electric Resistance Welded), Seamless, LSAW (Longitudinal Submerged Arc Welded), HSAW (Helical Submerged Arc Welded), and Ductile pipes. @jeewangarg has already provided a detailed list of which player manufactures which product.

- Man Industries is undertaking CapEx in ERW and Seamless segments. Additionally, they are opening a new plant in Saudi Arabia.

- Seamless pipes command higher margins (around 18%), while LSAW, HSAW, and Ductile pipes have lower margins (around 10%).

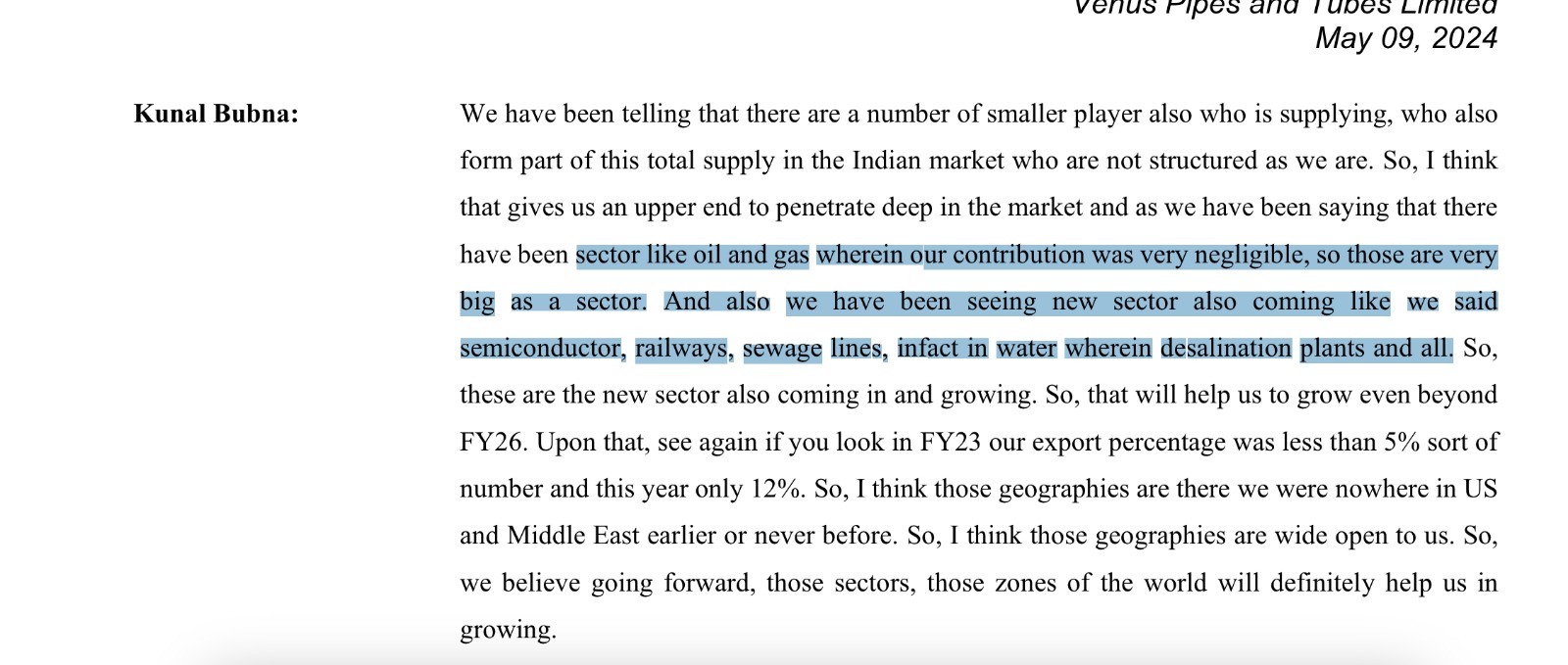

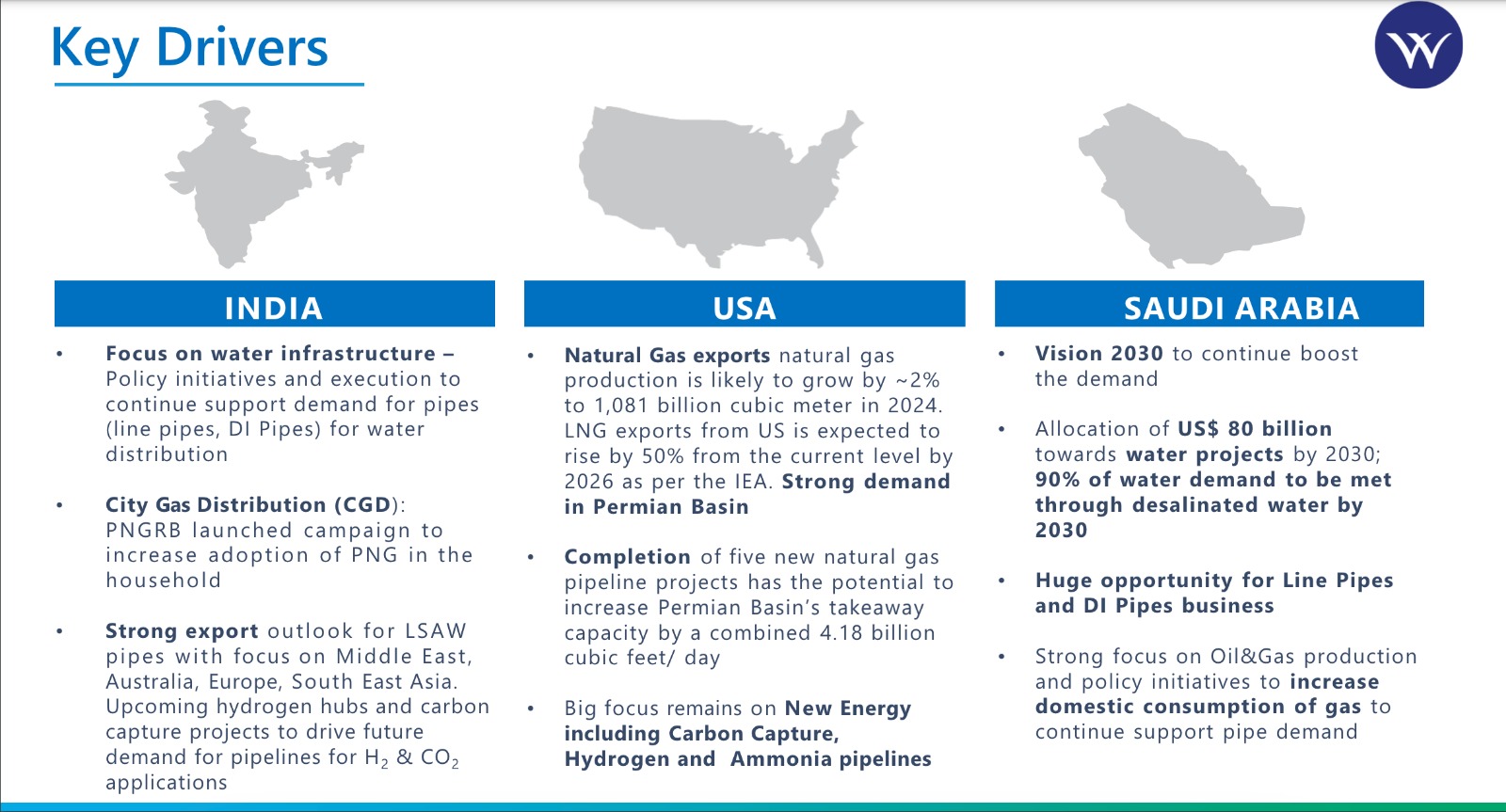

- The demand for water transportation pipes is peaking in India, while the demand for oil and natural gas pipes (LSAW & HSAW) is increasing in Saudi Arabia. Globally, pipes for the oil and gas sector have higher demand compared to water pipes.

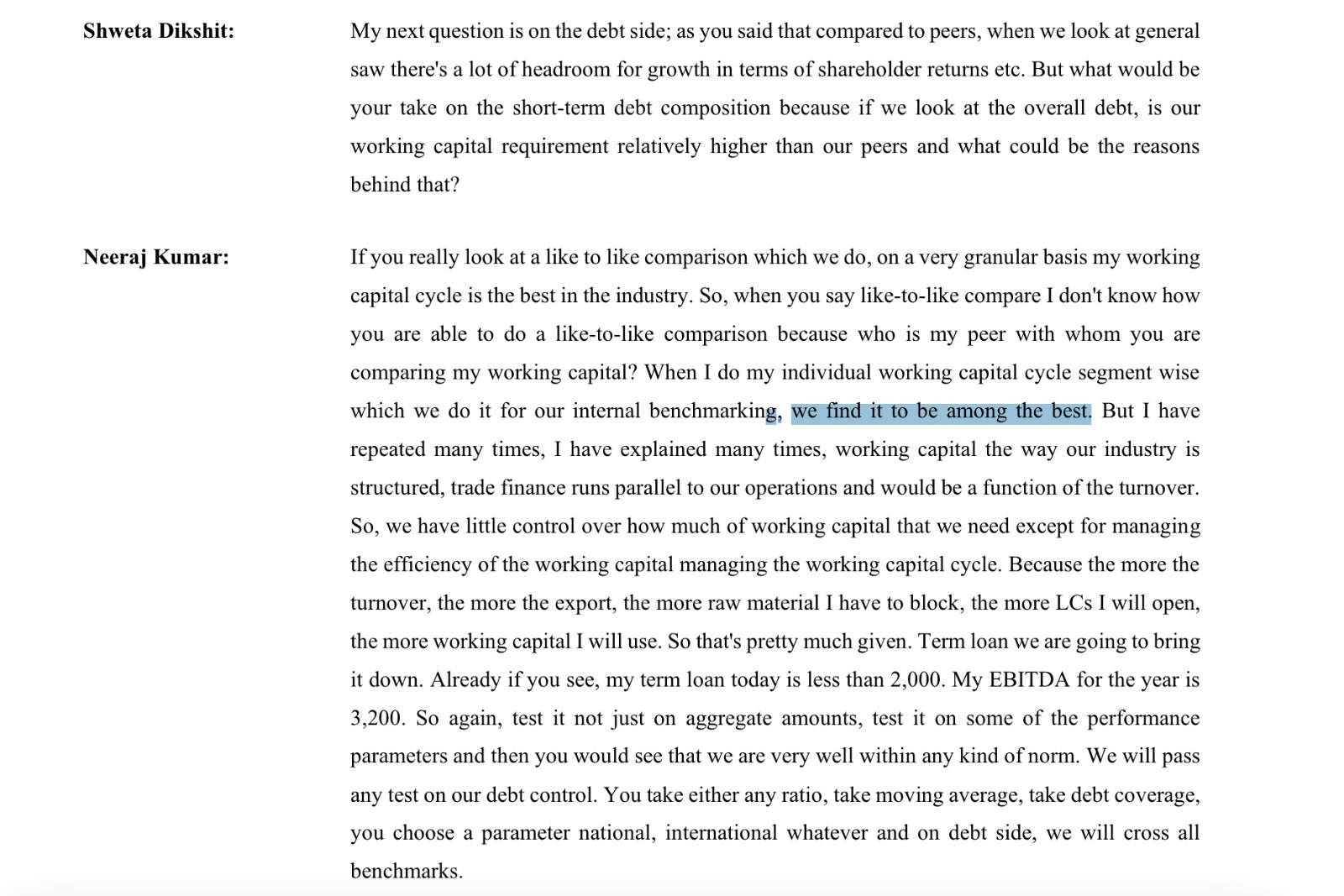

- Maharashtra Seamless is the only debt-free company among its peers and has no plans to take on debt for further expansion.

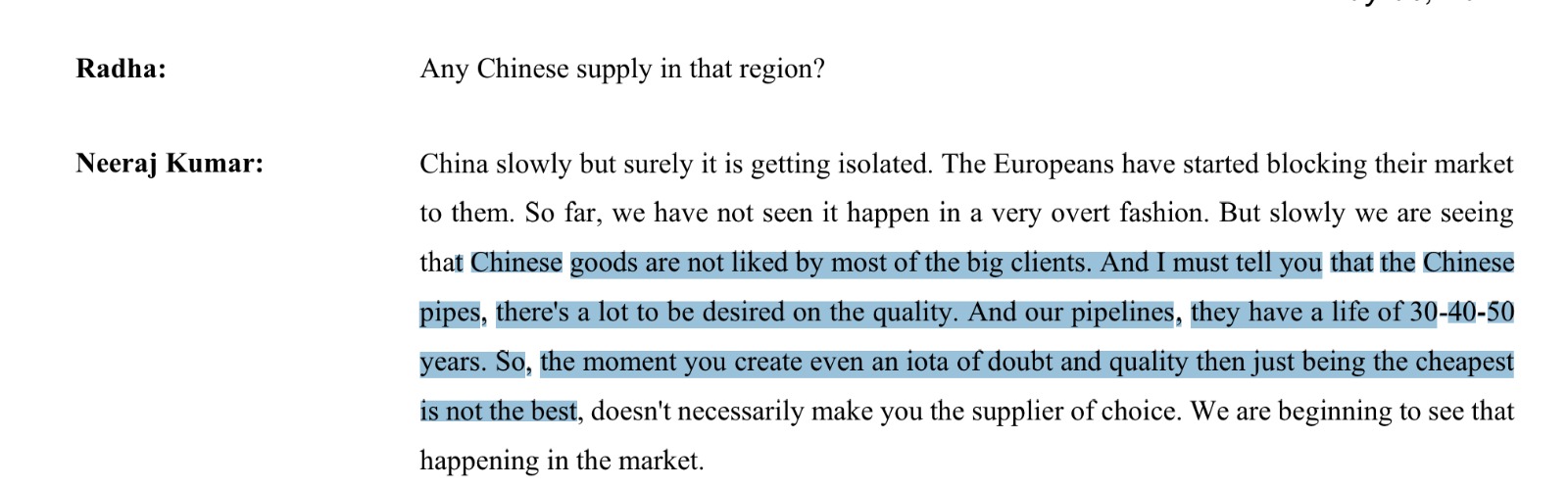

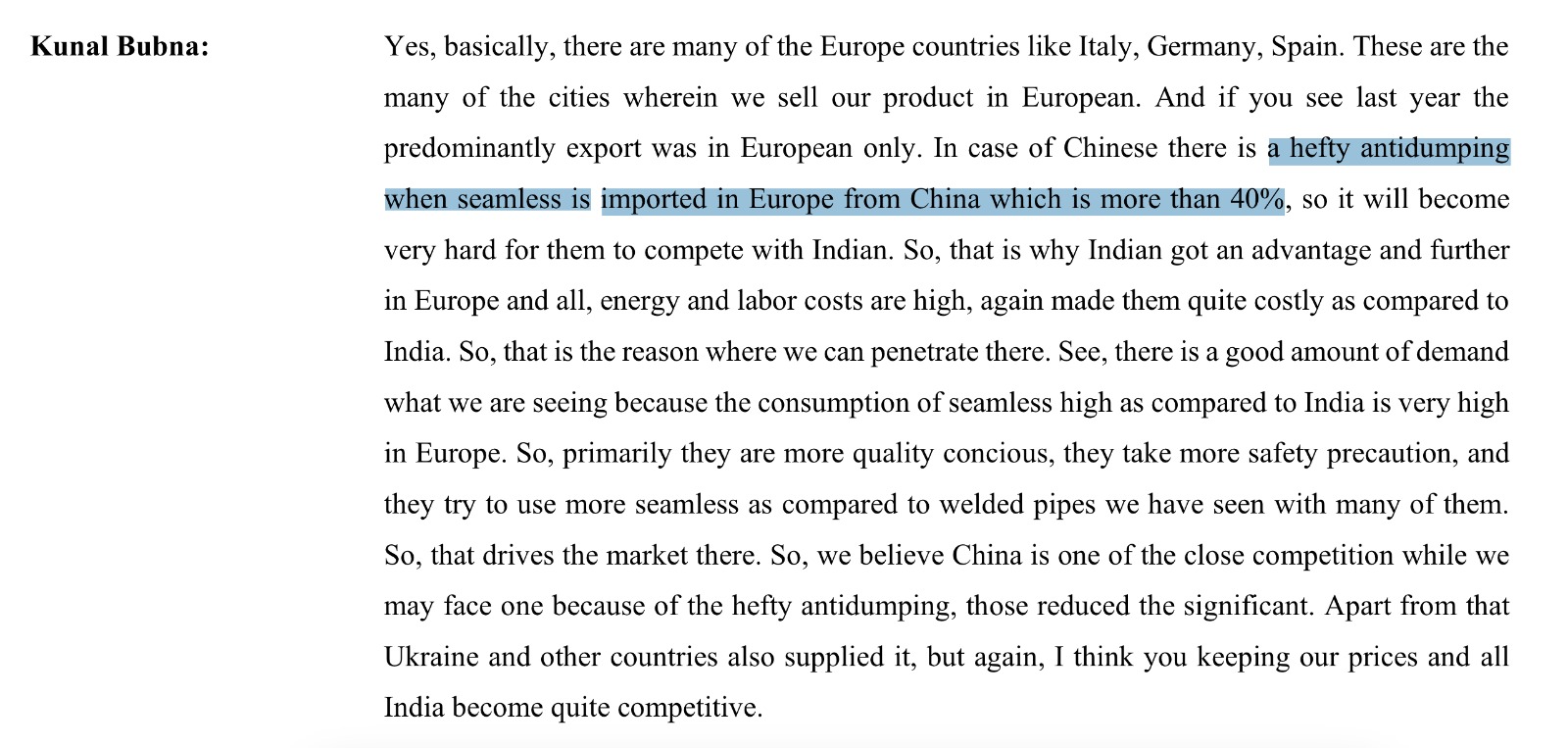

- Chinese companies currently hold around 54% market share in this space, while India’s share is only 7-8% (as per Venus Pipes’ DRHP). Additionally, there is a growing trend of buyers avoiding Chinese companies, which could provide substantial growth opportunities for Indian players if this continues.

Points for Discussion:

- With multiple players undertaking capacity expansions, when can we expect oversaturation in the industry?

- Why did Maharashtra Seamless witness a decline in revenue, even as its peers reported exceptional growth? The concall reason of not compromising on margins was unclear.

- What is the expected trend for steel prices, a key raw material for this industry?

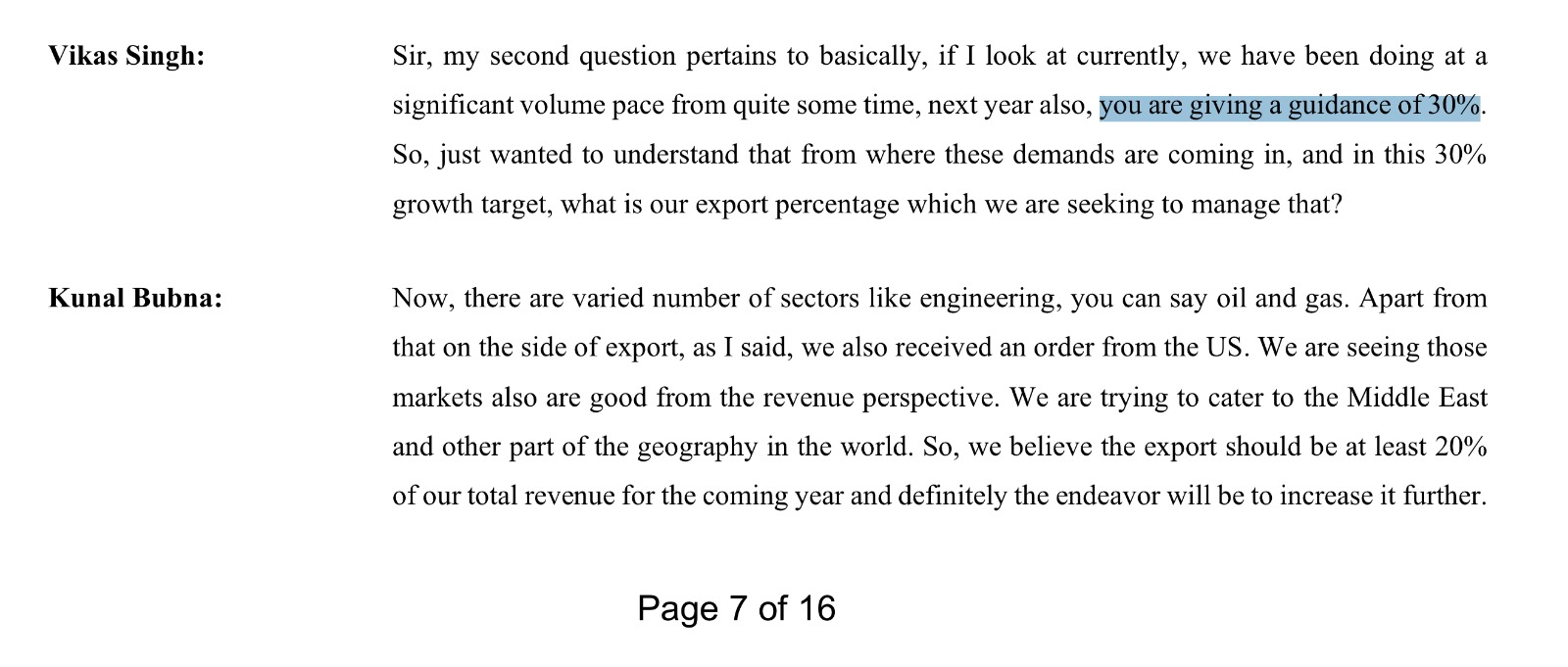

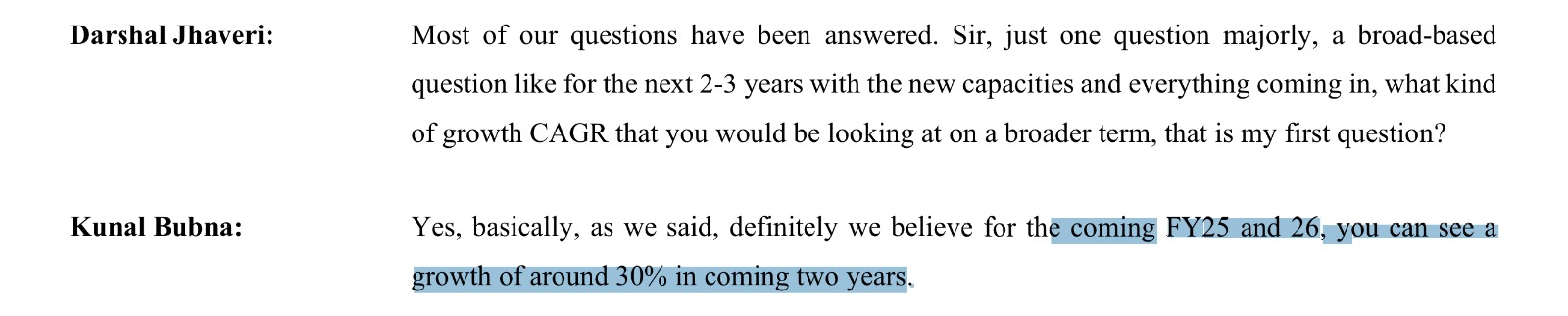

I have attached some interesting excerpts from the concall transcripts across the sector. More will be shared in subsequent threads.

Supreme Power Equipment Limited (16-06-2024)

From available public data:

The Operating Profit Margin (OPM) of Supreme Power Equipment Ltd. increased from 7.4% to 17.4% in recent years due to several factors:

-

Improved Gross Margin: The company’s gross margin increased from 11.62% to 14.20% over the same period, indicating higher profitability from its core operations[3].

-

Reduced Operating Expenses: The company’s operating expenses as a percentage of revenue decreased from 85.38% to 74.91% during the same period, indicating better cost management and efficiency[3].

-

Increased Revenue: The company’s revenue increased significantly, from ₹113.59 crore to ₹14.00 crore, over the same period, indicating higher sales and revenue growth[2].

-

Improved Return on Capital Employed (ROCE): The company’s ROCE increased from 29.16% to 73.32% during the same period, indicating better utilization of capital and higher returns on investments[1].

-

Increased Net Profit Margin: The company’s net profit margin increased from 1.11% to 14.32% during the same period, indicating higher profitability from its operations[1].

These factors collectively contributed to the significant increase in the company’s OPM from 7.4% to 17.4% over the recent years.

Citations:

[1] https://www.indmoney.com/stocks/supreme-power-equipment-ltd-share-price

[2] Supreme Power Equip Share Price Today (14 Jun, 2024), Supreme Power Equipment Stock Price (₹ 256.65) Live NSE/BSE, Supreme Power Equip Shares

[3] Supreme Power Equipment Ltd. | Tijori Finance

[4] Supreme Power Equipment Ltd. Live Share Price, Stock Analysis and Price Estimates

Supreme Power Equipment Limited (16-06-2024)

Could you help me on the reason for the expansion of margin from merely 7-8 % to 16-17%.

I would appreciate your input on this.