Posts tagged Value Pickr

Tinna rubber – recycling a rubbery growth path (11-06-2024)

That is because of small equity capital and promoters hold the max 73.5% holding, leaving less on the table for FIIs and MFs.

Delta Corp – A huge but risky opportunity (11-06-2024)

Any recent views on Delta? Goa was full of tourists when I visited last week despite off season and am sure Casinos business will be doing very well. If there is a turnaround, does valuation appears reasonable to enter? Any relief possible on GST for online gaming? Appreciate thoughts…

Anlon Technology Solutions (11-06-2024)

Brief Business Overview:

• The Company specializes in providing end-to-end engineering services tailored for aviation infrastructure including firefighting trucks, runway rubber removal machines, friction testing machines, runway sweeping machines, spare parts and other equipments.

• They perform sourcing, supervising, quality control, transportation, and installation of equipments for airports (80% of revenue), government, municipalities and refineries (20% of revenues)

• They have long term collaborations with leading OEMs worldwide and deliver bespoke solutions that meet the needs of their clients.

Currently revenue source is as follows:

Commission (They procure orders from its clients majorly airports and other refineries, municipalities etc. for its suppliers Rosenbauer, Bucher Municipal, Winter Grun etc. and charges a commission on it. Operating margins through this source are the lowest.) – 15%;

Spare parts (they source spare parts and provide installation services for the same) – 45%;

AMC (The Company provides maintenance services for vehicles and other services provided to airports.) – 40%.

This mix is expected to change drastically over the next 2 years as the assembly line of vehicles starts

Why you should look at this Company

• In-house assembly of vehicles:

Up until now, Anlon was an exclusive distributor for its OEMs in India. It used to earn a commission on its sales and then an annuity revenue in the form of AMC charges for those vehicles. What changed for the Company in May 2020 was the announcement of Atmanirbhar Bharat where the government announced all global tenders below Rs 200 would not be allowed for government procurement. As most of the vehicles that Anlon was supplying in India were high value-low volume they were all below Rs 200 cr so this caused a problem for the Company moving forward.

Since Anlon has been the sole AMC player for these vehicles in India for ~15 years, it was able to convince its European counterparts to build assembly lines in India for those vehicles and sell them as Made in India (similar to what is happening with iPhones).

The Company raised Rs 15 cr in its IPO to set up its assembly unit in Bengaluru that was inaugurated at the end of February 2024 and production is expected to start by June 2024.

The vehicles rolled out from this unit are expected to be about 25% cheaper as compared to the CBUs that were being imported till now. The vehicles will now be indigenized for eg. the chassis will be sourced from Bharat Benz, Ashok Leyland etc. though the core or critical components will still be imported from Europe/USA.

• Industry dynamics:

By 2030, India is projected to have about 230-240 airports up from 148 now. With most of the metro/bigger cities in India already being well-connected by air, major growth is expected to come from tier 2 towns and below. Anlon also acts as a Consultant to its clients and will be able to customise the vehicles will the requirements of each airport

India has an aircraft fleet size of ~750 currently that is projected to grow to 1,200-1,400 by 2030

Air passenger traffic is expected to grow to 42 cr by 2030 up from 14.5 cr today

• Long term relation with suppliers provides export opportunities:

Anlon has been the exclusive supplier for Rosenbauer, Bucher Municipal, Winter Grun etc. in India for over a decade and a half now thereby maintaining excellent relations with the OEMs. Anlon prefers keeping its OEM network consolidated and working only with the best. Over the next 12 months Anlon has an opportunity to showcase its skills and expertise by assembling these vehicles in India with similar quality standards as its European OEMs would have. If they are able to prove their mettle as a manufacturer, this presents an opportunity to Anlon to become an export hub for these vehicles in the future.

QIP

The Company recently raised Rs 25 cr from investors at a price of Rs 382.

The Company holds orders received in Feb 2024 from Delhi and Cohin airports. They also received an order from AAI worth 22 cr to be supplied during FY25 (to put things in perspective their FY24 revenue from services stood at Rs 35 cr)

Risks

➢ Airport infrastructure growth in India slows down leading to fewer number of tenders for these vehciles.

➢ Anlon is not able to assemble these vehicles at the same quality as its European OEMs.

Management

➢ Unnikrishnan Nair P M (Chairman & MD)

He is the promoter of the company. He holds a Bachelor’s degree in Engineering – Mechanical from Bangalore University. He has more than 28 years of experience in the industry. At present, he is responsible for the overall management, day to day affairs and is the guiding force behind the strategic decisions of the Company. Hearing him on the concall, he seems very focused on quality of his products rather than just chasing growth numbers

Link to IP – https://nsearchives.nseindia.com/corporate/ANLON_28052024113647_IP.pdf

Link to 1st earnings concall May 2024 – https://nsearchives.nseindia.com/corporate/ANLON_30052024131700_Transcript.pdf

Invest in upcoming semiconductor industry (11-06-2024)

The Indian government has approved multiple semiconductor fabrication, OSAT and packaging plants under its US 10 billion dollars subsidized scheme called India Semiconductor Mission. A few more proposals, like the one by Zoho, are under scrutiny for approval. India is about to become the fifth largest exporter of semiconductors in a few years and 2.5-3 lacs skilled semiconductor jobs are to be created by 2027. There will be indirect job creation as well. How and where do I make investments to benefit from the upcoming rise in the semiconductor industry of India?

KEI Industries Ltd – A consistent performer over the last decade (11-06-2024)

@Parakh You are right…But many times stocks move so fast, specially momentum stocks…that they are more than 30% above its 30 weekly EMA ( 150 D Ema), in that case even if you apply trailing stop losses just below 30 week EMA, you may end up giving more than 30% of your gains…Can you finetune this trailing stop loss better to keep the gains?

SBI Cards & Payment Services Limited (11-06-2024)

Sort of you are correct

KEI Industries Ltd – A consistent performer over the last decade (11-06-2024)

Book: Stan Weinstein’s Secrets For Profiting in Bull and Bear Markets

Chapter: 6

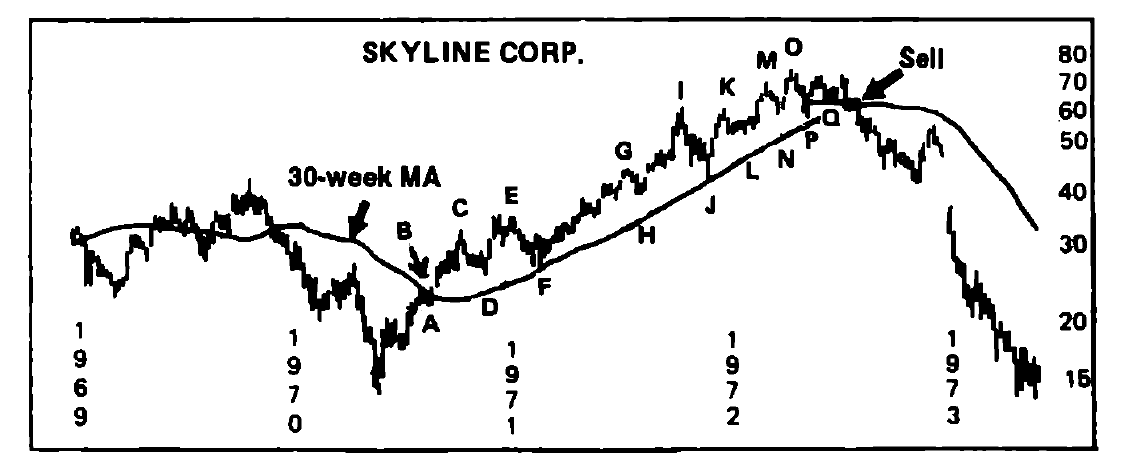

Relevant concept: A stock is said to move from stage 2 to stage 3 when the current market price moves below 150 DEMA (per Stan Weinstein) (200 DEMA in more contemporary literature). Since strong stocks seldom cross this threshold, you can put a stop at this threshold, which if crossed, closes the position at profit. As the stock climbs up on the price chart, the sell stop needs to be accordingly needs to be moved up, just below the 200 DEMA. This needs to be done on a regular basis. It can be weekly or max fortnightly. As and when the stock would enter stage 3 (and it can happen on low volume), you will be safely exited. Here’s a pictorial representation of the same (From Stan’s book):

The dark line is 150 DEMA

I use a variation of this exit system in my fresh buys, with the aim of capital preservation. Once a stock has given me around 15% profit, I usually place a safety GTT, Rs. 2 above my breakeven price. That way I remain protected from volatility, like we saw on June 4, 2024. Yes, it can sometimes throw you off of positions which may quickly recover, but it will almost always preserve your initial capital.