Jindal Stainless’ defence arm rifle gets army clearance | India Infoline

Posts tagged Value Pickr

Poonawalla Fincorp formerly Magma Fincorp (10-06-2024)

Why is this falling? Any major event or PE adjustment before Bajaj IPO?

Royal Orchid Hotels – Available at good valuation! (10-06-2024)

May be partly also due to governance concerns. Google for governance issues and study the past Annual Reports of the company. There are several litigations, auditor qualifications, adverse remarks, write offs, defaults, etc. Company was a defaulter and went through CDR mechanism. The promoters have reduced their stake over the years.

Borosil Limited (10-06-2024)

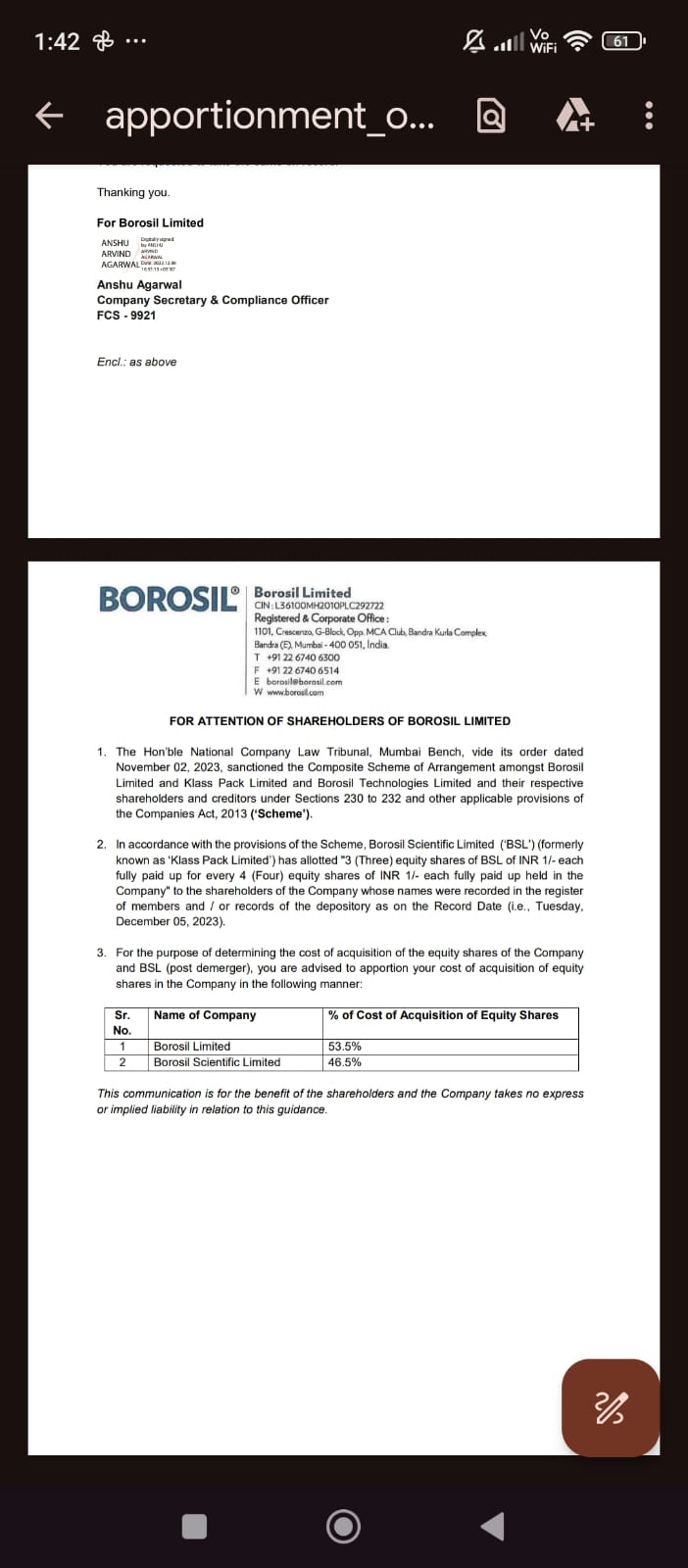

Thats the basis for price adjustment as per me, in the past I also got shares of Borosil Renewables and they have been at 0 acquisition cost, because as an investor we receive shares without any cost price…but you can consult your CA for right advice…

Focus Lighting & Fixtures Limited (SME) (10-06-2024)

Focus Lighting Q4 FY24 concall notes:

The company is a pioneer in many lighting fixtures. Many of its products have patents with products that are disruptive with superior tech. Its products are one of a kind, with no other company worldwide providing such products (as claimed by the management).

Take a look at their concall presentation conducted on Zoom in which the management has explained their products & initiatives in the first 35 mins – Focus Lighting Q4 FY24 Concall presentation

Financial performance

Stable performance with 60 Crs topline – almost same as last 2Q, 10 Crs bottom line – same as last 3Q. Expected EBITDA margins of 22%. No surprises here.

Growth – Trade division, new products

Retail – The company invests a lot in R&D, innovation & tech. All their innovative products & designs are patented. For ex. they have been able to reduce no of fixtures needed for retail stores by more than 25% using innovative designs & tech. This will lead to lower electricity & air conditioning load for store operators. Using better lighting fixtures with less light spillage. They serve customers like Mercedes, big auto showrooms, IKEA, Reliance retail among others.

Home & Infra – Both divisions to experience rapid growth. The Infra division will see good traction as they bid for more projects nationwide. Approval has been given for light fixtures for Vande Bharat trains from railways. They recently won the bid for Navi Mumbai Airport.

Trade – This is a new division they plan on starting. Plans to enter the high volume, low-value segment of manufacturing for big OEMs & also begin to create a brand from individual sales. They want to manufacture differentiated products for OEMs which score high on sustainability by reducing weight by eliminating aluminium & reducing production time. They expect blended margins to be stable. Chinese imports do not seem to be a big problem as their products are differentiated & not basic commodity nature.

Experience centers & Exports – They plan to set up experience centers in the Middle East & India to increase brand & product visibility. Middle East is a booming market with good opportunities.

Guidance

Guiding for 15-30% sales growth, more towards the upper side. ~20% OPM’s.

There is some elongation in the receivables days due to infra projects. The company is also investing in CapEx for future growth, as seen in CWIP of 19 Cr upon Net Block of 21 Cr. I don’t know the nature of this capex, whether it’s a new facility for the trade division, new machines for increasing production or the new experience centers they were planning to set up.

Borosil Limited (10-06-2024)

Hi

As per my understanding we are supposed to take 46.5% of the initial buy average price.

Rural Elect Corp (10-06-2024)

REC shows Strong performance in multiple areas with strong Institutional holdings showing uptrend.

Discl: Invested from lower level with 4X returns within 2 years, apart from hefty dividend yield. May Be biased.Not a buy or sell recommendation. PSU stock carries risks and subject to Govt policy changes resulting in to volatility. Also, PSU stocks may not show qoq sequential growth. The quarterly performance may be lumpy.

Poddar Pigments (10-06-2024)

hey, anyone with updated views on this? Thanks!

Sunshield Chemicals Ltd (10-06-2024)

yasho industries and there is another one that is unlisted and smaller in size/capacity

TCI Express – Logistics Sector niche player (10-06-2024)

Delhivery_ET prime.pdf (1.9 MB)

An article to be read. Is Delhivery’s aggressive pricing strategy impacting the express logistics business? If one reads TCI Express’s concall over the last 6 qtrs, one can see their inconsistency in forecasts. Either they don’t want to acknowledge that competition is eating into the available pie or they are extremely rigid about their strategy in pricing.

Disc: Invested from higher levels