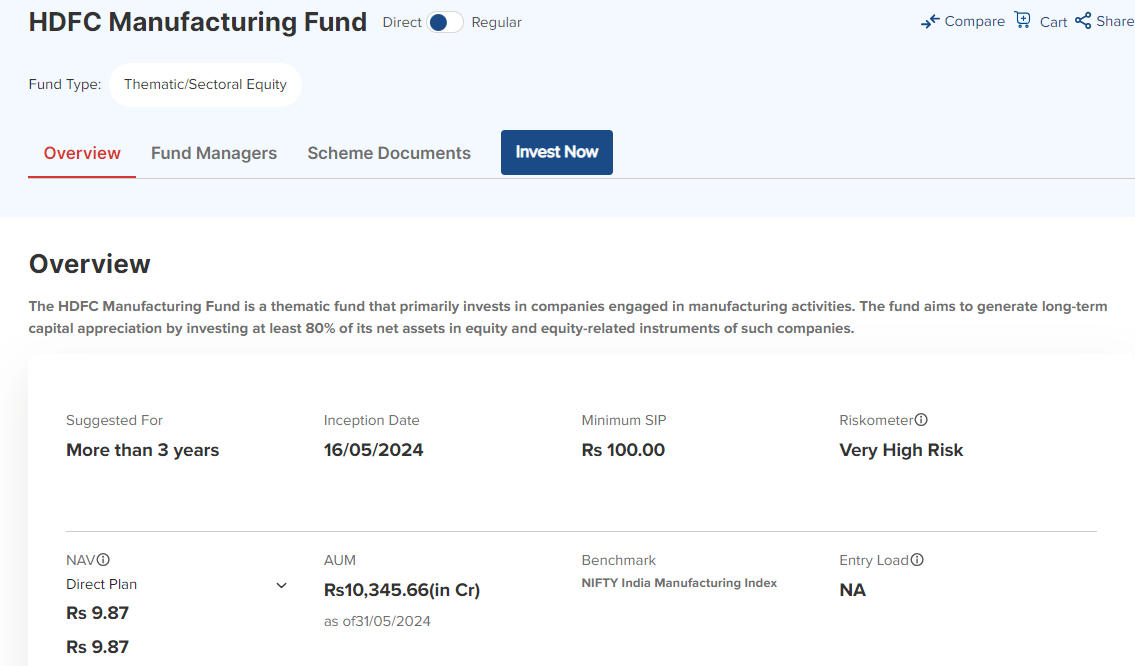

HDFC Manufacturing fund has indeed garnered 10000 crores in the NFO

https://www.hdfcfund.com/product-solutions/overview/hdfc-manufacturing-fund/direct

HDFC Manufacturing fund has indeed garnered 10000 crores in the NFO

https://www.hdfcfund.com/product-solutions/overview/hdfc-manufacturing-fund/direct

Super disappointed with election results .BJP drawing blank in TN. Annamalai contested from my constituency and he lost. This person having been very vocal about the rampant corruption in the current government and still got nothing to show in return. Poor guy gave so much time with his health and personal life taking back seat. I was taking his victory for granted. He deserved much better. Thank god I’m not in a profession where in the result is left to the whims and fancy of the people (say like movies and politics)

Enrolled for a 10k run in September. hope to breach the 70 minute mark.

how much more pain ?

Hey do you know if there any issues with IRB invit management or with the assets they own? The price has been falling more than usual in the past few days and i was wondering why

Agree but market wasn’t pricing in drop in oil prices post OPEC decision to pump more. Both ONGC and OIL were bafflingly up 8% on Monday (post exit-poll) even though globally oil stocks were down. So fall yesterday and today is now more of a reality check. If oil prices come down to 70 range, earnings will get seriously impacted for both the companies (especially when there is zero to negative volume upside for them).

I am also feeling sad as i also have major holding of pf into zen, but the harsh realty is that NDA government will face lot of restriction in spending into renewable, defense etc. and i see major spending into other sectors / freebees so surely sector rotation will happen, so it will be difficult for zen to get domestic order and de rating of PE will happen if no new order received. Second order of 700cr from govt may get cancel . So eventually if we consider best case 30-40 PE this sector will get, if we consider best case if order dont get cancel 900cr sales 25 EPS 30*25=750 rs after 1 year.

Technically 890 is major support for the stock & the way selling order are there it will break and next major support is at 800.

Hope is Budget if government continues its focus into Defense sector & we see major portfolio with BJP.

We need to differentiate between valuations linked to earnings and P/E premium given by the market due to external factors. I think now that the latter has disappeared we’ll have to see how much valuations can be sustained by earnings which I feel will now moderate due to increasing competition (acknowledged by management in the last concall) and uncertainty over demand trajectory (both overseas and domestic).

I still maintain my previous position that all future prospects are priced in already into the counter and earning growth has peaked (which explains low p/e).

That said stock may still give decent return but I’m not comfortable with risk and reward.

A large number of industries in US (including Green energy) are facing the effects of sky high interest rates. Incremental spending has simply collapsed to only essentials… Unless the interest rates start easing in US, there wont be any major movement on new Clean Energy projects which means Bloom’s order book will be weak which results into a weaker order book for MTAR. Besides that another near term uncertainty will be US elections…If Trump wins, will he set aside Biden policies promoting green energy? That may also impact clean energy spend.

Just my 2 cents. MTAR will need a lot of patience

Disclaimer: Invested

When the bridge comes we will cross over.

Hello Stage !

are we into “side-way” situation or deep correction has started ?..All my darts were spot on till now.![]() …“abhi ankh pe andhere a gaye he, bhage ya ruke…bhage to konsi aur bhage”

…“abhi ankh pe andhere a gaye he, bhage ya ruke…bhage to konsi aur bhage”