Now de rating of this script will start

Posts tagged Value Pickr

PMS (Portfolio Management Service) fee deduction for income tax calculation (04-06-2024)

I was wondering what is the correct way to claim the PMS fee as a deduction as part of filing taxes. should it be deducted from the overall capital gains (short term or long term?)? Can we deduct it from the dividend earnings also?

Any opinions based on experience would help.

Public Sector Banks (04-06-2024)

Found this relevant, specially to PSU banks. Cross posting it here for better visibility and to maintain historical reference for future when reviewing PSU banks or banking industry.

Opportunity in banking industary (04-06-2024)

A good read on banking industry’s current status on its asset quality and asset-liability mismatch, and given the history, how are they likely to fare in the foreseeable future.

India’s Banking NPA crisis (04-06-2024)

TheMorningContext says, another crisis might be brewing… Indian banking’s inconvenient truths

Gokul Agro Resources Ltd – Good for health? (04-06-2024)

On May 15th they have announced 100Cr capex to setup Biodiesel plant.

Last year sales 14,000 Cr

Market cap 2,000 Cr

- Currently they operate on 1% NPM this can go up.

- Biodiesel fits well into their current business as

they produce feed stock themselves. - Kotyark made a killing in this space and their net

block is around 90Cr so this vertical is significant. - Huge supply gap and no need to even think of

market size. - Promoter bought ~1% stake in recent quarter.

Cons:

- They don’t do con calls.

- FY24 EBITDA is 295 Cr but the intrest expenditure

is 117 Cr. This is huge considering their total debt

is 700 Cr approx.

Bought today in the market fall @ 136

Technically the chart looks good.

Hitesh portfolio (04-06-2024)

@hitesh2710 ji,

Given the election results, how do you see the market behaving in the next few months?

Good news is : NDA forming government

Not so good news : It is a (small) coalition and not absolute majority of BJP

PG Electroplast – Potential for cooler returns? (04-06-2024)

PG Electroplast Ltd

PGEL (established in 1977) specializes in Original Design Manufacturing (ODM), Original Equipment Manufacturing (OEM) and Plastic Injection Moulding. At current price the share is expected to give a return of 45% for next year

| Date of report: | 04-06-2024 | Competitor PE | 61.71 | Sector | Electronic Components |

|---|---|---|---|---|---|

| CMP: | 2346 | Current PE | 45.2 | No of Years | 47 |

| Market Cap: | 6107Cr | Highest PE | 77.9(2022) | Key Products | RAC & Plastic Moulding |

| ROCE / ROE | 18.7% / 18.8% | Lowest PE | 33.4 (2024) | Key Competitor | Hind Rectifiers |

Business Model and Industry Analysis

Overview:

Company is into OEM manufacturing of AC, Washing Machine and Air coolers termed as Product business which contributes 61% of revenue followed by plastic moulding business. Company serves as an OEM for many leading brands such as Blue Star, Godrej, Haier, Voltas etc. Company also is an ODM where it also helps in designing products which then consumers sell them under their own brand name. It operates only in domestic market. Co pricing works as Fixed Cost + Markup where it is able to recover increase in cost but is not required to pass on any reduction. Thus the business is naturally hedged from commodity price fluctuation.

Industry Growth:

AC Industry: Expected to grow at CAGR 16.7% till 2029. Currently AC penetration in India is only at 8%

Washing Machine: Expected to grow at CAGR 7.43% till 2029. Currently AC penetration in India is only at 15%

Air Cooler: Expected to grow at CAGR 7.7% till 2029.

Plastic Molding: Expected to grow at CAGR 4.18% till 2029.

Capacity Utilisation:

The company has 5 plants namely 3 in Uttar Pradesh, 1 in Maharshtra and 1 in Uttarakhand. Co is not providing any numbers on capital utilisation. Co stands second for selling of Washing Machine units in India. Co has invested Rs150 Cr in expansion for doubling washing machine capacity while also further expand Room AC capacity to 200,000 Indoor Units and 100,000 outdoor units, along with further backward integration by adding the set up for Room AC controllers.

Opportunities:

Co has huge potential for growth in AC segment as disposable income in India is rising along with the summer temperature in India leading to higher AC sales. Further in Washing machine segment, with rising female employment, there is rise in sale of washing machine. Co is also availing grants from government under PLI scheme leading to better gross margin. It has also entered into JV with Goodworth Electronics for TV segment. This JV will help strengthen sourcing capability from China as company is planning to double its TV production. The pricing mechanism acts as a natural hedge for the company and is guarded against commodity inflation.

Risk:

Co has major risk of debt trap. With the expansion taking place the company has also been taking up debt. Although co has started mitigating this risk. To get out of the debt trap, co has raised funds from QIP for purpose of debt repayment. No other major risk is seen in company

Future Expansion:

The company has given guidance of 370cr to 380 cr of capex to expand its RAC Capacity by setting up a unit in Rajasthan and further adding up on washing machine capacity by ~60% by taking up a plant in Noida. The SUPA facilities will be expanded further with new buildings and further capacity enhancement for room AC business.

Management:

Management is genuine and decision are taken in line with investor interest. Few examples being share split to increase liquidity in market, QIP to pay off debt etc. The concerning point is that management and repalted party draw salary of around 10% from after tax profit which is significantly high. Promoters hold 53.7% in the company which is free from any pledge

Institutional Investor:

FII and DII continue to hold around 22% in the company

Historical Data and Financials

Profit N Loss Account:

* Sales have historically grown at **65%** over last 5 years and at **27%** in last year

* Margins have continuously improved and stands at around **10%** currently

* High salary withdrawl by related party amounting to 10% of PAT

Balance Sheet:

* Company has reduced its debt by raising QIP and debt/equity stands at **0.42** from **1.46** in 22/23.

* Interest coverage ratio is **4 times**

* EVA of company is negative

* Inventory days have increased from **73** days to **90** days

* Debtor days is constant

* Working Cycle and Cash conversion cycle have improved YoY

* Current ratio has improved from **1** to **3** from 22/23

Cash Flow:

* CFO/PAT is at lower side standing at 75.61% due to long working capital cycle

* FCF/Earnings is negative due to high capex investments by the company to support revenue growth

Valuation and future potential:

| Particular | Current | 52W High | 52W Low | Historical High | Historical Low | Industry Median |

|---|---|---|---|---|---|---|

| Price | 2346 | 2734 | 1459 | 2734 | 35.2 | – |

| PE Ratio | 45.2 | 57.7 | 33.4 | 77.9 | 33.4 | 74.86 |

| EPS | 51.9 | 51.9 | 41.9 | 51.9 | -5.15 | – |

| Price/Book | 6.2 | 13.5 | 3.1 | 13.5 | 0.4 | 5.83 |

| EV/EBITDA | 8.4 | 29 | 16.6 | 111.8 | 11.2 | 25.22 |

Valuation:

| Particular | 23/24 | 24/25 | Comments |

|---|---|---|---|

| Sales | 2746 | 4000 | Management Conservative guidance |

| Profit | 137 | 200 | Management Conservative guidance |

| No of Share | 2.7 | 2.7 | – |

| EPS | 52 | 75 | – |

| PE Ratio | 45 | 45 | Average PE traded |

| Share price | 2346 | 3411 | |

| Return | 45% |

Disclaimer: This is a study report, not for any decision making or investment advisory.

Made by: Nidhi Devidan

Date:4th June 2024

Sandeep Kamath Portfolio | Momentum Investing (04-06-2024)

First real turbulence today but then today was a market wide tremor. But no action taken since its mid week so I dont even check if any stock is eligible for an exit. Earliest I will check is on Thurs so lets see. Today’s hit is 8% on the portfolio.

Portfolio start date → Jan 23, 2024

Total returns → 19.3%

Aegis Logistics – Can It Be Exception? (04-06-2024)

Confcall notes: Confcall Link & FY24 – Q4 PPT Presentation

Aegis business getting supercharged now, with capex and growth lining up nicely.

Main Announcement from Raj Chandaria

Dividend Announcement:

- Final dividend recommended: INR 2 per share.

- Total dividend for the year: INR 6.50 per share.

- Two interim dividends already paid in February and August.

Company Mission and Strategy:

- Focus on transitioning to a more sustainable India.

- Mission to store and distribute bulk liquids and gases in a safe and sustainable manner.

- Looking for M&A opportunities to expand.

- Expanding distribution footprint by installing more LPG filling plants.

- Building out capex plan for growth.

Financial Performance:

- Surpassed INR 1,000 crores in normalized EBITDA for FY ’24.

- Record revenues and EBITDA in Liquid Division.

- Highest-ever volumes in Logistics and Distribution segment.

- Operating EBITDA for Liquid division: INR 396 crores, for LPG division: INR 612 crores.

- Record volumes in LPG logistics business and distribution volumes.

- Profits for FY ’24: INR 672 crores, 32% year-over-year growth.

Expansion Projects:

- Various expansions and acquisitions across different ports like JNPT, Pipavav, Mangalore, Kandla, Kochi, and Haldia.

- Total liquid capacity to reach almost 2 million KL.

- Additional 300,000 KL to be constructed in FY ’25.

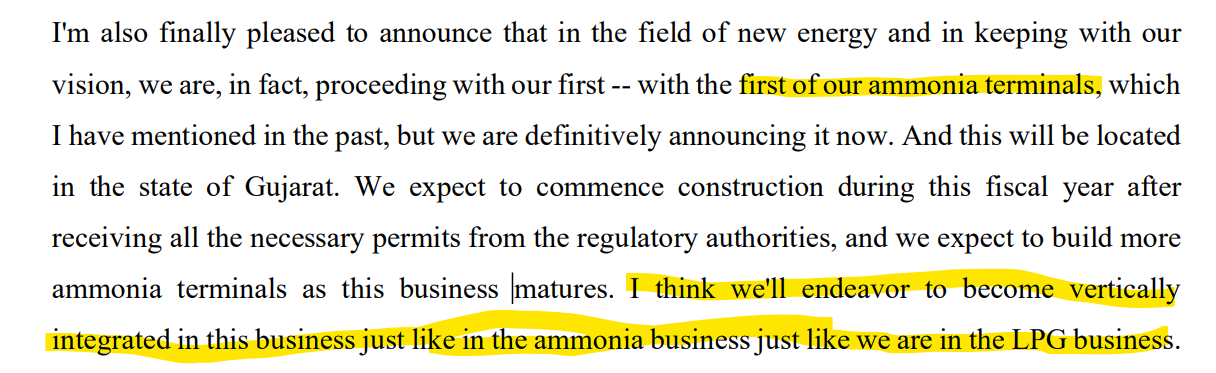

- Plans for ammonia terminals to be constructed in Gujarat.

- Major capex plan of INR 4,500 crores by FY ’27.

Q&A Insights:

- Discussion on ammonia terminal capacity and financials.

- Margins improvement in Distribution business due to procurement efficiencies.

- Expectation of logistics volumes to exceed 5 million tons in FY ’25.

- Liquid revenue growth attributed to capacity addition and product mix.

- Liquid capacity utilization at 87%.

- Expectation of 10-15% growth from capacity addition in Liquid business.

- Confidence in delivering 25% EPS growth year-on-year.

- Logistics division EBITDA per ton around INR 1,100.

- Distribution EBITDA impacted by procurement efficiencies.

Overall Outlook:

- Management optimistic about continued earnings growth.

- Focus on leveraging different business segments for profit growth.

- Emphasis on sustainable and strategic expansion for the future.

Ammonia Terminal:

- Revenue between ₹2,500 to ₹3,500 per stacking capacity metric ton.

- Potential profitability similar to LPG, around 90% EBITDA.

- Expected EBITDA of ₹120 crores at full or 3x asset turn.

- Terminal equipped to handle import and exports of various types of ammonia.

- Initial focus on gray ammonia imports and green ammonia exports.

- Expected demand for green ammonia in the future.

- Infrastructure already in place at Pipavav for the terminal.

- Initial capex estimated at around ₹500 crores.

LPG Business:

- Throughput EBITDA per ton in FY ’24 was ₹1,100.

- Distribution EBITDA per ton in FY ’24 increased to ₹4,500 to ₹5,000.

- Minority contribution to profit expected to be between 15% to 20%.

- Healthy competition with natural gas in markets like Morbi.

- Propane continues to be in demand due to cost advantages over natural gas.

- Focus on replacing dirty fuels with clean fuels like LPG.

Liquid Business:

- Return on capital employed for the Liquid division varies due to factors like CWIP, assets under construction, and cash reserves.

- IRR for Liquid division expected around 25%.

- Capacity utilization expected to be high as demand drives usage from day one.

Distribution Business:

- Procurement efficiencies led to improved EBITDA in a particular quarter.

- Average EBITDA margin in the Distribution business expected to be around ₹3,000 per ton.

Future Outlook:

- Anticipated growth in LPG demand in India due to energy transition.

- Government initiatives supporting the growth of clean fuels like LPG.

- Potential for significant growth in LPG demand in the coming years.

- Confidence in delivering good financial results in FY ’25 and beyond.

Challenges and Opportunities:

- Potential challenges from natural gas distribution plans by the government.

- Strong push by the government for LPG usage and distribution.

- Focus on continuous growth and expansion in the sector.

New Projects and Developments:

- Announcement of a new ammonia terminal project.

- Expansion of storage facilities and tanks to enhance capabilities.

- Positioning the company well for future growth and sustainability.

- Confidence in executing expansion plans and delivering strong financial performance.