Record date is 5 June.

Posts tagged Value Pickr

Sharda Motors – Emission tailwinds or EV threat to exhaust systems? (02-06-2024)

Rahul Singh Portfolio (02-06-2024)

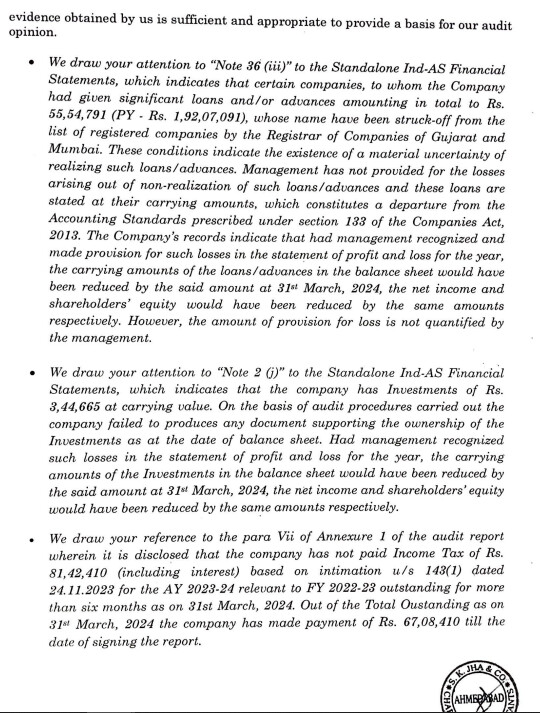

Recentyl Sumuka agro has announced its Q4 numbers. Numbers were in line of expectation.

But it has come with some negative points from auditers.

Kindly find below snap of auditer view .

- I usualy prefer stocks which are being accumalted by promoter. Here promoter has stopped buying shares where promoter holding is still at lower side.

- Since I have lost money in this type of companies previously I would like to stay from this kind of promoters who is not supporting or furnish the required information to auditers. Example- sanwaria consumer

3.Company products visibility is not increasing since last 1 year. they still have 2 SKU on flipcart and no SKU on amazon.

Hence I would chose to stay away from SUMUKA AGRO

@akash_das since you track this company let me know your view as well.

KDDL (Ethos Watches) – Scalable business model at an inflection point? (02-06-2024)

Ethos FY25 concall summary

https://x.com/radireddy/status/1797168793778561377

My portfolio updates and investment journey (02-06-2024)

Jaiprakash sir, how to calculate any asset life?

2- sir agr koi company asset ki value balancesheet may uski life ke pahle he dikha kr clear krti hai to ya red flag ku hai.

Mujhe lgta hai agar company agr company jaldi show kragi tabhi to profit show kragi balancesheet may.

Pls is guide Kro ku?

Sir Mai RAB ko study kr rha hu.

Carysil (earlier Acrysil) – Kitchen sinks (02-06-2024)

Carysil –

Q4 and FY 24 concall and results highlights –

Q4 outcomes –

Sales – 191 vs 146 cr

EBITDA – 35 vs 26 cr ( margins @ 18 pc – flat YoY )

PAT – 16 vs 12 cr

FY 24 outcomes –

Sales – 684 vs 594 cr

EBITDA – 129 vs 110 cr ( margins @ 19 vs 18 pc )

PAT – 58 vs 53 cr ( due higher depreciation, interest costs and higher tax rates )

ROE @ 17.4 pc

Only company in Asia to manufacture Quartz Sinks. Current capacity @ 10 Lakh sinks / yr. Company makes 150 different sizes / designs of the same. 50 pc of company’s topline comes from Quartz Sinks segment. 28 pc of topline is contributed by the solid surfaces segment

Company’s steel sinks capacity @ 1.8 lakh sinks / yr. Company only caters to the premium segment. SS sinks contribute to 11 pc of topline

10 pc of topline contribution comes from selling Kitchen appliances ( Company also makes some of them, and trades in others )

India business growth for FY 24 was tepid @ 6 pc. This is an industry wide phenomenon ( ie building materials Industry ). Aim to grow by 15-20 pc in FY25. Company’s focus remains the luxury and premium products. To keep pursuing the B2B segment – ie directly selling to builders

Company is planning to raise upto 150 cr via QIP

UK contributes to 30 pc of company’s topline. Getting good orders from Howdens UK ( a big – organised retailer )

Exports : Domestic sales breakup @ 80 : 20. All of India sales are recorded under company’s brand – Carysil. Only 20 pc of export sales are under company’s brand name. Aim to take this up to 30 pc in the medium term

Higher freight costs due Red Sea crisis impacted the EBITDA margins by 100-150 bps in Q4

Company is guiding for 20 pc organic growth + 150 cr topline kind of Inorganic acquisition to meet their 1000 cr topline guidance for FY 25

Avg realisation / Quartz sink is around Rs 5500. For steel sink, its around Rs 4200

Disc: hold a tracking position, biased, not SEBI registered

The harsh portfolio! (02-06-2024)

One comment on the PI Industries. From Various reports, it is evident that Chinese Agro Chem players are building aggressively and intensified Chinese dumping and also the major molecule PI is working on is going off patent. Have you looked into this aspect and still think PI industries is a good bet? I have been holding PI since 2020 and sold it now.

CSB BANK – will it become next HDFC Bank? (02-06-2024)

- I don’t think there is any moat. Banking industry is quite vanilla in nature itself. The point in favor of CSB bank is small market cap and small geographical presence and thus a headroom for growth. Under the leadership of Pranoy Monday(2022-present), bank has aspirations of going pan India which should inevitably bring growth at such low market cap.

Kerala - 30%

Tamil Nadu - 29%

Maharashtra - 23%

Karnataka - 5%

Others - 14%

Recent partnership with Jupiter (5M playstore downloads) shows intent in the areas of modernization

On the other hand, CSB bank’s own apps look lackluster.

Shreeji Translogistics (02-06-2024)

one very crucial red flag: frequent resignations of compliance officer (all officers resigning within 1 year)–>in 2020, 22,23,24. Does anyone have any inside info? why so much frequeant resignation in this KMP post?

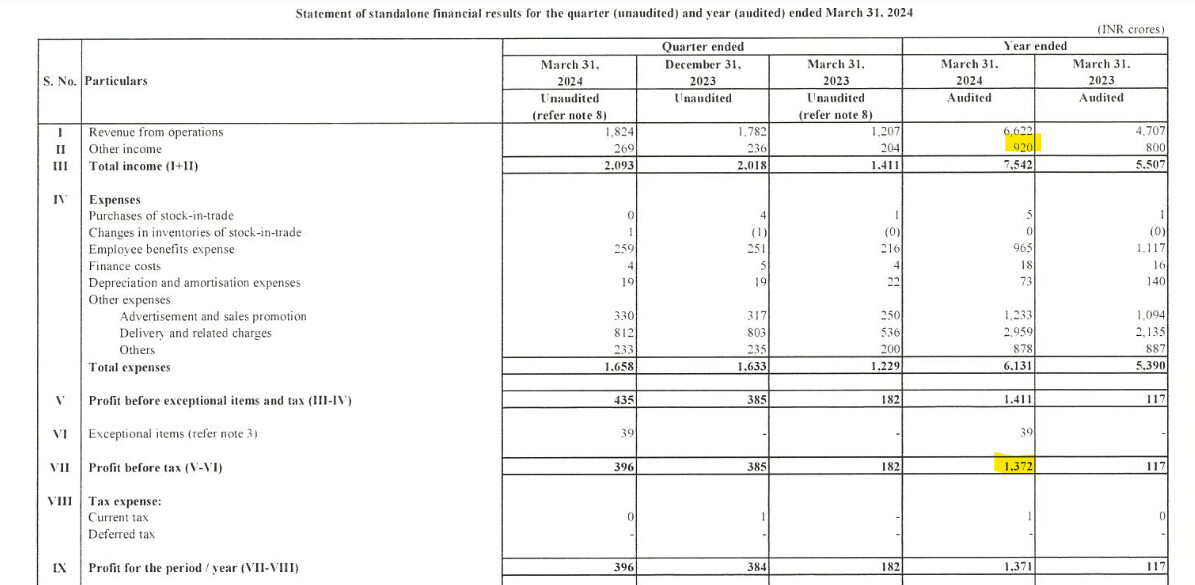

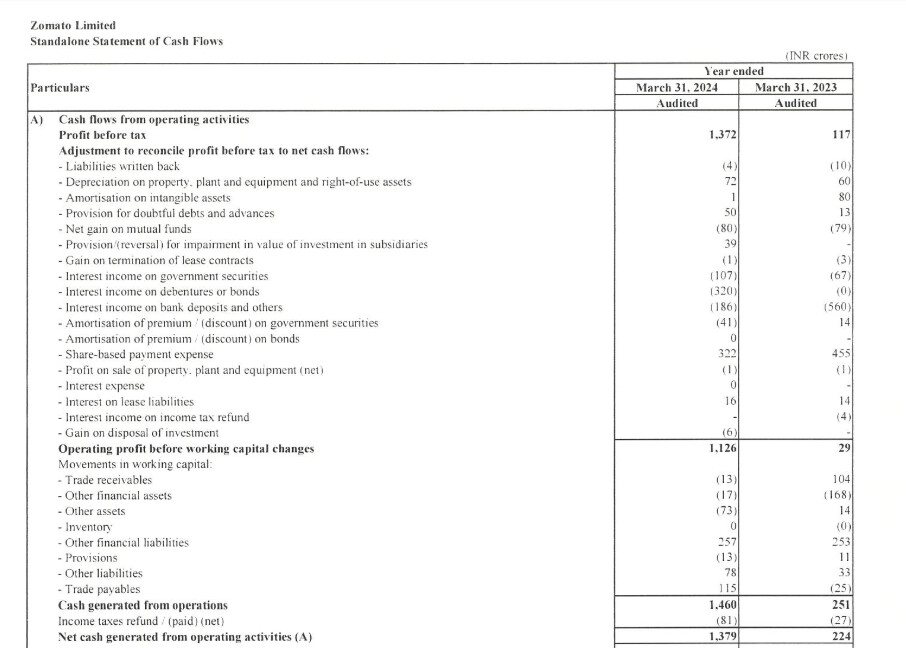

Zomato – Should you order? (02-06-2024)

Sir, I implore you to read their financial statements.

Zomato posted a standalone PAT of around 1400 crores and Q4 standalone PAT was ~400 crs. Even if you exclude other income (treasury), Zomato is PBT +ve with growing profit pools. See screenshot below:-

On the point of cash flow, attaching their cash flow statement:-

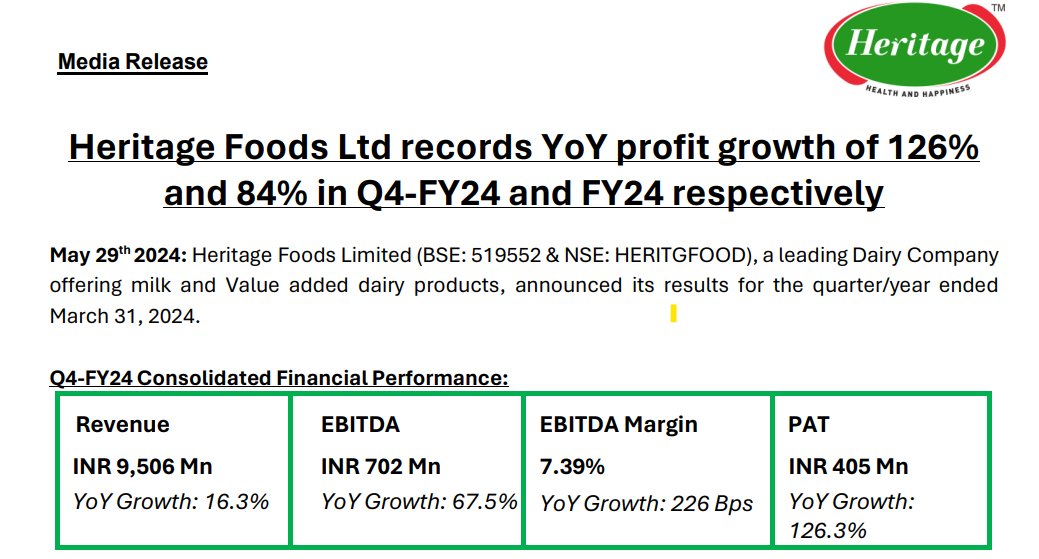

Heritage Foods Ltd (02-06-2024)

58% of revenue comes from milk however future business outlook based on management commentary includes a focus on increasing VAP share to 40% of revenue (which will take margin even higher), expanding the product portfolio (already launched 2 new ice cream: Fig Honey Cashew & Berry Burst & Vibez Ice cream) and penetrating new geographies.

Furthermore, Heritage Nutrivet Limited robust Top-line growth YoY 50% and bottom line YoY grown Exponentially 360%.