Can this Bring back the EV Charm and incentives by Govt ?

Can this Bring back the EV Charm and incentives by Govt ?

Why is the comapny doing CAPEX in electrical contacts if the space is highly competitive and even after CAPEX they will get a maximum 14% EBIDTA margin as mentioned in Q3FY24 concall

Depreciation increasing means the company is capitalising more assets and they probably haven’t gone to full production (depends on where they are in the go live cycle and industry). Short term it will drag PAT down but long term it has potential to grow topline as utilisation increases. Is it good or bad depends on your time window (short or long), company prospects and many other parameters.

The newly formed subsidiary firm, would be known as Bharat Coal Gasification and Chemicals Ltd (BCGCL) for undertaking a coal-to-chemicals business.

Coal India (CIL) holds a majority 51 per cent stake in the new entity while the remaining 49 per cent is owned by BHEL.

Some keys variables to track –

Management guides to improve the EBIDTA per wheel for its steel wheels (bread and butter business as it is called). EBIDTA per steel wheel was Rs 253 per wheel similar to previous year. Steel wheels is 72% of full FY24 revenue. The expectation is see positive side correction on 72% of the business as per the management.

Knuckles revenue shall doube from 35 cr to 70 cr and then 4x

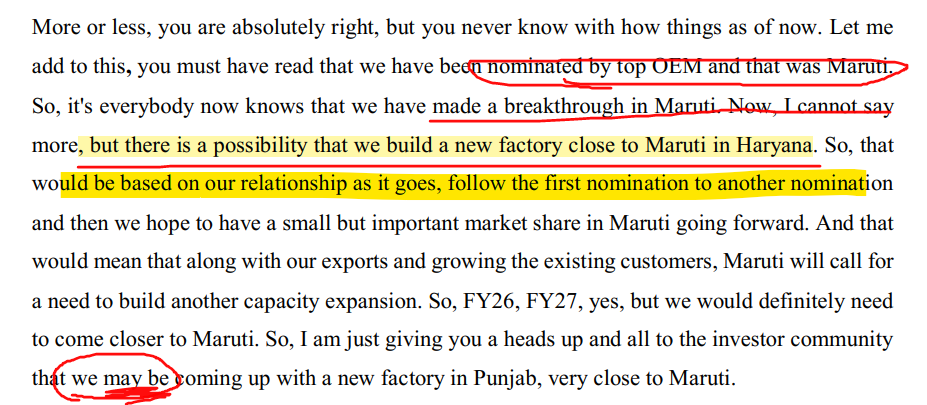

Co may consider to do a greenfield expansion very to the Maruti plant based on how the relationship with Maruti goes. (REMEMBER- “may consider”)

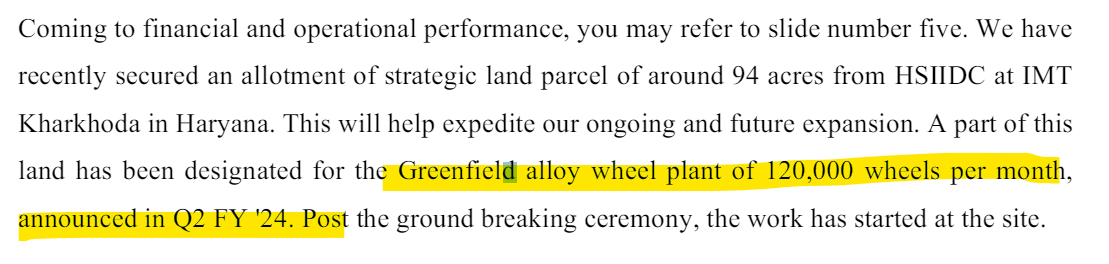

Uno minda is making a greenfield investment in alloy wheels. 1.44 Million capacity per year. Below image from UNO Minda,

Guidance of 4800 Rev for FY25 with 0% growth in CV and no revenue contribution from AWM

Following is the reply I have got from Ishmohit (founder of SOIC). I am enrolled into his course and it has been a fantastic learning experience till now. He has replied beautifully (like always):

India needs an additional 2.4 million (24 lakh) hospital beds to reach the recommended ratio of 3 beds per 1,000 people, fuelling the demand for healthcare-related real estate space, according to Knight Frank. “India’s existing bed-to-population ratio is 1.3/1000 population (both private and public hospitals included), and there is a deficit of 1.7/1000 population. To cater to the existing population, there is an additional requirement of 2.4 million beds,” the consultant said.

Thus, there is enough demand.

Most important Question, How is NH going to grow?

NH is doing Greenfield Cape’s in same cities such as Bangalore, Kolkata, & Cayman Island. ROCE on existing assets is 25%+. They are going to invest 1650+ crores in FY25. This is needed for Hospital to grow beyond 2-3 years.

In a stable growth industry like Hospitals, there will be cycles of investments and phases of reaping rewards. NH is somewhere in the middle as majority of the investments will break even in 2 years. This is a business which requires FY27-28 type of thought process to compound the money well

Just wanted to understand from community here if there was any special opportunity with the merger with CoForge in terms of valuation difference? Currently it is trading at 1310 and merger is at 1415 following which there will be share swap. Possibly the swap might give an opportunity to enter coforge at a price lower than current market?

Q4 results seem very bad. We may need to check the management commentary.

Valuation seems ok to enter now considering Q1 results going to be very good because of the extreme heat conditions which may have expected to rake in more & more ACs and ancillary appliances in the consumer households.

Even though the co has very small listed history, it has been a growymtg co based on management guidance (for me). The guidance was alwats based on existing order book and ongoing talks with the customers.

Now, for any co, even the management doesn’t have much capability to predict about the deferment of orders. That’s okay the management couldn’t predict and do missed on the guidance

The risk that has played out is the customer concentration risk. If, the customer concentration risk weren’t there, the management wouldn’t have missed the guidance by so much margin.

What could be the way forward

Disc: No personal investment currently