Got it.

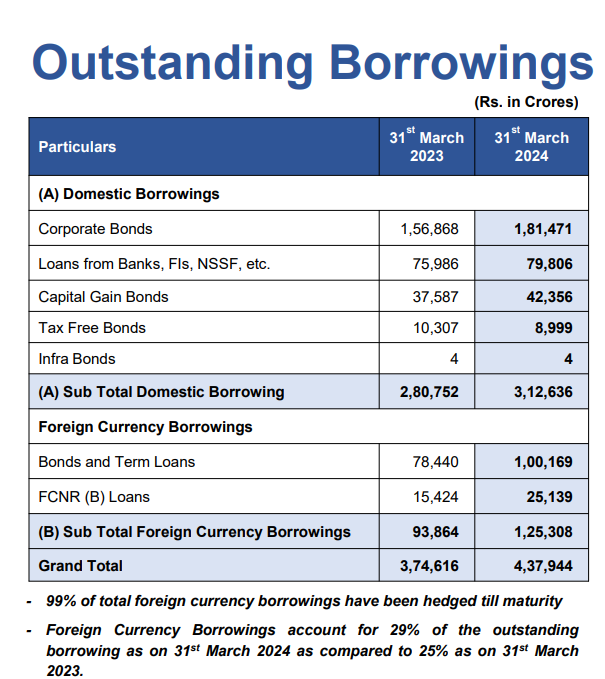

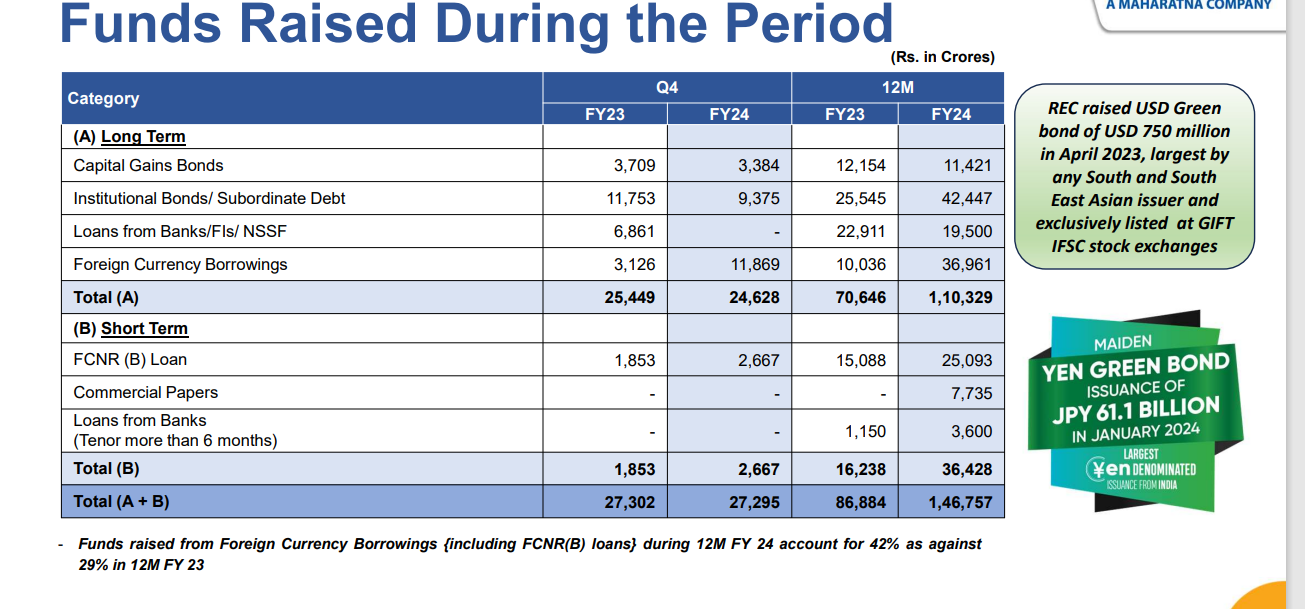

Most of borrowings are hedged. So lower cost of funds will have almost no impact on NIM in future.

Got it.

Most of borrowings are hedged. So lower cost of funds will have almost no impact on NIM in future.

For a sale of about 20 crore, PAT of 2.19 lakh is difficult to digest. Do agree if it was newly blossoming unit. Big no for a unit of 18 years old and consolidating.

Jyothy Labs –

Q4 results and concall highlights –

Q4 outcomes –

Revenues – 660 vs 617 cr, up 7 pc ( volume growth @ 7 pc )

Gross Margins @ 49.5 vs 45.7 pc

EBITDA – 108 vs 91 cr, up 19 pc ( margins @ 16 vs 15 pc )

PAT – 78 vs 59 cr, up 31 pc

Advertisement and Promotional spends @ 60 vs 46 cr ( at 9 pc of sales vs 7.5 pc of sales )

FY 24 outcomes –

Revenues – 2757 vs 2486 cr, up 11 pc ( volume growth @ 9 pc )

Gross Margins @ 49 vs 42 pc

EBITDA – 480 vs 316 cr, up 52 pc ( margins @ 17 vs 13 pc )

PAT – 369 vs 240 cr, up 54 pc

Advertisement and promotion spends @ 228 vs 174 cr, up 30 pc ( at 8.3 vs 7 pc of sales YoY )

Cash on balance sheet @ 618 cr

Breakup of revenues, full yr growth –

Fabric care ( main wash ) – 34 pc, grew by 12 pc

Fabric care ( post wash ) – 9 pc

Household Insecticides – 11 pc, sales were flat in FY 24

Personal Care – 9 pc, up 21 pc

Dishwashing – 33 pc, grew by 8 pc

Others – 4 pc

Brands … Mkt share

Exo … 14 pc

Pril … 13 pc

Ujala Detergent … 23 pc ( in Kerala )

Ujala Whitener … 84 pc

Maxo … 8 pc in Liquids, 23 pc in Coils

Other Promising brands – Henko, Ujala – Crisp and Shine, Margo, Mr White, More Light

Expanded direct distribution reach to 12 lakh outlets vs 11 lakh outlets in the previous year. Will continue to expand direct distribution by 8-10 pc / yr for the foreseeable future

New launches in FY 24 included – Henko Liquids, Ujala Liquid detergent, Margo Neem Naturals (launched 3 new Margo variants this yr)

Seeing gradual pickup in the rural markets – augurs well for next FY

Both – Ujala and Henko liquid detergents are doing well – in South of India Mkts and Modern trade

Company has lined up a few new product launches. Did not disclose their names / categories

Aiming for 16-17 pc EBITDA margins for full FY 25 after spending aggressively behind existing brands ( specially the liquid household insecticides ) and new launches

Company’s percentage of revenues from South of India @ 38-39 pc

Disc : Holding, Biased, Not SEBI registered

They have 4 verticals namely

4)Medical Consultancy :- like helping healthcare facilities with type of infr etc they would need to organize and run a hospital. point 3 & 4 are negligible part of revenue.

The major focus is on asset light hospitals in these countires where helath care is in boom but not many player were able to sutain business over here. They also mentioned that they will be doing a capex of 25 Cr in FY25-26 to put up additional beds+ equipments . Also looking for M&A in Tanzania & Nigeria.

Its worth to make a note that they have ARPOB around 0.8 CR in FY23.

Note: Invested & will add more when the story is reflecting in numbers.

Thank you so much for putting your efforts and sharing this video on a busy week start. Really appreciate that

BigBloc Construction Concerns

I have seen recently many investors getting Gung-Ho on this company but I somewhat don’t feel comfortable with this company due to multiple reasons.

1- ![]() Reasons of Bad Q4 -due to Holi vacation- shortage of Labour in both construction site and plant.

Reasons of Bad Q4 -due to Holi vacation- shortage of Labour in both construction site and plant.

![]() In Q3 concal, they mentioned → there was a volume reduction in q3 due to extended monsoon.

In Q3 concal, they mentioned → there was a volume reduction in q3 due to extended monsoon.

![]() I personally could not digest these reasons. These all reasons are quite insane to be given and how can a investor buy those reasons without thinking twice? All thanks to the price movement in stock which actually give them the confirmation bias make them bullish unnecessarily thinking it’s all good.

I personally could not digest these reasons. These all reasons are quite insane to be given and how can a investor buy those reasons without thinking twice? All thanks to the price movement in stock which actually give them the confirmation bias make them bullish unnecessarily thinking it’s all good.

Holi was there in Q4 last year also. Then why such issue this year? (As mentioned above by another investor)

2- Percentage increase of Sales– 14.20% and 21.57% in March 2023 and March 2024 VS percentage Increase in Receivables– 18.35% and 67.90% in March 2023 and March 2024 respectively.

Parallelly Percentage increase in Inventory– 75.20% and 46.19% in March 2023 and March 2024 respectively which makes me suspicious about their sales numbers.

3- Their EBITDA margins are almost double of their competitors even from the largest player in the industry which again makes me more suspicious without any strong justification for the same that how are they able to operate on such a high margins catering to B2B clients that too in a Real Estate sector.

4- Also CFO/Ebitda is 56% and 35% in March 2023 and March 2024 respectively which is considerably low, which again is alarming.

5- If their ROCE is north of 30% then why their is still rise in Net Debt I know one will argue that they are in expansion phase even considering that the debt shouldn’t increase if the ROCE is north of 30% there are companies who have executed the expansion without increasing the Debt to this level considering their ROCE was also in line with this company.

I know I’m making this contra perception and many won’t agree to this but feel free to share your opinion and kindly correct me if I’m wrong somewhere in my analysis.

(post deleted by author)

As quite a few people had asked, I have prepared a short video explaining how the calculation for 50EMA and 200EMA is done. Link given below. Please let me know if the video is clear. Thanks.

Any update on Quaterly Result??