Hi,

Thanks for bringing this data in notice.

Which tool shows data in this format?

Thanks & Regards,

Sushil

Hi,

Thanks for bringing this data in notice.

Which tool shows data in this format?

Thanks & Regards,

Sushil

Will you be posting your MF portfolio too?

And please see if you can add desc with reasons to choose that fund.

Thanks in advance

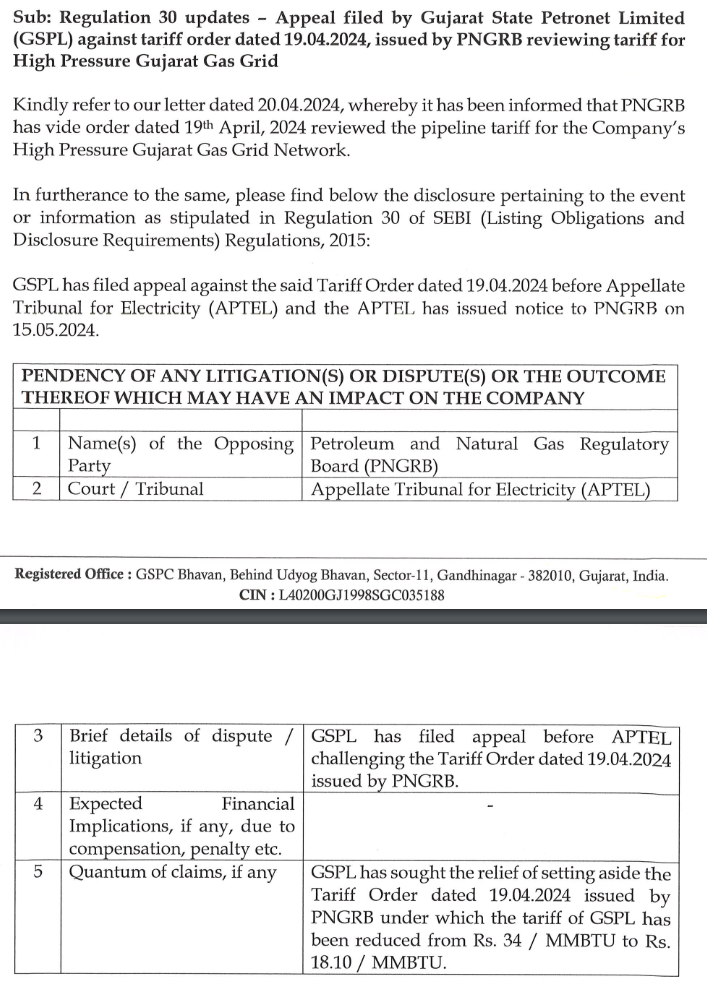

GSPL has appealed against the tariff order by PNGRB before Appellate

Tribunal for Electricity (APTEL).

to me it looks positive, as I wrote earlier, I was expecting 100Cr only

In the November call, they only cited ~100Cr of receivables for booked, unbooked, and retention money. Even in a recent call, I heard a similar figure; what is the 400Cr amount? According to my understanding, it is using a price increase provision following a force majeure to negotiate 100+ crore. I see the focus is largely on recovering ~100 crore.

disclosure: invested

Didn’t follow you. Are you comparing CMS with Infosys/TCS ?

They (Altius)where good few months back but now they are more into getting 10-20% margin.

So I will advise WhatsApp at least 5-7 brokers and get the best suited price.

And the second thing it’s very hard to value unlisted share there are more opportunities in listed shares.

Few days back valuation of OYO was around 6 billion and in 5-10 days they raised funds @3 billion or lower.

Its over! who won?

The results are in and as expected we are looking at a solid QoQ growth and an equally solid YoY.

The ebitda is up 16.6% YoY, consistent PAT margin at 16% YoY, QoQ Revenue stood at whooping 25% and YoY at 18.3%.

Coming on segment wise the tech solution business seems to be the growth engine here with 35% YoY growth in revenue.

Biggest YoY growth in revenue segment wise came from card services at 47.4% YoY followed by ATM managed services at 30.2% on the flip side the cash mgmt services grew at 11.1% YoY. Looks like the company is now changing its focus from a atm management business to a more actively managed software and tech business.

Can anyone here point out how much of the company’s tech related business overlaps with what large cap tech giants like TCS, Infosys provides to Indian banks or is it completely different?

A to Z of data centre by Ameya & Dinesh

Data Centre Decoded #datacentre | Ameya @finstor85 | Dinesh | #AI Prince

Con Call Notes for Q4-24 (CMR 80) . PPT

Co-Lending

Making a lot of backend investment. 2/3rd focus is building the backend.

HFC 880 cr equity. Following the old model Housing Fiance model 1.0.

ARC dominant player- 40% market share

Wholesale reduction will take another two years, but it is becoming more and more insignificant.

In the next two years- By selling, AIF/Nuvam will be liquidated in 2 years. Current net debt shall be reduced from 7500 to 3500 cr in the next two years.

Business will start giving dividends from the underlying dividends.

Insurance business losses have peaked. They will reduce going forward

Mutual Funds

NON-ETF- 100,000 cr in another 18 months.

MF industry- A good driver of profitability is equity AUM. In the next couple of years, we aim to achieve 50% of equity AUM. Most good players are between 50-60%

Equity AUM has an upfront cost.

Good cost to income 50 -60%. Ours is 85. Aiming to bring it in line with the industry

Last year invested. Opened new offices in new cities. Only in 30 cities. We could go to 100 cities.

Each branch takes 50/60 lakhs to set up. The branch will break even in 6/8 months, depending upon the product mix.

Staying power is very important.

13rd largest AMC in India

It is a scale business.

It takes about 5 yo 7 year and 100,000 to get to scale. New players needs 5/7 years and 3000 cr of investing to come to 100,000 cr AUM and need lof of AUM.

Corporate Debt

13,000 cr now

3000 cr of liquidity is holding

AIF (Alternative)

Lot of competition in private credit.

They are on third funds in most of our strategies. Carry income from the first and fees from the second coming in.

They have a track record. It matters when you are scaling your business. It need strong distribution within India.

They have distribution in India and abroad.

Deployment of around 7k in FY23 and Fy24.

The primary focus is risk management, not deployment.

FY24 will focus on closing funds, and FY25 will focus on deployment. Hope to scale the business in Fy25

Clocking 250 to 300 cr annualised profit (based on 75 cr PAT in Q4)

In the next six months (Oct to Dec quarter), long-term plan for the business including listing.

There are 5/6 segments called AIF. We are only in two

1- PE. We hope to do business

2- Private Credit

3- Infrastructure

4 Real estate (e.g. REIT)

5- Hedge Funds (PMS/Public)- No there

Enough space to grow within existing spaces and also to enter into new spaces.

The key is expertise, which takes 5/10 years to build and build a track record and distribution.

Globally, when there is a fee plus carry, it is called an Alternative.

Valuation