2 Order wins annoucements in this month, 34MEuro & 49M$.

Posts tagged Value Pickr

A tale of 3 companies – TCS vs Infy vs HCL Tech (13-05-2024)

Interesting how head count ballooned in FY2022

JTL Industries – Fast Grower at an inflexion point (13-05-2024)

I missed the concall today so I was searching for notes. If anyone has made notes, please do share.

Dynamic Cables – Much more dynamic in 2022? (13-05-2024)

Well, looks like, ” there seem to be limited triggers (Currently) for Dynamic Cables that can help the co’ achieve a 20-25% PAT Growth” needs to be updated.

Company announced on 10th May 2024 that it is going to raise funds ! (Amount is not known yet but likely ~100 Cr (not verified)) for expanding Capacity.

My portfolio updates and investment journey (13-05-2024)

Sir any specific sector or shares on your radar to study or on your shopping list?

Ranvir’s Portfolio (13-05-2024)

ADF Foods (very bullish management commentary) –

Q4 FY 24 concall highlights –

Revenues – 153 vs 123 cr

EBITDA – 34 vs 24 cr ( margins @ 22.3 vs 21.5 pc )

PAT – 25 vs 16 cr

For Full FY 24 –

Revenues – 520 vs 450 cr, up 16 pc

EBITDA – 104 vs 80 cr (up 30 pc, margins @ 20 vs 18 pc)

PAT – 74 vs 56 cr, up 32 pc

Segmental performance –

Processed foods –

Sales – 132 cr, EBITDA – 36 cr ( margins @ 27 pc )

Distribution of Unilever brands (company distributes Red label, Knorr, Taj Mahal brands in international mkts) – Sales – 21 cr, EBITDA – 1.7 cr ( margins @ 8.2 pc )

Company is presently exporting its processed foods offerings to 55 countries

Ashoka brand ( company’s biggest brand ) revenues for FY 24 @ 254 cr ( 5 yr CAGR @ 29 pc )

Company expects the strong topline growth in Q4 to continue into the next FY

The Truly Indian – brand launched in US. Seeing descent traction

Expansion in Gross Margins due to mix change towards higher margin products

Both the brands – Truly Indian ( for International markets ), Soul ( for Indian markets ) continue to be in investment mode. Likely to remain like that for foreseeable future

Have been trying to list Truly Indian brands in American supermarket chains. Currently listed with 02 large chains giving the company access to about 350 retail outlets. In Germany, Truly Indian brand is available in over 1000 stores. In UK, its available in over 500 stores

Targeting > 20 pc topline growth for FY 25 !!! ( with better capacity utilisation, cost absorptions … this should led to an even better PAT growth )

Because of issues with supply chains wrt Red Sea crisis, EBITDA margins were adversely affected in Q4. Company is seeing return of normalcy wef Q1. This should further add to margins

Company intends / targets – Truly Indian brand to be as big as the Ashoka brand in 4-5 yrs. For soul brand, company is targeting > 100 cr sales in about 3 yrs

Company’s Surat manufacturing facility ( Greenfield capex ) is expected to be ready in 15-18 months

25 pc of company’s standalone top line comes from contract manufacturing for various brands. Company is in talks with multiple brands and they expect this B2B vertical to expand to 30 pc of sales in FY 25

Have lined up another 20 products for launch under the Soul brand in India in FY 25

Disc: holding, biased, not SEBI registered

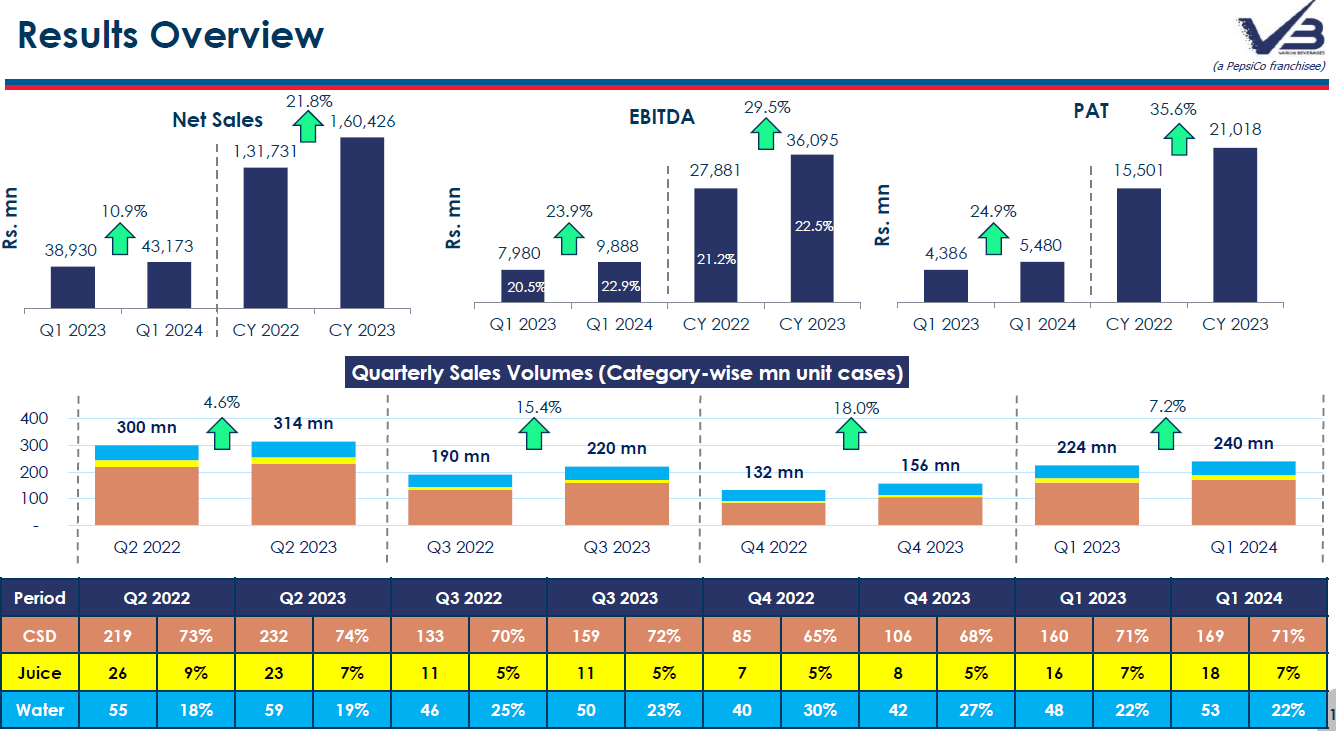

Varun beverages fast growth duopoly business (13-05-2024)

Q1 2024 results: Good YOY growth

- Consolidated sales volume grew by 7.2% to 240.2 million cases in Q1 CY2024 from 224.1 million cases in Q1 CY2023.

- PAT increased by 24.9% to Rs. 5,479.8 million in Q1 CY2024 from Rs. 4,385.7 million in Q1 CY2023 driven by volume growth, increase in net realization and improved profit margins.

- Gross margins improved by 385 bps to 56.3% from 52.4% during Q1 CY2024 primarily due to reduced PET prices as well as the focus on reducing sugar content and light-weighting of packaging. Approx. 46% of our consolidated sales volumes come from Low sugar / No sugar products.

- EBITDA increased by 23.9% to Rs. 9,887.6 million YoY and EBITDA margin improved by 240 bps to 22.9% in Q1 CY2024, led by higher gross margins and increased realization.

Next two summer quarters to follow ![]()

No Moat Growth IT Services Sector (13-05-2024)

I mostly agree with the issues highlighted, therefore, I think the type of companies we should look for need to change. Over the long term, ER&D(firms like LTTS & KPIT )and IT products firms(like intellect) looks interesting.

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (13-05-2024)

Any idea on why the trading window is closed from today? Results are anyway out, so what price sensitive announcement is pending?

https://www.bseindia.com/xml-data/corpfiling/AttachHis/6a6b09be-4388-450e-b644-aebfdfb01522.pdf