For the location (Coimbatore), I’d say that’s fair.

The Average Compensations for CFOs in Coimbatore is actually much lesser: https://www.glassdoor.co.in/Salaries/coimbatore-cfo-salary-SRCH_IL.0,10_IC2836047_KO11,14.htm

For the location (Coimbatore), I’d say that’s fair.

The Average Compensations for CFOs in Coimbatore is actually much lesser: https://www.glassdoor.co.in/Salaries/coimbatore-cfo-salary-SRCH_IL.0,10_IC2836047_KO11,14.htm

This shouldn’t matter and is neutral if they all stocks in proportion of holding. This can benefit if they sell over valued stock which turns out to be under performer. This will be negative if they sell something which turns out to be out performer.

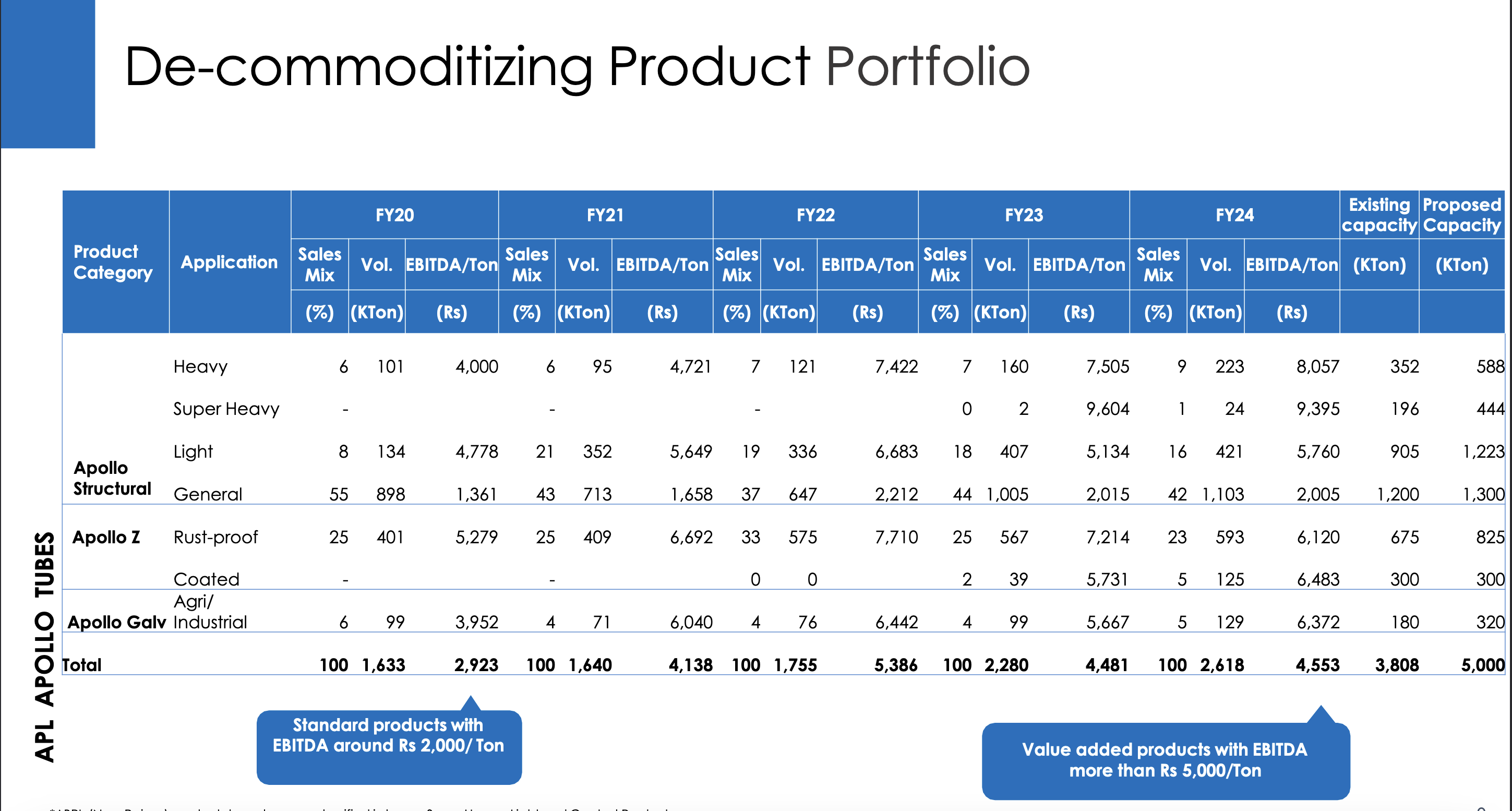

Results look flat. At 6% margin,only high double digit sales growth can push EPS. Although there are some discussions about “De-commoditizing Product Portfolio” but are have not started reflecting in OPM.

While the promoter group is busy flaunting over LinkedIn and other social media platforms. The shareholders lost value over time in this business.

One simple thing such promoters can do is to share cash flows regularly with shareholders however, what they do is completely reverse, they keep that cash in the company and take hefty salaries and perks to enjoy their lavish lifestyle.

Just check what all Aakriti Gupta (the daughter of promoter) is doing over LinkedIn, giving gyan to people over wealth, corporate culture, ethics, business and entrepreneurship etc. while travelling to useless conferences.

Possible to share a .pdf?

Disclosure: Invested

https://www.bseindia.com/xml-data/corpfiling/AttachHis/d9aabcc4-17dc-4c11-9952-a52d7bc68e6c.pdf

Disclaimer: I have vested interest in CMS Info. And, tracking Radiant Cash. Both having different models.

Unable to read Australian Financial Review article due to paywall.

Some differentiating factors in Indian industry from Australian industry:

However, I do think there will be pressures in the long run as services like Cash on Delivery etc lose their value. As they have started to already, delivery guys and cab drivers are readily accepting UPI which was not the case before. Hospitals also have constraints that you cannot pay more than 2 lacs in cash. There should be discomforting transition period for companies in future (no prediction about timeline).

Investment thesis in nutshell:

good webinar on the data center ecosystem by industry experts organized by the Care Edge team.

The company got a recent patent in “Multi-Layered Breathable Prefabricated Precast Wall panels and Structure” – any visibility on contribution to Topline in non-asbestos category ?

waiting for the concall. source is LinkedIn of MD Sayten Patel

Disc – Invested

To understand the prospects of Indian cash management companies, it might be useful to look at how similar companies have performed in other markets. One parallel example that may be useful is that of an Australian cash logistics company, Armaguard, which is currently fighting to stave off bankruptcy and is negotiating a rescue plan with its potential investors.

The reasons why Armaguard got into trouble in the first place bear some similarities with Indian CMS companies like Radiant. Despite being in an oligopolistic market, a consolidated customer base consisting of banks and large retailers led to price wars between the two largest players in the market, Armaguard and Prosegur. Radiant too has indicated in its concalls that it has been facing pricing pressure from its customers while renewing contracts.In 2022, Armaguard and Prosegur merged but that did not help improve the prospects of the combined entity much due to a faulty business model where the pricing was based on volume of cash handled, which has been declining, while the cost structure is fixed leading to deteriorating unit economics. Radiant too has indicated an increase in the share of volume based revenue model from a fixed price one earlier.

There seems to be a misconception that the cash in circulation (CIC) will not decline as a percentage of GDP in India going forward. While it is true that CIC to GDP ratio has actually gone up since demonetisation, the reasons for this paradox need to be understood better. This working paper from the RBI outlines these.

Reserve Bank of India – Database.

The paper suggests that the recent anomalous growth in CIC-to-GDP ratio was primarily on account of COVID-19 pandemic where household preferred hoarding cash as a hedge against uncertainty arising out of the pandemic. As the effects of the pandemic recede, CIC-to-GDP ratio has started falling again and if this trend is likely to continue in the future then it may not augur well for CMS companies like Radiant who will be forced to fight for increasing their market share of a declining total addressable market (TAM).