Posts tagged Value Pickr

The SME portfolio (12-05-2024)

Judicial custody of director under money laundering act.

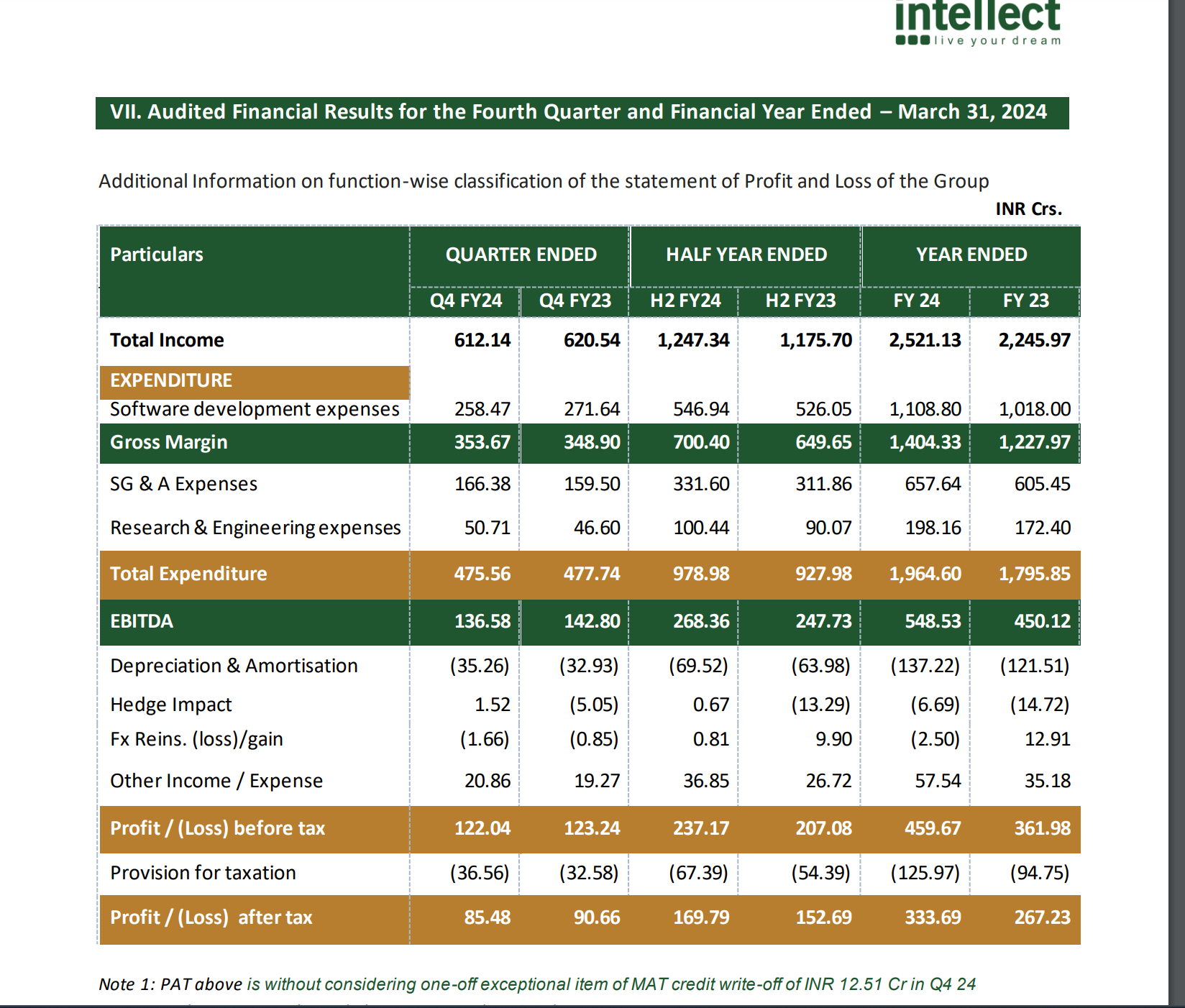

Newgen Software (12-05-2024)

Change in strategy to focus on large banks:

So when we are talking of changing strategy, we are talking about pivoting from the smaller

bank sizes to a larger addressable bank, which are banks above $20 billion or $50 billion up to

$200 billion, which is typically around 100 accounts.

Companies with 20%+ growth guidance for next few years (12-05-2024)

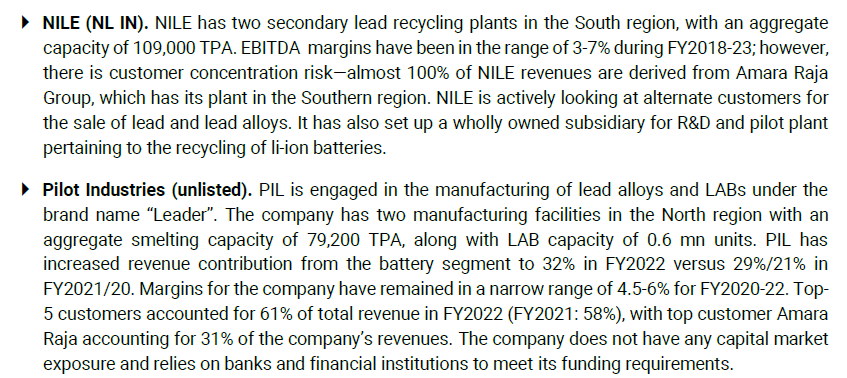

My personal view point is that companies like NILE and Pilot Industries should be impacted more which have a major dependency on Amara Raja Batteries for their sales. They are geographically also less diversified.

Credit: Kotak Securities.

Gravita should do much better considering the global network and diversification.

Companies with 20%+ growth guidance for next few years (12-05-2024)

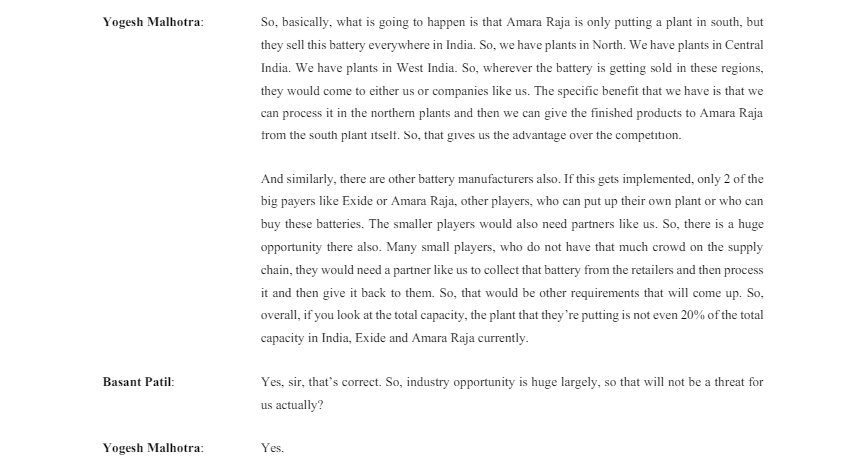

Posting a snapshot from the Mgmt concall in May 2024 on this question:-

The SME portfolio (12-05-2024)

Anyone buying in any quality SME with recent fall?

Commodity and Cyclical Plays (11-05-2024)

Tijori Finane: RM section

Commodity and Cyclical Plays (11-05-2024)

Tijori Finane: RM section

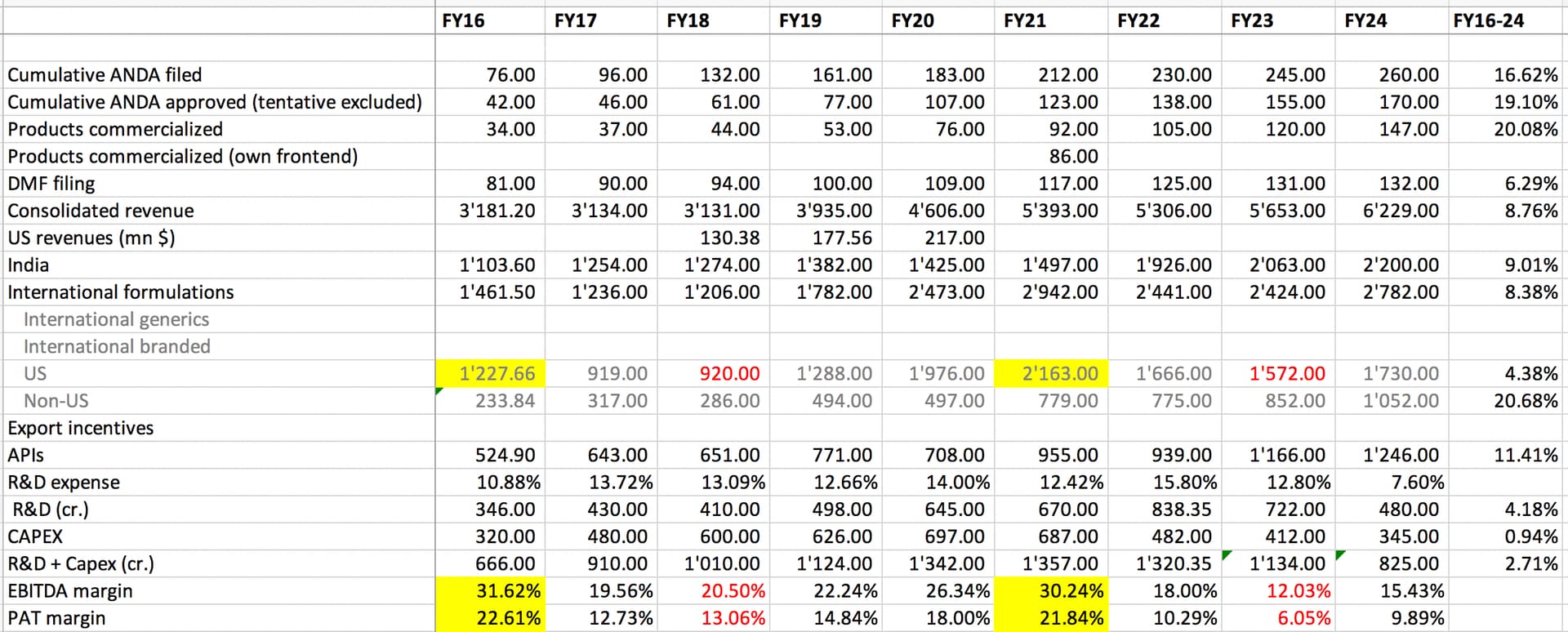

Alembic Pharma (Oral Solids ==> Injectables, Onco, Derma, Opthalmic) (11-05-2024)

Recovery continues for Alembic with them growing sales by 8% and EPS by 17%. Finally they seem to be getting closer to 20% EBITDA margins and have commercialized large number of products (27 in FY24, 25 planned in FY25). Concall notes below.

FY24Q4

-

7 products launched in Q4 in USA (27 launches in FY24). Expect to launch 25 products in FY25

-

Expect quarterly US sales of $50mn (lower than $55mn earlier guided) as there were one time opportunities in 3QFY24

-

Gross margins increased to 75% due to increased US sales in the US, R&D and other cost optimizations. Expects GMs to be 70%+

-

Expect 20% growth in ROW business. International business is now 40% of order book vs 20% earlier

-

API is regulated market business and higher margin than corporate margins

-

FY25 capex: maintenance (300 cr.)

-

R&D will increase to 550-600 cr. in FY25 (vs 480 cr. in FY24)

Disclosure: Invested (position size here, no transactions in last-30 days)