Commonmentalmistake ( TILSON)

~. Overconfidence

~ Projecting the immediate past into the distant future.

~herd like behaviour ( social proof) , driven by a desire to be part of crowd or an assumption that the crowd is omniscient

~misunderstanding randomness;seeing patterns that don’t exist

~commitment & consistent bias

~Fear of Change, resulting in a strong bias for the status quo

~“Anchoring” on irrelevant data

~Excessive aversion to loss

~using mental accounting to treat some money differently than other money

~.Allowing emotional connection to over ride season

~.fear of uncertainty.

~ Embrace certainty

~. Overestimating the likelihood of certain events based on very memorable data or experience.

~. Becoming paralysed by information overload

~. Failing to act due to an abundance of attractive option

~. Fear of making an incorrect decision & feeling stupid ( regret aversion)

~. Ignoring important data points & Focusing excessively on less important ones ; drawing conclusion from a limited sample size

~. Reluctant to admit mistake

~ Overestimate the degree to which on would have predicted the correct outcome ( hindsight bias)

~. Believing that one investment success is due to wisdom rather than rising market,but failure are not ones fault

~. Failing to accurately assess ones investment Tom horizon

~ Tendency to seek only information that confirm ones opinion or decision

~ Failing to recognise the large cumulative impact of small amount over time

~Forgetting the powerful tendency of regression to the mean

~. Confusing familiarity with knowledge.

Posts tagged Value Pickr

Investment principal & checklist from great investor (09-05-2024)

Investment principal & checklist from great investor (09-05-2024)

(post deleted by author)

CMS Info Systems Ltd (09-05-2024)

I am currently studying CMS Infosystems. Good to see this thread on Valuepickr. The answers that the management gives to the question concerning threats to their Business Model i.e., the Impact of a higher adoption rate of digital currency/UPI are listed below:

- First of all, the Cash Logistic Business is a B2B business and their revenue model is not directly correlated to the volume of ATM Transactions, rather their revenues are directly correlated to the no. of touchpoints.

- It is in the business plan of Banks to add more and more branches to enhance their physical distribution (to improve CASA & Loan growth). Historically, for every branch, 2 ATMS are being added. So, an increase in ATMs will increase CMS’s Cash logistic business.

- To put down the growth in no. of ATMs, in 2021, there were around 225,000 ATMs & it is projected to grow at 6.5% to 365,000 ATMs by 2027. One more data point that they mentioned in one of their Investor meet was that currently 60% of ATMs are being outsourced by banks, rest 40% are managed by Banks, themselves. This split was 50%-%50% between self-maintained & Outsourced a year back. They said that banks are trying to focus primarily on their core business and outsourcing other things. This 40% ratio will even drop further and thus will increase the market size.

- The future market size of the Cash logistics business (FY 2027) is projected to be 8000 Cr. Considering their 45% odd market share, this creates a turnover of Rs. 3600 Cr from the cash logistics business alone from Rs. 1300 Cr in FY 2023. This will be a growth of 29% CAGR.

- Furthur, they said that RBI had issued a circular/data, wherein it stated that Cash and digital currency will co-exist in the future. As a testimony to it, they said in one state of the USA, a law has been passed for the vendors not to refuse payment in cash, signifying the co-existence of both modes of currencies

These were some answers that management gave to the question of the future of the cash logistics business. Another thing that I have seen from my personal experience is that even though I am going the majority time for cashless transactions, i.e., using UPI for small payments for Auto, Cabs, Grocery, Street Foods, etc., these recipients (vendors) do not use UPI for making their payments or in their their expenditure. Rather, what they do is, withdraw cash from their account and use it in their discretionary spending. So, what trend is becoming evident is that earlier, people like you and me used to transact in cash with such vendors for our discretionary spending by withdrawing surplus from our banks (Which means we used to do activity in ATM), v/s now, people like you and me pay through UPI for Discretionary Spending and these vendors are getting money in their bank so they go to ATM to withdraw money from ATM.

The management also said that even after the UPI Transactions touched new highs in our country, but the ATM transactions have remained steady at similar levels. This means that the Set of People using ATM Services is changing but not the level of activity. Although I don’t have the numbers to back this analogy, I do get some conviction after thinking in this way. Any Logical arguments will be positively accepted.

Their AIoT Business & Managed Services business are growing at a good pace their share of revenue to total revenue is also increasing. I believe the biggest moat that this company has is its DISTRIBUTION NETWORK. The pace at which they are growing their newly launched AIoT Business (from 0 to 400-500 Crs in 3 years) is backed by their distribution strength. Leveraging their distribution, they can build a large business from here on.

The other side of me also acknowledges the fact that the management is also looking to diversify from the cash logistics business and reduce revenue share from this segment. They too acknowledge the risk of digital currency in their Annual Report & DRHP.

In a news article shared on VP & other public platforms, I read that they are piloting Gold Logistics & related services also. I couldn’t find any official news for this. If anyone has anything on this part, please share.

Disclosure: I started Studying recently. Not invested currently.

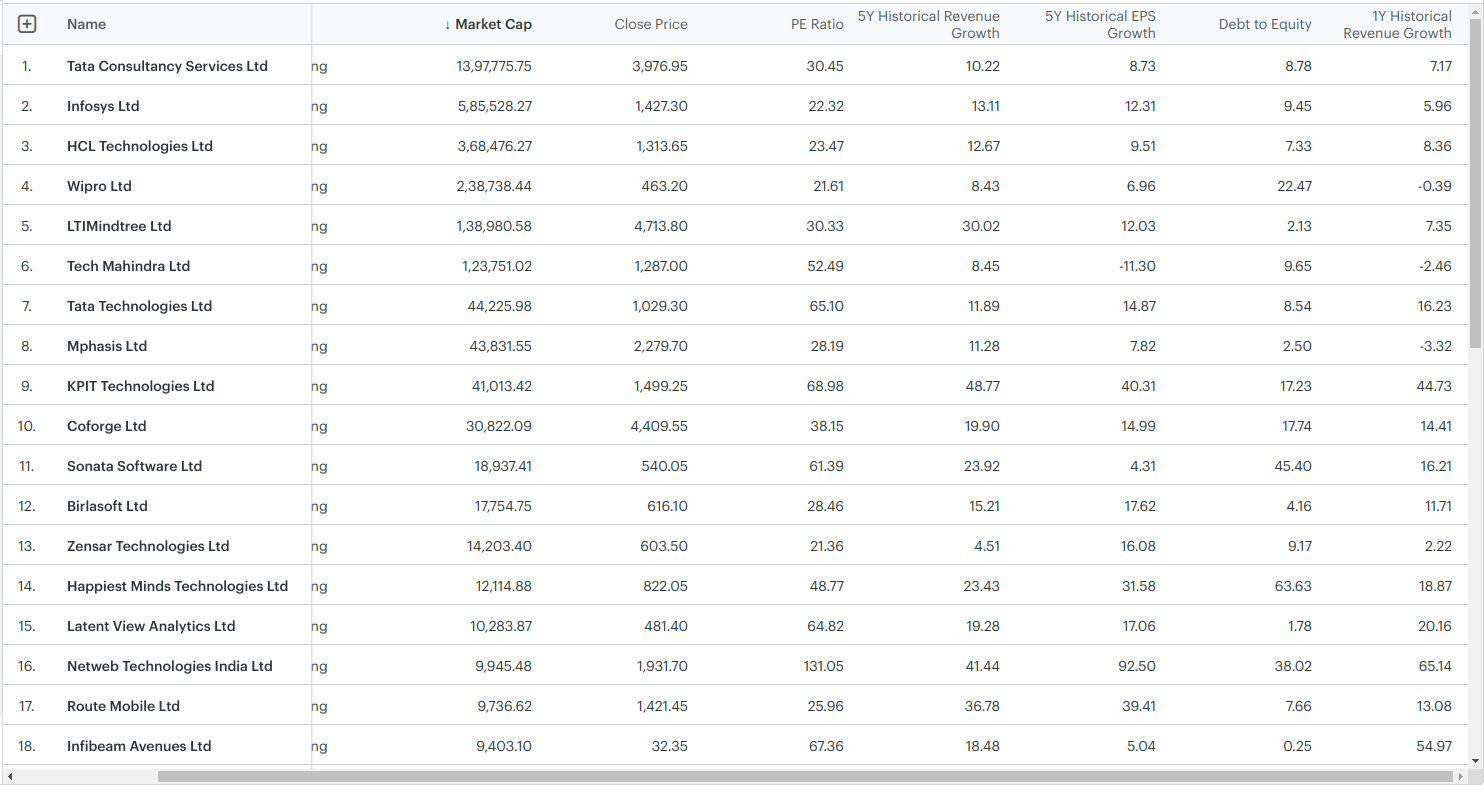

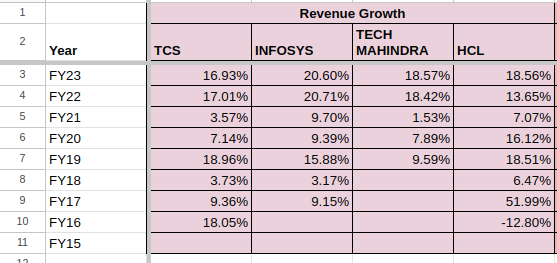

No Moat Growth IT Services Sector (09-05-2024)

There are lots of IT companies, everyone seems to grow. employees themselves jump from one IT to another for a pay raise. The talent moves, the customers move and I am sure the shareholders also move.

Important Question,

- how do you select a stock here? how much percentage have you given allocation? What is the reason for selecting the particular stocks? interested in response only from people who plan to hold this sector for next 10 to 15 years.

Longterm issues with this sector,

- Dollar might lose value, all central banks are buying gold. less interest is seen with dollar. So service cannot just focus on the dollar. they have to move to all currencies. the cushion that we had on IT services revenue when rupees lost value will no longer be the way it used to be.

- India is diversifying, CNG, Electric, petrol, etc. what use to keep the dollar more valuable is decreasing. expectation is to decrease. so more we become self-sufficient. cost advantage that these IT companies enjoy loose over time. self sufficient india not in IT companies favor

- Growing AI intelligence, IT services has to be more adaptive to changes. much more than before. It cannot be a kodak or nokia. It have to adapt quicker than before.

Share you thought process on this sector why and what you have? how much allocation have you given for it.

Nifty 50 : ~12.7% allocation (6 stocks)

Nifty 100: ~10.92% allocation (7 stocks)

Nifty 500: ~ 9.66% allocation (33 stocks)

Bull therapy 101-thread for technical analysis with the fundamentals (09-05-2024)

I am not sure how this chart is useful at all unless we expect smallcap index and Sensex to give same returns over long period. If one of the index gives even couple of % higher CAGR over decade+, the ratio will get skewed in favor of that index.

Same applies to S&P 500 vs Gold chart that get’s shown many times. These are typical cases of torturing the data to reveal what you want.

The rebound time is also incorrect since it leaves out dividends. We should be checking Total Returns Indexes. I have Nifty 50, Nifty Next 50 and Nifty Midcap 150 Index TRI data in front of me. Post 2008 January Peak, Nifty TRI took 33 months to cross previous highs. Nifty Next 50 TRI took same 33 months and Midcap 150 TRI took 76 months (it reached 90% of previous peak in same 33 months). Long periods but nothing as long or as dramatic as 9 years.

PayTM (One 97 Communications Ltd) (09-05-2024)

Seen that, but what happened with RBI makes me unsure to believe that. Hope it is different this time. Time will tell.

Lt foods (daawat) (09-05-2024)

I have a question, and if someone can please help me understand it, will be helpful.

LT Foods has consistently maintained 10-12% OPM over a long period, whereas the same for KRBL/Chamanlal Setia is not reflecting. Checking historical price trend of Basmati Rice (C Setia page 18/35) , I find it surprising how they have managed to maintain these margins. Their annual report mentions strong brand allows them to pass off these hikes to customers, but then India Gate is also a strong brand, however they can’t maintain it.

Can someone please throw some light on how this works? Is pricing for Finished goods different in US and EU? Logically, if RM and FG are both subjected to such fluctuations and there is a gap of 1-2 years in transactions, they should be impacted by this, correct?

As I close my research for this scrip, this is a big pt in my mind. (Risk being that actual OPM is quite large and they are skimming off in good years and putting something back in bad years)

I have no investment in this, and I am studying as of now

Piccadily Agro Industries Ltd (09-05-2024)

A stock can’t keep rising indefinitely. It will eventually face selling pressure and hit lower circuit for a few days. In October-2023 Piccadily was at Rs 312, then it hit lower circuit for many days and went down to about Rs214. It stayed in that range for a few months before shooting up again in Feb-2024. This is a normal pattern for stock price growth.

Piccadily Agro Industries Ltd (09-05-2024)

Why stock is hitting lower circuit for two days… is this profit booking ? pump and dump…

Just trying to understand broader picture,for this behavior

Will delete this post…

JSW ENERGY — channel breakout (09-05-2024)

Why is jsw energy falling in spite of good results? Is it because of the fund raising plan? Is the market wary of over capitalisation?