luckily these indian hype men tend to not speak much english

Posts tagged Value Pickr

Macfos Limited- A niche E-commerce Company (08-05-2024)

Examining the annual results for 2023 reveals sales of 80 Cr and a profit of 7 Cr. However, when focusing solely on the March quarter, sales and profits are reported as 72 Cr and 7.93 Cr respectively. This scenario seems implausible as it suggests the company generated nearly all its sales and profits within a single quarter, which is unlikely. Therefore, it appears that the data presented by the screener is inaccurate. Despite this discrepancy, the company has demonstrated decent growth, evident in its annual performance.

Investing Basics – Feel free to ask the most basic questions (08-05-2024)

There are various scenarios exist not one exact can be derived unless you give the whole picture, this stays good in all stock analysis, although I try to give you the possible 4 reasons

- Aggressive accounting practices: The company might be managing its earnings through aggressive accounting methods, which inflate CFO relative to PAT.

- High depreciation or amortization: If the company has significant non-cash expenses like depreciation or amortization, it could lead to a higher CFO/PAT ratio.

- Tax management: Effective tax planning strategies could also influence the CFO/PAT ratio by reducing the tax impact on profits.

- Capital structure: If the company has substantial non-operating income or expenses, such as interest income or expenses from investments or financing activities, it could affect the ratio.

The ideal CFO/PAT ratio varies across industries and depends on factors like capital intensity, growth prospects, and business models. Generally, a higher ratio suggests better cash flow conversion from profits, but a sustainable and stable ratio is often preferred over extremes. For instance, a ratio between 0.6 and 0.8 is often considered healthy, but it’s essential to compare it with industry benchmarks and historical performance for a meaningful analysis.

DCX Systems Ltd (08-05-2024)

Nomura has initiated on the India Defence space, with DCX mentioned.

Anyone know where one can access the complete PFD copy?

Dharmaj ready to benefit from high demand for agrochemicals (08-05-2024)

On a conservative side 13 % would be bit difficult in dharmaj but the growth prospects looking good

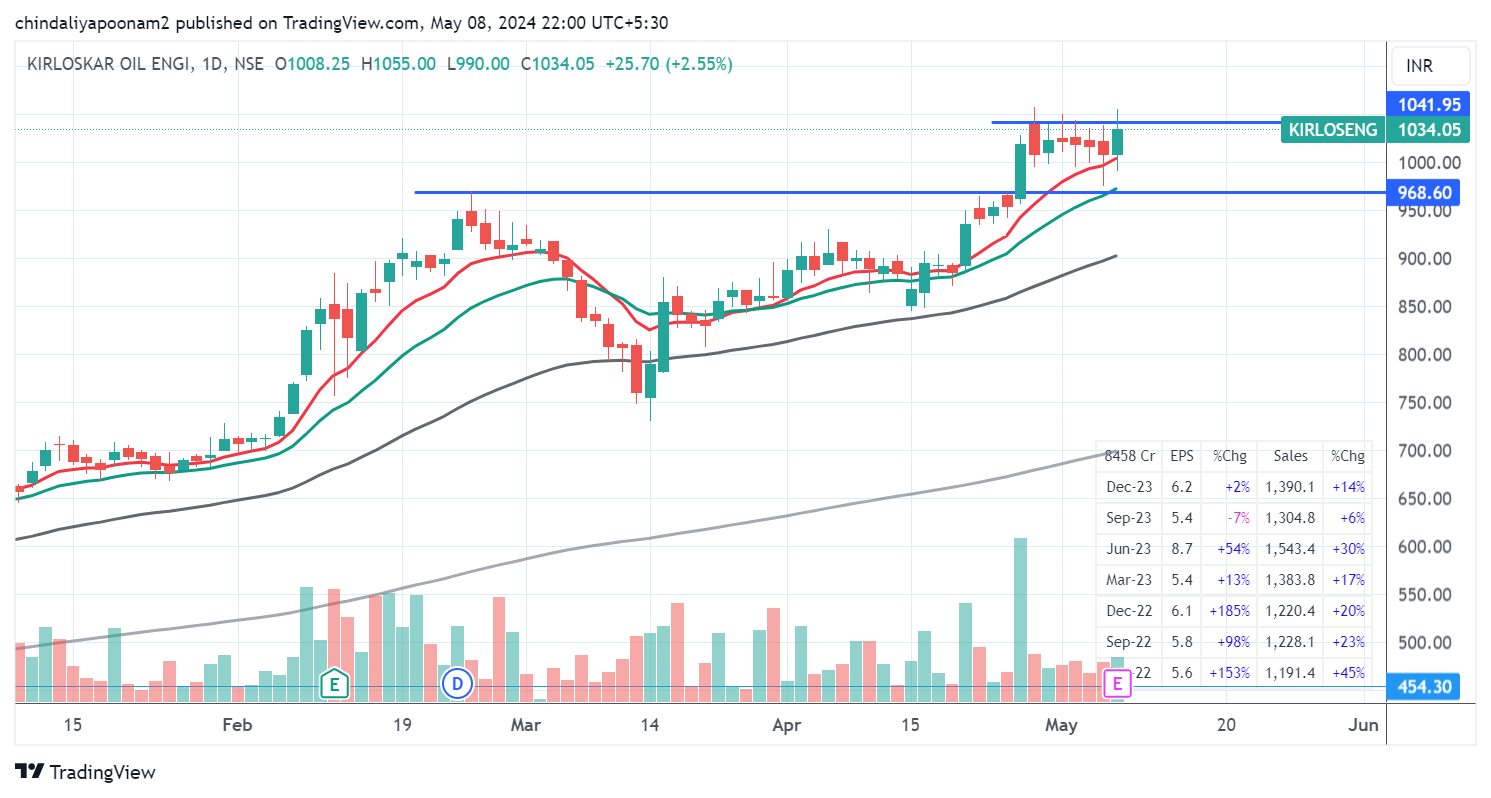

52 week highs and all time highs strategy (08-05-2024)

Kirloskar Oil Engine looking good on charts… Stock gave breakout with good volumes, now consolidating near ATH

Macfos Limited- A niche E-commerce Company (08-05-2024)

The result shown in the screenshot above compares the result of two quarters a year apart. So Jan-March 2024 has been compared with Jan-March 2023. Taken that way the company has experienced de-growth, which is bad.

Comparing the previous quarter (Q3FY24 vs Q4FY24) within the same financial year, the company has done good. But this is seasonality at play. Majority of the companies especially manufacturing companies, post their best quarter as Q4 of a financial year. Although, Macfos is not a manufacturing company.

As far as financial year comparison is compared i.e. FY23 vs FY24 is concerned, the company has done good and grown.

As an investor the de-growth that the company has experienced compared to last year’s quarter is a fly in the ointment, given that it is a microcap, expected to grow exponentially.

Piramal Enterprises Ltd (08-05-2024)

- Growth business shall be 100% off lending business- which means Wholesale 1.0 will be completely run down, and all lending revenue will be based on the growth business.

- Smaller legacy businesses shall aid in the cost of funds.

- SR reduced by Q1- Cash realisation of 1400

- AIF- 340 cr cash realised plus interpretation of AIF circular- write back of 1600 cr

Approx 3000 cr of provision run down

- 1400 of markdown of fair value markdown on non-earning assets

- Large stage 2/3 – 1000 cr settlement of account by taking settlement

- Provisioning buffer of 700 cr for future provisioning

-

Adjusted this against a similar amount from a one-off gain. This is beneficial to PEL in the long run and for the lender.

-

Wholesale 1.0 down from 44k to 14k cr- Book down by 30k, but credit costs 9000 cr in the last two years. lGD (Loss Given Default) is 30%. In the future, LGD could work on the remaining book- It is up to individuals to estimate it.

-

First, low-hanging fruits are disposed of. The last part is very difficult and risky. The most problematic fruits are left behind.

-

For PEL- Some of the large assets are out. A large account has gone out this quarter.

-

Retail growth will be slower going forward as compared to Fy24.

-

Run down is adjusted against undervalued or no valued assets. Hence, we thought of doing a run down by taking haircuts. One net basis net worth remains the same at the same time, taking a run down.

My view

Fee income—I’m not sure what is propelling fee income. Is it retail or wholesale 2.0 lending? How sustainable is this?

Another set of accelerated run down for wholesale 1.0. This term refers to the gradual reduction of a particular type of lending. They have mentioned this many times. As far as I understand (please feel free to correct), they have made similar statements at the start of FY24, in Fy23 and every year in the last 2/3 year. There is nothing conservative about their provisioning. IN Q3-24, they said we were done with provisioning and within 3 months, came up with 3000cr of write down. Based on the call, it looks like another set of 4 to 5000 cr provisioning is remaining (assuming 30% LGD on 14k wholesale AUM)

INR 67 bond (My limited understanding)- which is converted to cash 1/3rd per year. This is a kind of dividend but in a different format. They have reduced the dividend amount from Rs 33 to Rs 10. I am still figuring out why there is such a drastic reduction in dividends, but they are distributing the money to shareholders in a different format. For example, INR 67 bonds will be converted to cash 1/3 – INR 22 per year INR 10 dividend, which means around INR 32 dividend for FY24 and possibly for the next 2/3 years.

PEL has done a massive amount of bad lending in the last 5/6 years. Shareholders have paid a massive price for earlier management (confident but stupid, which massively increased wholesale lending at 25/30 CAGR before COVID). They will not acknowledge it openly, but the results from the last 2/3 years make it very obvious. They have buried their bad practices under the hood of DHFL, but they come every few quarters with accelerated wholesale provisions with a promise that they are reaching the end of the tunnel. The only silver lining is Wholesale1.0 is reducing much faster, so hopefully, they could recoup some of their losses.

INR 10k losses assets. Looks like PEL is unlikely to pay any taxes for the next 3/4 years even if they report 2500 cr PAT every year. This will help return ratio improve faster going forward.

Note: invested

Query on Banking Basics (08-05-2024)

Good question. I don’t think there is anything specific for banking. Just like any other business, as per Indian income tax regulations, losses from a specific business can be set off against future profits generated by that specific business (only!). So a bank can carry forward losses like any other business.

Now because a bank has past losses to carry forward, that means, tax wise, they will be able to generate profits but their final taxable profit would be after the previous year’s carry forward losses have been set off. This gain in bottom adds to the final Return on Assets number that a bank generates, and because Return on Equity is essentially Return on Assets * Gearing, it also has exponential gain on return on equity, specially for a leveraged business. Exemplifying how leverage boosts your profits:

Quote from Devil take the hindmost, A history of Financial Speculation by Edward Chancellor, pg: 207

Corporate leverage operates in a similar manner to the speculator’s margin loan. For exam-ple, if a company has earnings before interest of $100 million and interest payments of $90 million, then its net profits before tax are $10 million. A 10 percent increase in earnings to $110 million will produce a 100 percent rise in pre-tax profits to $20 million. Insull and other holding company operators in the 1920s enhanced the effects of corporate leverage by creating a pyramid of cross-shareholdings between heavily indebted companies

Here’s a snapshot of Consolidated P&L of IDFC First Bank for FY2021 (source: AR for FY2021 pg: 269)

Notice Balance in P&L carried forward from FY2020 to FY2021.