Meaning, for every 100 shares held we get 25 shares?

Posts tagged Value Pickr

Buy Unlisted Shares (06-05-2024)

Really? I tried it with NSDL for many days. Their mobile app is rejecting every password that I have tried.

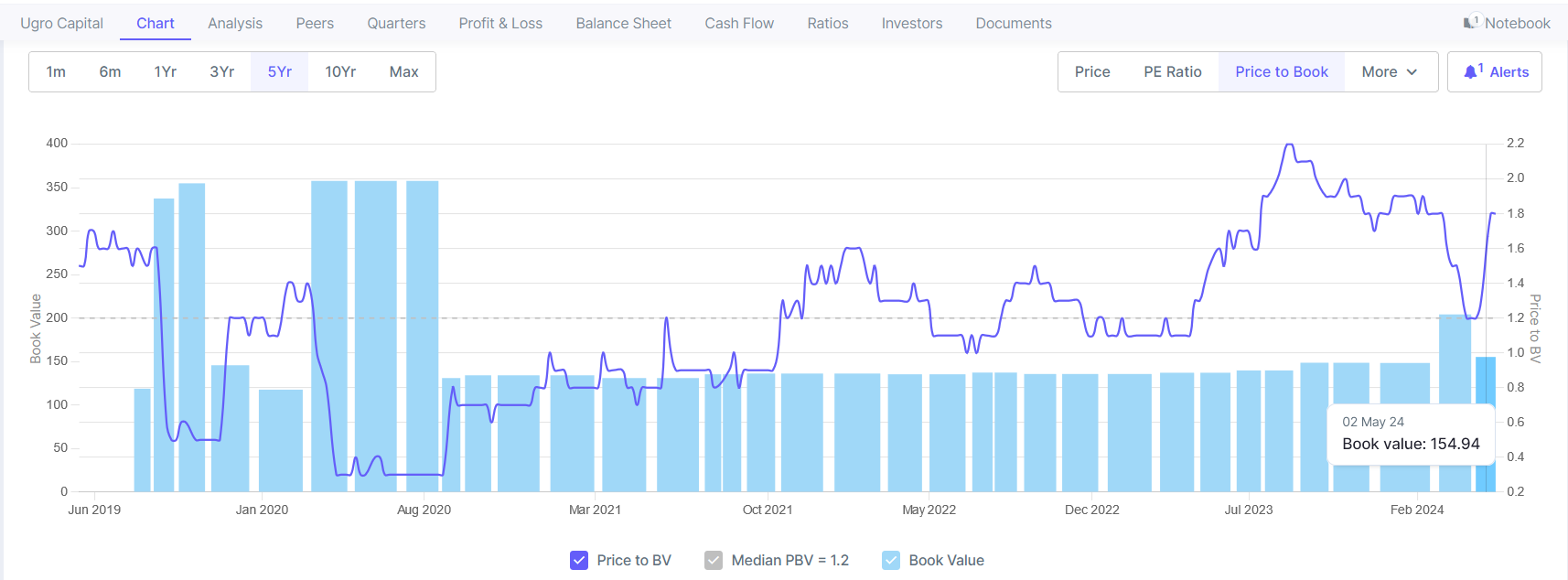

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (06-05-2024)

As per quarterly earning presentation the book value per share at the end of:

Q2 FY24: 150.2

Q3 FY24: 153.8

Q4 FY24: 157

So, no compression of the book value.

Smallcap momentum portfolio (06-05-2024)

@Anand_Jain Is the order also matching? @Malepati_Varaprasad had a slightly different order.

Smallcap momentum portfolio (06-05-2024)

@Malepati_Varaprasad Happy that you have created your pf.

I am interested to see why there is a difference. Is this the order for this week? Most of the numbers are identical except a few that are interchanged.

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (06-05-2024)

why drastic compression of book value from 204 to 157 in Q4FY24?

Gravita India success story (06-05-2024)

Gravita India FY24 results and conference call:

Consolidated Topline/ Topline growth YoY: 3161Cr / 13%

EBITDA/ EBITDA Margin for FY24: 285Cr / 9%

PAT / PAT GROWTH YoY: 242Crs / 18.6%

Commentary:

-

Gravitas’s wholly owned subsidiary situated in Tanzania, Gravita Tanzania Limited, has increased the battery recycling capacity by 5,000 metric ton per annum, bringing the total capacity of battery recycling of this unit to 12,000 metric ton per annum.

-

Gravita has expanded its total capacity to 3 lakhs plus metric tons per annum in Financial Year ‘24 compared to 2.34 lakh metric tons per annum in Financial Year ‘23, which shows an increase of 28%. The company aims to increase our capacity to 5 lakh plus metric tons per annum by Financial Year ‘27.

-

Volume growth is less in aluminum because there is no hedging mechanism for the same. Alum. alloy contracts are expected to be launched soon on mcx which will help the company hedge the metal.

-

EBITDA per ton for plastic is Rs. 11,176 per ton, lead is Rs. 19,252 per metric ton and aluminum is Rs. 15,308 per metric ton in Q4 Financial Year ‘24. This is in line with the company’s target.

-

45% of revenue in Financial Year ‘24 came from value-added products, management aims of achieving 50% revenues from this category. India contributed 62% and the balance contribution of 38% is from overseas business.

Vision 2028. Management has stressed on the following points as a par of their 2028 vision.

-

Diversifying into new business verticals like lithium-ion, steel and paper.

-

Aiming for revenue CAGR exceeding 25%, profitability growth surpassing 35%, maintaining an ROCE of 25% plus

-

Elevating non-lead business to over 30%, using 30% plus renewable power and reducing energy consumption by 10%

-

Commitment to sustainable development, increasing the proportion of value-added products to 50%

-

by fy 2028 the company wants revenue from non lead business to contribute 30% to the topline

Management on Aluminum capacity utilization: The company had only capacity utilization of 11% in the case of ADC12. So, this year, they plan to increase it once the contracts are in place on mcx. Management expects that the derivative should list somewhere in next quarter and then brand empanelment will start. So, in Q4, they expect it to have a growing volume. And next year further, the volume growth and capacity utilization to higher levels. The aluminum business will grow at least by 60% to 70% in terms of volumes because they are also adding capacity at a certain location, at Ghana, that should be operational in the beginning of the Q2.

Management on Supply chain issues: Mgt. also mentioned about the logistics delay and macroeconomic challenges they feel by addressing the issue by diverting the volumes to other geographies, as the company has touchpoints all over the world… So, wherever there is an issue like this they encounter it by diverting the volumes to other geographies without affecting the volume growth.

Arbitrage play: The management mentioned that this year, they have not taken as much domestic scrap simply because the overseas scrap was much cheaper compared to the domestic scrap, and there were some arbitrage opportunities. Overseas markets were lower compared to Indian markets.

So, they bought more international scrap as compared to domestic scrap. So, this also contributed to their increased working capital cycles.

Regarding Amararaja putting up a plant: They mentioned that Amara Raja is only putting a plant in the south, but they sell this battery everywhere in India. while Gravita has plants in the North, in central and even in west India. The specific benefit that we have is that we can process it in the northern plants and then we can give the finished products to Amara Raja from the south plant itself. So, that gives us the advantage over the competition

I feel that this is a good time to deep dive in the recycling sector and feel that garvita is in a great space with a huge market potential. I have made some tracking position and would track it as closely as I can.

Lazycap’s Portfolio – Feedback (06-05-2024)

Update

Added some 30% position on top of existing to KMB in two tranches one at 1660 and other at 1550. Current avg price of total holding stands at 1705. On cost basis KMB is 20% position now and at portfolio level it is around 15% position. This addition was with some cash inflow from my salary which was happy coincidence with the fall

I was seriously mulling over selling a lot of other holdings and adding a lot more of Kotak if it falls to 1300 levels, still can do but that price level could be a wishful thinking

Indian Hotels–for long term portfolio stability (06-05-2024)

Can you please share the sources that you use for getting the reports that calculate valuation parameters such as EV to EBITDA after calculatedly anticipating/predicting a company’s future performance?

Meghmani Finechem – Underrated multibagger? (06-05-2024)

My One of friend is Manufacture of PVC Laminate sheet , and other friend is dealing in PVC , CPVC regained -its material that is kind of scrap made from cpvc pipe and other bunch of material .

In Plastic industry other most used and low value chemical is calcium

Calcium is mostly have three type i see in market

- Domestic : calcium is natural material and by grinding natural calcium stone manufacture mostly in india we get in Rajasthan and near ambaji region . in domestic calcium is cheaper and have more percentile of silica in calcium . mostly available in range of 5000-7000 inr/MT

- International : in Import there are mainly two type of calcium : 1)Vietnam : Vietnam calcium is more purity and mostly used by PVC pipe manufacturer . even though they used also domestic Calcium when Price is increase of Imported Vietnam calcium , this Vietnam calcium is give pure white tone in Pipe ,its price rang is approx. 9000-12000 /MT ,in Gujarat 50X20 imported from Vietnam it self.

-Secound type of imported calcium is imported from JORDAN , its calcium give IVORY tone thats why its application is not feet into PVC PIEP, its low value then Vietnam Calcium and its bulck Product , it used in manufacturing of non vergine molecular typically mixed with Reliance /ongc /armaco PP to Cost cutting used in POLYPACK AND FIBC BAG manufacture .industry is cut through competition and in this calcium having wafer thin margin .

–But in calcium margin is wafer thin and extended credit period of 90-120 days and another problem is Non consistency of Product Quality .

SO even calcium like material that is totally low product like calcium that having approx. 1X20 container value approx. 2.5-3 lakh in that case manufacturer buy from dealer and distributor . one reason that get credit of 60-90 days . second reason is for any company that directly sells to dealer or end customer that face one critical problem of Large Inventory , check out the innerwear manufacturer that operate EBO , there big chunk of money stuck in inventory , by selling to distributor /dealer company once sell inventory goes out now its distributor inventory not company Inventory and also company can used some part of money of distributor and utilize Working capital .

Think about this 2.5.-3 lakh is very small amount for Piep manufacturer then also 9/10 buy from domestic dealer not from Direct exporter or from Exporter of material. same case with high value product like PVC.

where i Live is manufacturing Hub of Ceramic/Polypack /Fibc Bags/non vergin PP /PVC Piep I Get this insigh from friend who are Managing director or working in this industry.

Company may sell to Direct End Costumer like BIG PVC PIEP manufacture , but its totally fine to have delar and distributor network , even though i tried to contact company to ask about same but didnt get any response .

I would love to connect also personal level fellow investor friend who having same interest , because i have friends but with no serious interest in Investing so feel free to connect me : Parthsarsavadiya@gmail.com