People exiting or entering a stock based on one exchange filling error should revisit their thesis (if they have one) before making such decisions. Especially in case of SME stocks, one needs to have strong understanding of the business before buying the stock.

But looking at the reactions here, looks like people just jumped in the wagon reading the word VFX in company’s profile and are now jumping out because company didnt show 50% profits YoY (I dont think they even promised that).

In stock market, decisions without thinking are the most expensive ones. Please be patient and wait for clarification to emerge after concall scheduled next week.

Dear Value pickr family,

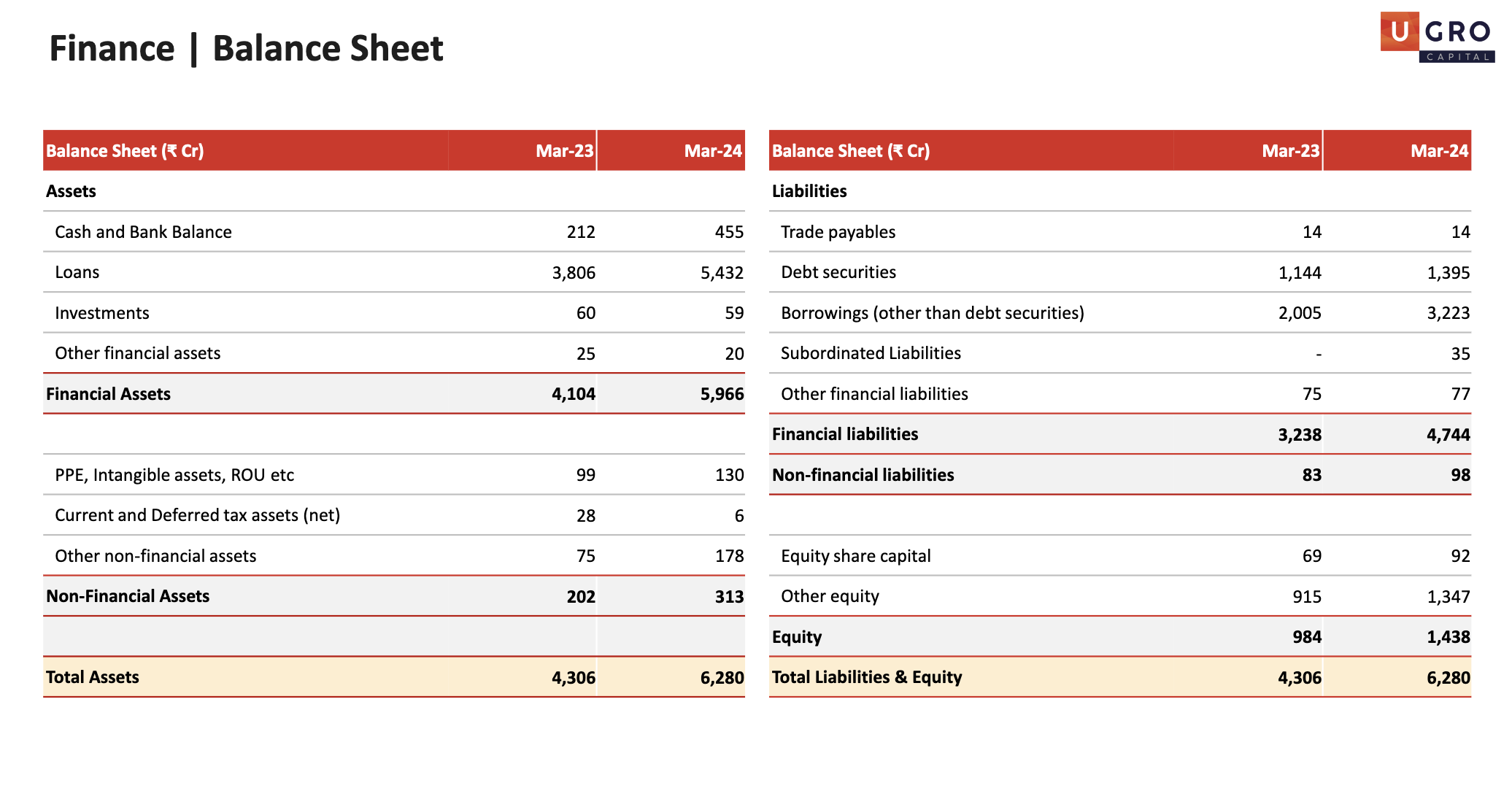

Could anyone of you help me to understand how the ROA of Ugro is being calculated for F24.

ROA: 2.3%

AUM: 9047Cr

On book and off-book mix for loan is 55:45

Management said that they calculate the ROA on balance sheet and not on AUM. Please explain me the calculation. Thanks!

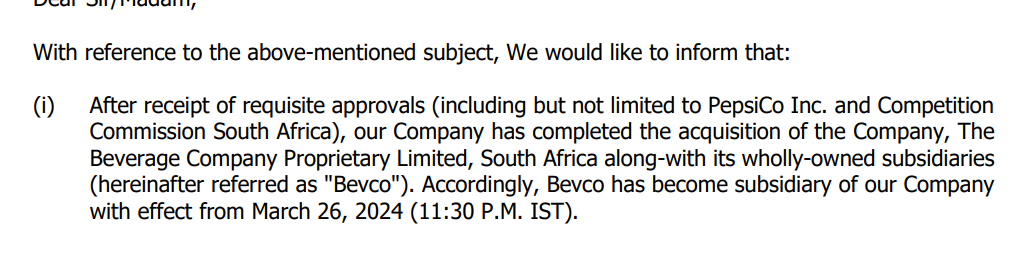

@Jitendrapd94 As Bevco became subsidy on 26th March , 2024 , will its earning will be part of March quarter consolidated earning ?

Having three entries muddled up is not typo

Employee Expenses reduced, current assets go up, direct expenses changed

In their favour tax paid was based on higher value.

Could be intentional, oversight, who knows. Definitely not done themselves any favour

P.S.: disclosure : invested. Exited partially today

RPG Lifesciences –

Q4 concall and results highlights –

Q4 outcomes –

Revenues – 127 vs 118 cr ( up 7 pc )

EBITDA – 22.4 vs 17.8 pc ( up 26 pc, margins @ 17.6 vs 15 pc )

PAT – 13.2 vs 10.4 cr ( up 28 pc )

FY 24 outcomes –

Revenues – 582 vs 512 cr ( up 14 pc )

EBITDA – 135 vs 107 cr ( up 26 pc, margins @ 23.3 vs 21 pc )

PAT – 87 vs 67 cr ( up 30 pc )

Segment wise performance for FY 24 –

Domestic branded formulations – 390 vs 340 cr ( up 15 pc ). New products ( launched after FY 19 ) contributed to 25 pc of sales. Sales force productivity crossed 5 lakh

International formulations – 106 vs 92 cr ( up 15 pc ). New products ( launched after FY 19 ) contributed to 30 pc of sales

APIs – 85 vs 79 cr ( up 7 pc ). Company hopes to ramp up API segment growth into double digits – going fwd

Company’s leading brands in India formulations market include –

Azoran ( immunosupressant )

Aldactone ( Diuretic – used to treat high BP/ heart failure )

Lomotil ( used to treat diarrhoea )

Naprosyn ( potent painkiller )

Serenace ( anti-psychotic )

Norpace ( used to treat abnormal heart rhythm )

Manufacturing facilities –

02 – formulations facilities @ Ankleshwar. Unit -1 caters to domestic and emerging mkts. Unit -2 caters to developed mkts

01 – API facility @ Navi Mumbai. Company makes the APIs of immunosuppressants in-house

In Q4, company’s secondary sales grew by 19 pc vs Industry growth of 6 pc !!!

Naprosyn and its line extensions – touched 75 cr sales in FY 24

Immunosuppressants portfolio – touched 70 cr sales in FY 24

Company aspires to take both these portfolios beyond 100 cr sales each

Cash on books @ 127 cr – actively looking at M&A opportunities ( cash build up has happened despite spending 140 cr for modernisation of one of their formulations and API facilities over last 2 yrs )

Company has traditionally been a laggard wrt chronic therapy sales. Have identified Derma, GI, Cardio, metabolic disorders – as key focus areas to ramp up their presence in chronic therapies. The ramp up shall however take time as the incumbents are well entrenched

The Jan-Aushadhi Kendra led Generic-Generic medicines do pose a long term threat to the company. However, if the manufacturers supplying to Jan-Aushadhi Kendras were to comply with the WHO GMP / Other quality standards, their product costs shall rise materially and be comparable to branded generics

When the company launches a new product in the Mkt, its manufacturing is generally outsourced. Only when its volumes build up beyond a certain scale, the company brings its production inhouse

Some countries to which company is exporting to are facing forex shortages. Hence the Govt’s there are resorting to import restrictions which is reducing company’s export growth rates. Still, Pharma Industry is one – which is the last one to face such restrictions

Company has identified new APIs for in-house manufacturing. Aim to launch these by FY 26 – should lead to better growth rates in the API vertical

Disc: holding, biased, not SEBI registered

RPG Lifesciences –

Q4 concall and results highlights –

Q4 outcomes –

Revenues – 127 vs 118 cr ( up 7 pc )

EBITDA – 22.4 vs 17.8 pc ( up 26 pc, margins @ 17.6 vs 15 pc )

PAT – 13.2 vs 10.4 cr ( up 28 pc )

FY 24 outcomes –

Revenues – 582 vs 512 cr ( up 14 pc )

EBITDA – 135 vs 107 cr ( up 26 pc, margins @ 23.3 vs 21 pc )

PAT – 87 vs 67 cr ( up 30 pc )

Segment wise performance for FY 24 –

Domestic branded formulations – 390 vs 340 cr ( up 15 pc ). New products ( launched after FY 19 ) contributed to 25 pc of sales. Sales force productivity crossed 5 lakh

International formulations – 106 vs 92 cr ( up 15 pc ). New products ( launched after FY 19 ) contributed to 30 pc of sales

APIs – 85 vs 79 cr ( up 7 pc ). Company hopes to ramp up API segment growth into double digits – going fwd

Company’s leading brands in India formulations market include –

Azoran ( immunosupressant )

Aldactone ( Diuretic – used to treat high BP/ heart failure )

Lomotil ( used to treat diarrhoea )

Naprosyn ( potent painkiller )

Serenace ( anti-psychotic )

Norpace ( used to treat abnormal heart rhythm )

Manufacturing facilities –

02 – formulations facilities @ Ankleshwar. Unit -1 caters to domestic and emerging mkts. Unit -2 caters to developed mkts

01 – API facility @ Navi Mumbai. Company makes the APIs of immunosuppressants in-house

In Q4, company’s secondary sales grew by 19 pc vs Industry growth of 6 pc !!!

Naprosyn and its line extensions – touched 75 cr sales in FY 24

Immunosuppressants portfolio – touched 70 cr sales in FY 24

Company aspires to take both these portfolios beyond 100 cr sales each

Cash on books @ 127 cr – actively looking at M&A opportunities ( cash build up has happened despite spending 140 cr for modernisation of one of their formulations and API facilities over last 2 yrs )

Company has traditionally been a laggard wrt chronic therapy sales. Have identified Derma, GI, Cardio, metabolic disorders – as key focus areas to ramp up their presence in chronic therapies. The ramp up shall however take time as the incumbents are well entrenched

The Jan-Aushadhi Kendra led Generic-Generic medicines do pose a long term threat to the company. However, if the manufacturers supplying to Jan-Aushadhi Kendras were to comply with the WHO GMP / Other quality standards, their product costs shall rise materially and be comparable to branded generics

When the company launches a new product in the Mkt, its manufacturing is generally outsourced. Only when its volumes build up beyond a certain scale, the company brings its production inhouse

Some countries to which company is exporting to are facing forex shortages. Hence the Govt’s there are resorting to import restrictions which is reducing company’s export growth rates. Still, Pharma Industry is one – which is the last one to face such restrictions

Company has identified new APIs for in-house manufacturing. Aim to launch these by FY 26 – should lead to better growth rates in the API vertical

Disc: holding, biased, not SEBI registered

Zomato could also start subscription based service for restaurants where they provide the analytics of their own restaurants to grow and improve. This would also increase the buy orders from customers and further improve the sales for Zomato.

Questionable Capital Allocation of late. Co’ has become a Fund Manager.